Hi RIP readers,

Last months my finances have been dominated by currencies fluctuations more than savings and/or investments earnings (and/or weddings!). I’ve always considered currencies fluctuations a minor factor (and I still do) in wealth management. A factor not worth taking into account, especially when talking about three of the most stable currencies around: the Euro, the U.S. Dollar and the Swiss Franc. They’re pretty solid, aren’t they? None of these will swing by more than 5% in a year compared to any other of them, am I right? We’re not in Zimbabwe!

Well, no. Currencies, even the most stable, have trends and drifts. They’re like giant turtles: they have smaller short term volatility compared to stocks and bonds, but they may go on a straight line for months and accumulate a substantial gap over years.

Before you start screaming: no, I’m not going to invest in Forex or other pure speculative assets anytime soon. Speculating over currencies is a pure bet and you shouldn’t do it for the following reason: while stocks and bonds are expected to grow in the long run, currency pairs are expected to stay neutral. Why? Well, you tell my why not! So you’re facing trade fees for a zero expected return. Even worse: professionals and more informed traders are playing with Forex trading better than you do. Guess who’s going to get the pluses in this zero (almost, due to trade fees) sum game?

So why do I care about currencies?

Diversification.

Yes, the wise investor mantra! Diversifying by currency is another way to avoid betting on a single horse, a way to edge yourself against high inflation in your main currency.

“But RIP, being exposed to a single currency is how almost anyone live… Are we all crazy??”

No, they are not. But it’s important to know that even though my grandpa is not investing, he actually is. He’s investing all in Euro currency: his pension, his flat and his savings. It’s an accepted risk, maybe. But it’s important to be aware and recognize you’re at risk. A small risk, if your main currency is the one used in the country where you live and where you plan to live for the rest of your life.

Anyway my situation is different – and I assume I’m not alone in this, given the high mobility of my generation: I was born in Italy, I’m living in Switzerland and I’m working for an American company (and planning to comeback to Italy). I need to play with three currencies!

Note: when I say “diversify by currency” I don’t mean the trading currency. I mean the currency of the underlying assets. For example, if you own a S&P 500 ETF traded in CHF it doesn’t mean you are exposed to CHF, you’re still exposed to USD which is the currency of the underlying assets. In case CHF halved compared to USD, you’r fund is going to instantly double its face value in CHF.

“Ok, RIP, what are you going to do to edge yourself against currency fluctuations?”

Well, I don’t know yet. First step is always awareness: I’ve added a new sheet to my NW spreadsheet to monitor my currency exposure across EUR, CHF and USD.

Second, I’m probably going to try to keep my exposure almost always balanced, eventually slight unbalanced in favor of EUR first, CHF second and USD third – that’s because I plan to retire in Italy. If plans will change, balance changes too. I’m not going to formalize this by adding some rules to my IPS, I’ll just drop an eye on it every once in a while.

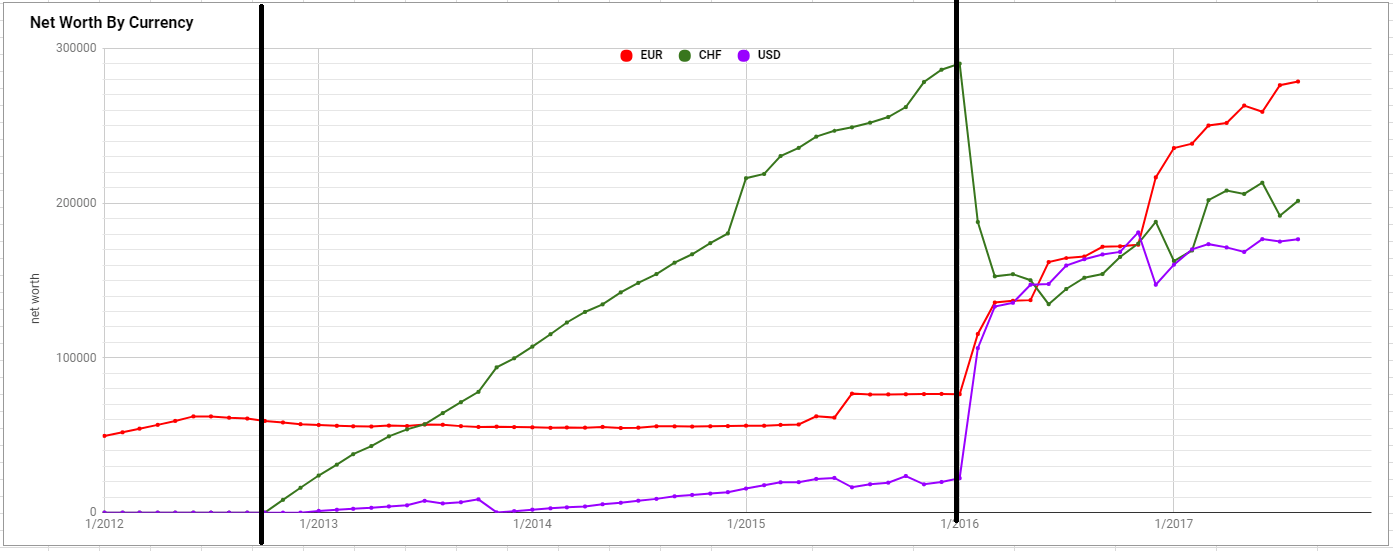

Let’s take a look at our currency split over the last 5 years 🙂

Here are absolute values of assets in each currency.

To compare apples with apples everything is converted to EUR. It means the ~290k peak in the green CHF line in January 2016 is actually ~320k CHF (1 CHF = 0.903 EUR in January 2016).

What we can see is that last 5 years can be divided in 3 phases:

First, the “What are other currencies?” phase. From minus infinity to November 2012. Before moving out of Italy I only owned assets in Euro and everything was easy.

Second, the “Holy sheet let’s pile a huge amount of cash in this fancy currency!” phase. From November 2012 to January 2016. I’m so dumb. I’m sooooo dumb. I’ve been saving ~70% of my salary and watching the pile grow in my 0.1% saving account. So ridiculously dumb. Btw, the jump in January 2015 is due to unpegging CHF to EUR. I’m so dumb.

Let’s take a look at S&P500 between November 2012 and January 2016

Out of those 320k CHF, 200k were investable cash (the rest being Pension Pillars 2&3). I just ran the math to quantify my dumbness, i.e. how much it would have become if I had invested month by month during those 3 years. Drums roll… 242k tadaaaa. I left 42k CHF on the table by not investing for those 3 years. Second biggest financial mistake of my life!

Takeaway for you readers: invest as soon as possible.

I’ve always been financially illiterate and scared of market crashes. I just stashed cash, but to reach FI you have to invest your stash. You need your green army to go to work for you!

Third, the “Wait, let’s try to be smart” phase. From February 2016 on. Started investing, differentiated by asset class, markets, currencies… Did a huge rebalance in November 2016 to expose myself more to EUR than CHF and USD. EUR is so predominant today due to currency fluctuations, maybe I’ll rebalance again in January 2018.

Here’s percent split of our NW:

and here an area chart because… why not?

Final thoughts: even if you’re living your single currency life, please take few minutes to consider whether it’s worth diversifying your assets by currency. This is not a game where passive play is safer than active. You’re always in the game, even if you’re not aware of it.

I’m not sure I entirely agree with the way you approach currency diversification. S&P500 companies may be traded in USD, but hey have significant chunk of their profit from abroad. So are Swiss companies that earn quite a lot in EUR/GBP/USD lands.

Now, I don’t have a way to accurately count this, so I just don’t 🙂 I do look at the country/region allocation, which, in a way, is a proxy for the currency exposure.

Good point indeed. Stock markets are strongly coupled due to globalization, but a good chunk of my NW is in Pension Pillars (CHF) and in a flat in Italy (EUR) and cash. Currency diversification happens at a higher level than stocks.

We currently keep track of our investments in 3 currencies too. (4 if I consider my small portion of GOLD junior miners in CAD)

In fact, Currency is an interesting argument when discussing retiring in another country out of your main currency’s investments.

I’d like to run some simulations using ERN data from their SWR series but including the impact of currency exchange in different countries.

Four more stable currencies I don’t see much of a problem (EUR/CHF) but with more volatile currencies like in LAM, it would play a big role if we keep the investments in CHF or USD and we need to convert every month for living expenses.

Anyway, I’m glad you’re back on track and keeping us updated.

Cheers!

Hi MrRIP,

Just wanted to say thanks so much for keeping the blog updated. My wife and I are currently in the “so dumb” phase and have a big pile of CHF cash just sitting in a postfinance account earning 0%. We are a multi-currency asset holder and also have the joy of exposure to GBP!

Just trying to assess what to do. We are simplifying our finances and then need to make a jump into the market at some point. The psychological block of having a large chunk of cash and not wanting to get burned in a market correction is a tricky (but ultimately nice) problem to have. I really wish we had started index investing years ago instead of cash collecting!

Thanks again for the great blog – it is appreciated.

Same regret here. Had I started investing back in 2012 (as soon as I moved to Switzerland and started earning big money) Now I’d be much closer to the Big Goal 🙂

If you’re scared of a “big jump” into investments, try to start little. Tell yourself you’re putting 10% or 20% or 30% into Stock ETFs and stick with this “not that aggressive” plan.

Change your asset allocation as you get more confident – and hopefully after you’ve experienced a 10+% market correction 🙂

I just recently started reading some blog posts, really good to hear that there are other Swiss Bloggers ?

Also very interesting how the huge investment numbers show, what currencies can do to the portfolio. I’m having at the moment around 60% USD and 40% CHF, and a few EUR which are not reasonable to mention.

About the EUR, I don’t have that much faith in it. It’s a pretty new currency and also its only goind down since it got implemented. I remember when SNB removed the 1.20 minimum price CHF/EUR, it was a disaster, a lot of money got swallowed up for the swiss people holding big amout of EUR. Not sure if there is a long term future for the EUR (50+ years).

Best Regards

Thomas

60% USD and 40% living in Switzerland is a dangerous split.

How have you performed lat months, since the USD has been losing terrain in last 6-7 months?

Sorry for the late answer, my portfolio is doing fine. Having some issues with GE and Altria, otherwise it looks good 🙂

I do really like US companies, additionaly I get more motivated if I earn mothly or quarterly dividends.

Regards

Thomas

Hey Mr. RIP

As CHF is going down against EUR (and it looks like it won’t stop in the nearest future), will you take any actions regarding your exposure to EUR? As you mentioned, you are planing to move back in Italy once you reach FI, so it would be interesting to know your approach regarding these recent unusual swings in currencies.

Thanks a lot

MM

What makes you think that ‘it looks like it won’t stop in the nearest future’?

If you think so just invest ultra-leveraged in forex!

My model for currencies is that they’re a zero sum game, so I don’t bet on them.

Of course I’ll react to that though. If one day retiring in Switzerland would be cheaper than in Italy (and better quality of life), I may change my mind 🙂

Hi Mr. Rip,

I was just making an assumption based on the recent CHFEUR decline, hopefully it wont last long or at least it will stabilize. I have somewhat similar exposure as yours (earning salary in CHF and investing in USD, EUR etf’s) and plan to retire in EUR country. I guess being a novice investor I overthink too much were there is no reason to do so.

Would you mind elaborating about the currencies being a zero sum game?

Thank you

MM

By zero sum game I mean I don’t expect the price to go in any particular direction.

If we run 100 simulations of the world in parallel for 100 years I expect the average value for CHFEUR is same as today.

While I expect S&P500 to be 1000x today’s value (7% growth per year ~= 1000x in 100 years)

The only factor that can make a currency pair drift is different inflation rates in the two money markets, but that’s again accounted in the zero sum game. I mean, if inflation rate in US is 2% per year and in Switzerland in ZERO, I expect USDCHF to drift a little bit over time to compensate the fact that what costs 1 USD and 1 CHF today will cost 2 USD and still 1 CHF in 36 years.

Investing in companies that operate in the global market should be currency neutral.

Now it makes much more sense. Thanks a lot for a quick response!