Gruezi RIP Freunde,

Welcome back to the Switzerland series!

Today questions are: when and how will my Pillar 2 & 3 be taxed?

We’ve took a look at the Swiss Pension System in a previous post. We’ve seen how Pillar 1, 2 and 3(a) work. We’ve seen that Pillar 2 & 3a are pre-tax investments thus when you withdraw them as lump sum you have to pay a tax named Kapitalauszahlungssteuer.

In this post we’re going to take a deeper look at this tax and how to optimize your withdrawing to pay as less a possible of it.

Let’s split the initial question in two. First: when will my Pillar 2 and 3a be taxed? When am I going to pay the Kapitalauszahlungssteuer, i.e. the lump sum tax?

You’re going to pay taxes based on the withdrawal actions from your Pillar 2 & 3a on each year. You can’t withdraw whenever you want from your tax advantage accounts though. Withdrawal actions from your Pillars happen when:

- You reach retirement age and choose to get a portion (or the whole) capital as lump sum.

- You buy a house of primary residence.

- You start a company.

- You permanently leave Switzerland.

- (some other minor circumstances).

I said “on each year” because lump sum tax is based on the amount you withdraw during a tax year.

It means that if you withdraw X this year, you pay – this year – the tax due on the full withdraw of amount X. If, instead, you withdraw half of X this year and the other half next year, you pay the lump sum tax due on a withdraw of half of X both this year and next year, which is usually less than the tax due on a single withdraw of X thanks to the progressivity of the tax.

So, first rule of thumb: if possible, split the withdraws over more than one year.

Before moving to the second question, I need to admit that I don’t know the actual details of Kapitalauszahlungssteuer payments. I mean, if you withdraw from N different Pillar 3a accounts you owe the tax due on the whole withdrawn amount. I’m not sure you get to access the gross amount from your accounts and then pay your tax at tax declaration time the year after. You may have left the country and be unreachable (and not accountable any more). I guess your funds/vested benefits accounts are going to withhold the expected tax on each lump sum and then you have to pay the difference at tax time, which is still risky for the government but at least you’ve already paid a good portion of your due tax. A safer option for the government would be to force you to communicate all other withdraws and withholds you had during the year so that on each withdraw you’ll pay the right tax due. I’d love if someone could bring their experience and clarify this point. Anyway, that’s just a technical issue and if you (like me) don’t plan to game the system in illegal ways (don’t, just don’t!) you shouldn’t care.

There are legal ways to minimize tax due though. For example we’ve already seen that splitting the withdraw over multiple years helps.

Next trick is: the lump sum tax is due in the Canton where your fund/vested benefits account is domiciled. It doesn’t depend on your domicile, even though your employer’s Pillar 2 and your Pillar 3a bank accounts are probably in your Canton of residence.

“RIP, does that make some difference? Do I have control over it?”

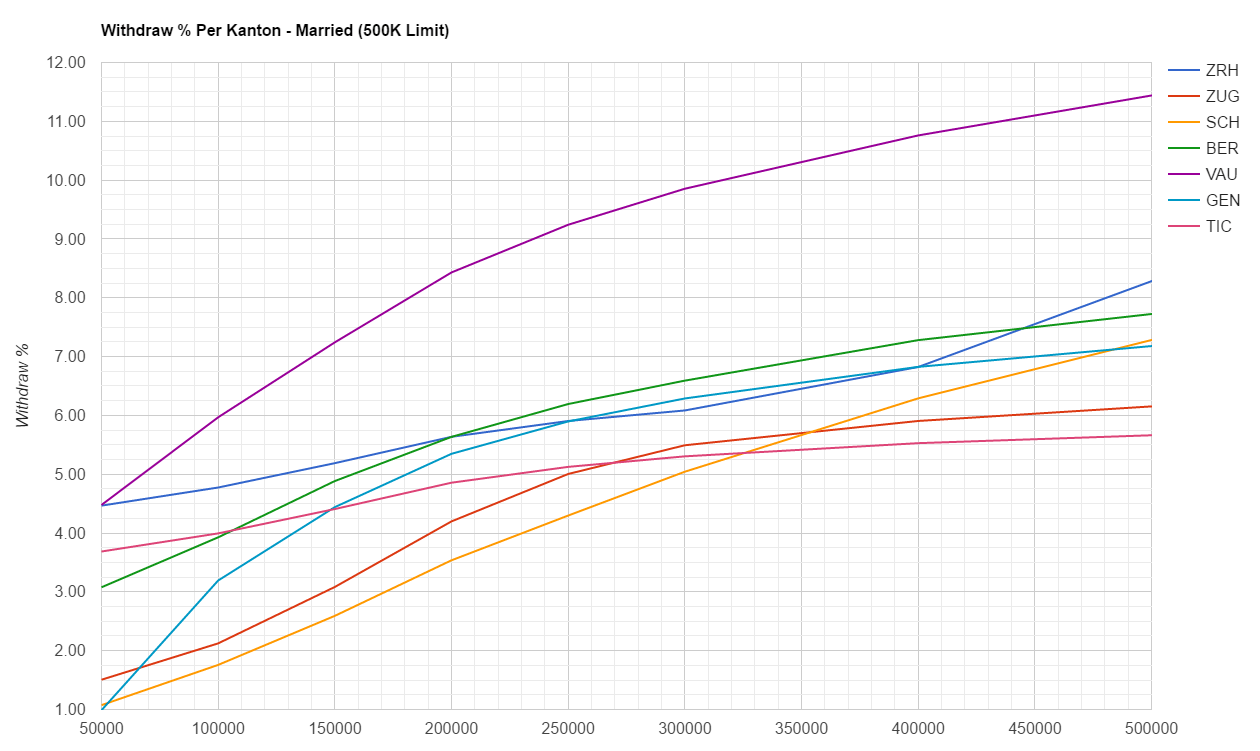

Sure my friend, let’s take a look at the tax rates on some popular Cantons. I’ve manually pulled data from the PostFinance tool for lump sum payments and I’ve created this spreadsheet. Here’s a screenshot

Data have been extracted beginning of November 2016. They’re probably going to change every year since federal government and individual Cantons can change their tax brackets. Having a way to extract numbers automatically would be great (I tried to inspect the HTML to find some API I could call but I failed). I won’t keep the spreadsheet in sync with the official data in future.

The Cantons considered for the analysis are:

- Zurich, Zug, Schwyz and Bern (German speaking)

- Geneve and Vaud (French speaking)

- Ticino (Italian speaking)

The selected Cantons represents all the (main) language areas of Switzerland, they are roughly the most populated ones (sorry Aargau). Some of them are there just show off their tax skills (welcome Zug and Schwyz).

On the left column of each region you’ve the amount to withdraw. I’ve analysed the range 0-2M CHF with 50K increases till 300K, then 100K increases till 1M, then 200K increases till 2M.

The upper blocks are absolute tax you’d pay to withdraw that amount in that Canton. Lower blocks are percentages.

There are 3 different scenarios analysed:

- Single person with no kids.

- Single person with with kids, apparently it doesn’t matter how many.

- Married couple, same applies for registered partnerships / civil unions. Apparently it doesn’t matter if you have kids. Most of the time tax brackets for a married couple are identical to those for a single with kids.

I completely removed church tax from the equation. All scenarios are without religious affiliation. Yes, in Switzerland there’s a tax on your religious affiliation.

Hi highlighted the top 3 (three shades of green) and the worst (orange) Cantons from a tax perspective on each scenario.

Few considerations:

- Zurich sucks.

- Vaud sucks.

- Zug is the asymptotic best Canton on every scenario.

- Schwyz is awesome for married couple up to 300K.

- Ticino Canton is amazing from 200K to 1M.

Some graphs (click on the images to enlarge them):

“Ok RIP, great, now I know I live in a sheetty Canton and when I’ll get my Pillar 2 I pay a lot of taxes. Is there something I can do about it?”

Yeah, you have control over it. You can open a vested benefit account in a Canton you like and transfer your funds there. There are even institutions who can do that for you (with reasonable fees).

So don’t worry, keep accumulating wealth into your Pillar 2 & 3a and at the time of withdrawal just evaluate if it makes sense to open a vested benefit account in a tax favorable Canton.

Mind that in 2020 there will be a major Pillar 1 & 2 reform and that they may make harder to pull money from Pillars (and Cantons can always play with the lump sum tax rates). There’s no guarantee that your today’s strategy will work tomorrow.

“But… what happens if I have a Pillar 2 in Canton X and a Pillar 3a in Canton Y?”

Well, I don’t know. I don’t think you’re going to pay taxes on each Canton based on the split funds volumes, that alone would be another nice tactic. I guess you pay the marginal tax on the amount you withdraw on each Canton based on previous withdraws as if they were all in the Canton where you’re performing the withdraw. But these are just speculations, if anyone has more information please let me know.

That’s all folks!

Before letting you go, let’s analyze a case study:

RIP Family

- According to rows 13 to 15 of my NW document, my current Pillar 2 & 3a capital is 126K CHF (end of October 2016).

- I do plan to invest 20K in a Pillar 2 buy in this year (2016).

- I won’t do any other buy in on the following years: buy ins are locked for 3 years and I do want to be free to withdraw by January 2020 (which corresponds to my current optimistic FI date).

- I do plan to keep investing 6.7K per year on Pillar 3a.

- I plan to keep my Pillar 2 monthly contribution at 8.5% (100% matched) of my gross salary, which means ~2450 CHF per month. Probably going down since I’ll start working 80%, but I plan to get a promotion within 12-18 months so I can assume the average will stay the same.

- I do plan to be in the Married/Partnership or at least have a kid.

- I assume Pillar 2 interests of 1% and Pillar 3a interests of 0.2%.

- I may work a little bit to find a better Pillar 3a options but it’s not my first priority. I may leave Switzerland in 3-5 years and I may be ok with investing in a saving account. We’re talking of 4-6 Pillar 3a contributions, i.e. 27-40K CHF.

This leads to a Pillar 2 & 3a projection of ~275K by January 2020 and 355K by January 2022 (forecast spreadsheet here).

Assuming, from a tax perspective, the worst case scenario where I won’t be able to split the withdraw between 2 tax years and that I will be able to withdraw the whole Pillar 2 (even the mandatory portion), it means I should expect a tax rate of 4.5 – 6.5%. Best Canton for my situation is Schwyz, with a tax rate of 4.5 – 5.5%. In my NW document I’m already taking this into account and expecting a tax rate of 5.3% (row 62).

Will it be worth to move my funds in Canton Schwyz? Well, we’re talking about 1 – 1.5% tax difference with respect current situation, i.e. a 3-4K CHF difference – hint: I don’t live in Canton Vaud 😀

I don’t know if it will be worth, I’ll think about it at withdrawing time.

That’s finally all 🙂

Enjoy!

2021-08 Update: I’ve found an amazing summary table on Finpension Blog, enjoy!

https://finpension.ch/en/capital-withdrawal-tax-compared/

Hello MR. rip,

Thanks for the great work and article.

To answer one of your question:

“Yeah, you have control over it. You can open a vested benefit account in a Canton you like and transfer your funds there. There are even institutions who can do that for you (with reasonable fees).”

That is correct only if you leave the country (so you will be “imposé à la source” where the fund is)

If you live in Switzerland you will pay the tax from your commune,canton+ federal

Yes, sure. Thanks 🙂

Will add that in the major review of these articles (they’re getting old and need a revamp).

Hi RIP,

I have a question on the buyback you mentioned in the article.

Let’s say that a person buyback in 2019 and leaves Switzerland for good within the next 2-3 years (within the 3 year lock in period), will he/she be able to withdraw the money in full after withholding taxes?

Thank you.

Buybacks (or buy-in) are to be considered in the extra mandatory portion, so one should be able to withdraw them if leaving the country even in the EU-EFTA region.

About withholding tax vs full income tax it depends on the holding period and the amount. If you buy-in today and withdraw tomorrow, you’ll be taxed as income even if “it’s different money” unless you’re below your Kanton’s threshold (in ZH is 12k CHF buy-in). If you wait 3 years you’re good to go. If you withdraw while you’re abroad make sure your country has a special agreement with Switzerland else they might tax the amount as income. For example, Italy has an agreement to tax Swiss Pensions at 5%. so even if your withholding is greater, probably you can get it back and just pay 5% Italian special tax on Swiss pension lump sum. Probably*

I have a question related to the buys in on the 2nd pillar. Does make sense to buy back early in your life, when the taxes are anyway lower, due to kids ( I have 2). Or better to buy back when kids are out of the house, salary is supposed to go higher with age, and you can save more taxes? What I mean is to have lower value pay back when young and above 50-55 to start have larger sum for the buy in.

It depends on the marginal tax rate you pay. If it’s >30% don’t think about it. Use the gap as early as possible. With a salary increase you get a gap to fill, so don’t wait for getting older.

Hi Jeremy, thanks for your comment. We live in canton zug and we have a total combined income ( my wife and me >300 chf yearly. However tax rate are not that high usually on the range of 40k per year. It’s well below the 30%, therefore I am not sure if the pay back makes sense or not.

The marginal tax rate is the tax you pay for every additional Swiss franc you make. It’s different from the total tax rate. If the marginal tax rate it’s way below 30% it doesn’t make sense you pay into your second pillar.

Understood, thanks a lot for the explanation. What about the 3b? I have been offered an education plan for the kids, using the 3b scheme. Does it make sense? Or better put those money into IB?

3b has no tax effect as far as I know, so it doesn’t make any sense to use it. Sure, IB or similar is much better.

Geneva sucks too, trust me.

Geneva is trash. Every Swiss knows that, and even tourists say that Geneva stinks.

Geneva is garbage. 🤮 I hate this city. Fuck Geneva!

Geneva can go fuck itself! 8====D