Hi readers,

I recently read an article by Michael Kitces I’d like to share and act upon it.

But before we get to the dinner table, who the hell is Michael Kitces?

Michael is a cool person I don’t have the pleasure to have met but I’d love to. He also has a Wikipedia page about himself! How cool is that?

On his website he defines himself as “a lifelong learner with a passion for sharing what I’ve learned with others” and it turned out that “my journey of learning and sharing led me somewhat randomly to the world of financial services“.

He is a certified financial planner that mainly helps other financial advisor thru his blog and his professional newsletter “The Kitces Report“.

He’s the kind of good financial advisor that it’s not a bad idea to listen to.

“RIP, is this a sponsored post? Are you getting paid to advertise this guy?”

Of course not 🙂

I’d tell you if I’ll ever host a sponsored content, which I bet I won’t ever do! Never say never though.

Anyway, Kitces is cool. I’ve read a dozen of his reports and most of his work on traditional and early retirement, safe withdrawal rates, sequence of returns risk, asset category correlation and Shiller CAPE. He’s one of my role model in the FIRE “researcher” community, like Big ERN.

How did I first hear about Michael Kitces?

He’s been a guest on Mad FIentist podcast episode 37 “The 4% Rule and Financial Planning for Early Retirement”. It’s been my favorite Mad FIentist podcast episode, along probably with episode 39 featuring Chris Hutchins “Why You Should ‘Retire’ Before You Hit Your Number”.

Both episodes focused on courage and were published around the same time. The Kitces one was about 4% rule being still safe, even too conservative. The Hutchins one was about what has become my mantra: once you’re almost there, you’re already there. 100% FI is necessary if you’re retiring and unable to produce any income, not if you’re young, passionate, creative and skilled.

You guessed right! When I listened to both those podcast episodes roughly a year ago I felt a strange torsion at guts level… was it the beginning of my midlife FIRE crisis?

I’ll drop here the Kitces episode. It’s more than an hour but totally worth. Enjoy!

If you’re like me, you also want to check out the Hutchins’ one. Enjoy again, see you in another hour!

Ok, welcome back 🙂

Let’s get back to today’s topic, which sadly it’s not the safe withdrawal rate – but don’t get mad, your favorite topic will be featured in one of my next posts.

As I said, I recently read a 2015 Kitces’ article about how to value social security benefits. It’s targeted for Americans close to traditional retirement but it got me thinking a lot and activated my financial nerd muscle.

I recommend you to read the article, but if you’re too lazy or don’t care much I’ll summarize here:

future cash flows have a present net value.

“Holy (spread)sheet RIP! You, the mastermind that in an old article wasted used 4 thousand words instead of just saying ‘efficient market hypothesis’ and ‘random walk’, you’re now dismissing a professional article in 7 words?? I’m speechless!”

Yeah, I’m studying how to be brief and concise 🙂

Anyway, the article is way more interesting than just that. It aims to show how to give a lump sum value to a future expected cash flow (like social security) for you to be able to compare two otherwise incomparable situations and tell which one is better. Like deciding to delay social security by a year or not.

The technique used is the classical Discounted Cash Flow, where each inflow and outflow event is discounted by a factor (usually expected inflation or opportunity cost) to present time. The algebraic sum of all discounted cash flow events is the Net Present Value.

As I said, it made me think. While the article targets traditional retiree at age 65 facing the decision whether to delay social security or not, the same analysis can be done for any future cash flow stream.

I’m thinking of Swiss Pillar 1 pension (and maybe the mandatory portion of Pillar 2 pension).

So far I wasn’t accounting for my (kind of) guaranteed benefit. But it’s there, it’s not going away anytime soon and we can all give a financial value to it so… why not?

“RIP, seriously? It’s going to be peanuts, you don’t control it, they may raise pension age, lower pension value and whatnot! What about inflation??”

Yeah, I know, it looks like a nerdy pointless exercise. But why not? I’m pretty sure it can be helpful to evaluate other (usually scammy) investment options and “insurances” in other circumstances. And btw, if you read the linked article by Kitces, at social security age the lump sum value of the whole social security is in the mid 6 digits (300k-700k), not bad I’d say 🙂

Plus, it’s a useful financial exercise to keep your mind awake. And yes, since I’m doing it now I want to share it on my blog! Got any problem?

“…”

Ok, cool! And of course when the laws regulating social security change I’ll need to redo the math and adapt my calculation to the new value. It seems a good thing to create a spreadsheet and just change few variables 🙂

Before getting too excited and jump to the funny math, let’s list all the problems and check if there’s a huge road blocker:

Problem: laws are subject to change.

Solution: we assume current laws. When the laws change we will change the model accordingly.

More Problems: that would require tracking laws changes, including for example Pillar 1 pension benefit inflation adjustments.

Solution: yeah, it may be time consuming and sometimes hard to do. I’ll check no more than once a year. If it will become too hard to track changes I’d give up.

Problem: future taxes are hard to predict. They’ll depend on future place of residence and maybe aggregate income/profits.

Solution: yeah, that’s annoying. I’ll be conservative and assume 25% taxes.

Problem: what about inflation?

Solution: I will discount everything to today’s dollars (actually Swiss Francs). I know current projected monthly pension is absolute, but I assume numbers will be adjusted with inflation moving on.

Problem: what about life expectancy? What if you don’t even reach pension age?

Solution: I’m going to assume an optimistic 30 years after pension age. Is it optimistic? Well, in every cFIREsim simulation I input 50 years of early retirement, which almost matches with 30 years of traditional retirement if I retire before age 45. I can also use trinity study to discount 30 years of standard retirement (4%). Remember that in this kind of planning, being optimistic with your life expectancy means stressing the system more and making it more robust. If I live less or will not reach pension age then my retirement success (not running out of money) would be easier to achieve. P.S. in Italy we use to make a superstitious gesture that I’m not going to describe here 😉

Problem(s): what about…

Solution: listen… there are so many unknowns, I know. But we have some data and the math is fun, trust me! I’ll be making conservative assumptions to avoid an eternal sadness sentence by setting high expectations. Kitces’ assumptions were easier than mine, like: “you’re already at social security age 66“, “you know the actual monthly payments” and “you have lower volatility on life expectancy, since you’re already 66“. Under those assumptions, Kitces calculated a lump sum value between 280k and 683k USD depending on average/maximum social security benefit and whether the retiree is male/female. It’s a lot of money!

Problem: “Hey RIP, you’re doing this because you want to cheat your way to cross ‘tha millioh’ this month, isn’t it?”

Problem: “Hey RIP, you’re doing this because you want to cheat your way to cross ‘tha millioh’ this month, isn’t it?”

Solution: go away noob! According to live data I’m there this month! Yeah, “seven digitz” kiss my aaaaaa… Ok, monthly salaries already accounted for but expenses till end of the month not yet, which means… well… maybe… let’s see… Ok, let’s focus 🙂

Why do I want to consider my Pillar 1 in my NW? Not just to cheat my way to the “twoo commaz“, of course. I don’t remember who I was talking with, but it was a FIRE seeker like me. It might have been MustachianPost, Sparkojote or someone else (a colleague?). We were discussing about issues of being an early retiree in Switzerland.

I remember saying “well, if you ER in Switzerland then one thing to consider is that you have to make Pillar 1 minimum payment of 478 CHF per year per person above age 20… that’s an extra tax…”

And my interlocutor said “…but that’s a good thing! You get 30-50 CHF/Mo forever starting at age 65! Good value for your money”

And I agree it’s a good thing. Well, things are more complicated than this, since according to the law “the amount in contributions for persons not gainfully employed is calculated based on their assets“. Apparently it’s cheaper to be self employed and earn less than 9400 CHF/Year. In that case you only have to pay minimum contribution of 478 CHF/Year and it seems a very good deal if every single year of contribution generates 360-600 CHF/Year after age 65.

Anyway, it seems a good deal but if I don’t account for it in my Net Worth document I’d only have a visible -478 CHF after the contribution. Which is not rational. Then I found the Kitces article and it clicked my nerd mind! Let’s do it!

Our Pillar 1 – and in general any defined benefit financial instrument like a pension, an annuity or social security – has a monetary value as of today. We can calculate it and include in our NW. Of course it will reflect current laws and we need to make several assumptions but it’s better than nothing.

I’m going to do the math for Pillar 1 only. Technically there are conditions for which one could cash out Pillar 1 and mandatory Pillar 2 benefits. Pillar 1 is almost impossible, unless you’re going to Puerto Rico or few other countries. Mandatory Pillar 2 is technically more accessible if you buy a house or fund a company with employees. That’s why I don’t lumpsumize mandatory Pillar 2 but I do lumpsumize Pillar 1. I definely don’t lumpsumize extra mandatory Pillar 2 and Pillar 3 since I can easily access them and take the money out (leaving Switzerland), pay lump sum tax, and invest it on my own. Btw, leaving my extra mandatory Pillar 2 in our provider hands to wait for the pension is not efficient and has a bad conversion rate of only 5%.

“But RIP, 5% is still better than your SWR! Why do you plan to cash Pillar 2 out (and pay some 5-7% taxes) instead of letting it generates 5% per year forever?”

We’re going on a tangent but ok, quick answer: first, I can cash Pillar 2 extra mandatory as soon as I leave Switzerland and invest at a pessimistic 3.5% yearly return for the next 20-25 years instead of waiting till age 65 and watching it grow by 0.5% per year. Second, at official pension age I won’t use a 3.5% SWR anymore. I’d be 65 and I’d go for 4% at least. And with a 5% conversion rate once I’m gone money is gone too. With the invested lump sum it’s likely that after my departure there will be more money than the lump sum itself. Plus, the 5% conversion rate is based on actual lump sum value and never adjusted for inflation! Bad, really bad.

So let’s do it for Pillar 1 only!

Where do we start? A good starting point is to take a look at how much we’re going to get at pension age with Pillar 1 contributions until today. If you have been a resident in Switzerland and ever contributed to Pillar 1 (AHV/AVS) you’re entitled to receive a pension at age 64 for women and 65 for men. The pension will be between Min and Max (=twice the Min), depending to your level of contribution on each year, assuming you contributed for 44 years if you’re a man or 43 years if you’re a woman. If you contributed for less than 44(43) years then your future pension is prorated.

Currently, Min = 14100 CHF/Year (1175 CHF/Mo) then Max = 28200 CHF/Year (2350 CHF/Mo). If you’re married and both contributed (or the only one contributing contributed more than twice the minimum each year, i.e. ~1000 CHF per year), the two pensions combined are capped at 150% of a single one, i.e. MaxCouple = 42300 CHF/Year (3525 CHF/Mo).

What a mess! Should we do all the math? Thankfully not, there’s an official online calculator named ESCAL!

Let’s assume we stop contributing by end of this month (August 2018) and see what’s our expected monthly pension at official retirement age:

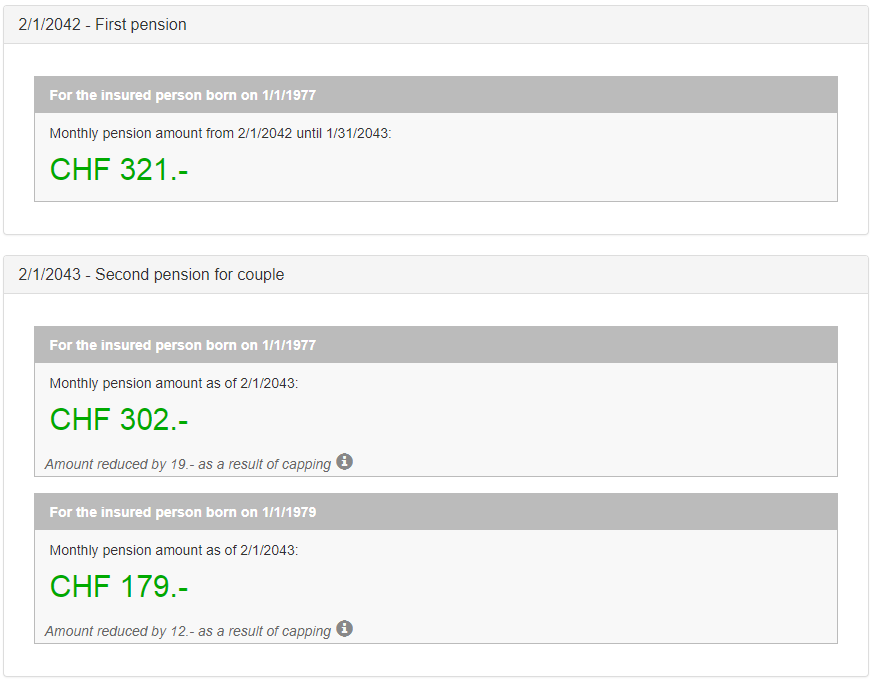

Birthdays are obfuscated, I picked January 1st for both, but birth years are accurate: 1977 for me and 1979 for Mrs RIP.

As you can see I’m reaching pension age in 2042 (LOL) while Mrs RIP will join me one year later even though she’s 2 years younger than me. that’s because pension age for women comes one year before (64 instead of 65). Excluding first temporary year we’re going to get 400 CHF/Mo, and that is assuming we stopped contributing next month!

This amount is in today CHF. At pension time it will be higher. According to official rules:

Adjustment for inflation: the pension amount or the increase of a pension in force is determined based on the pension index (hybrid index), which is calculated using 50 % of the nominal salary index calculated by the Federal Statistical Office and 50 % of the Swiss consumer price index

So we can more or less count on a purchasing power of 400 CHF/Mo of today CHF.

Now, before we move on, we can play a bit with numbers and see what happens for example if I’ll contribute for another year, until August 2019, while Mrs won’t work.

Now, before we move on, we can play a bit with numbers and see what happens for example if I’ll contribute for another year, until August 2019, while Mrs won’t work.

Ouch, that’s unfair! Why are we still getting 400 CHF/Mo??

Anyway, if I contribute more than double the minimum, i.e. more than ~1000 CHF/Year Mrs contribution should be covered. Let me check my Pillar 1 contribution last year… ok, we’re in the range of 10k CHF, she should be fine… plus she’ll take care of our kid(s) and care/education is covered.

Let’s try to change her contribution to end on August 2019 but edit her contribution amount to be zero during the whole 2019.

Let’s try to change her contribution to end on August 2019 but edit her contribution amount to be zero during the whole 2019.

Ok, now it’s more reasonable: 481 CHF/Mo.

It looks like we’re getting ~80 CHF/Mo increase in pension for each year of additional contribution.

It makes sense, since our MaxCouple is 3525 CHF/Mo and if you divide this by 44 years of maximum contribution you get ~80 CHF/Mo per year of contribution, assuming you make BIG contributions (greater than twice the minimum). So it doesn’t matter if she works or not, since my contribution covers for both. In fact it only changes the virtual split among the two pensions, not the total.

{kind=link}

Let’s see if it holds true for another year.

Let’s see if it holds true for another year.

Let’s set final contribution month August 2020, more or less our current FI forecast date.

Total pension: 561 CHF/Mo.

The rule holds.

Well, at least it holds while I make fat contributions.

Let’s see what happens if we stay another 2 extra years (until August 2022) but stop contributing (or just make minimum contributions) after August 2020. You can do that by clicking on “edit income”.

Let’s see what happens if we stay another 2 extra years (until August 2022) but stop contributing (or just make minimum contributions) after August 2020. You can do that by clicking on “edit income”.

Total pension 721 CHF/Mo.

Which is 160 CHF/Mo more than 2020, or 80 CHF/Mo more per year of zero contribution.

Huh? Shouldn’t be less than that?

What if I work until 2022 and contribute massively to Pillar 1 instead of lazily sailing to the Caribbean islands?

What if I work until 2022 and contribute massively to Pillar 1 instead of lazily sailing to the Caribbean islands?

Still 721 CHF/Mo.

It probably means that my huge contributions during these 6 years have an impact that lasts for several years.

I contributed much more than minimum and they probably don’t weight each year on its own, but sum the contributions and divide by the number of years and check whether the average contribution is above Max contribution. Or just maybe the online calculator is not reliable.

What if we keep contributing the minimum (2*478 =956 CHF/Year) for another 10 years, until 2032?

What if we keep contributing the minimum (2*478 =956 CHF/Year) for another 10 years, until 2032?

Total: 1522 CHF/Mo, i.e. +800 CHF/Mo compared to previous case. Still 80 CHF/Mo per year of minimum contribution.

Seems like something is wrong.

What about going all the way to official retirement age only contributing the minimum (since 2020)?

What about going all the way to official retirement age only contributing the minimum (since 2020)?

Total: 1682 CHF/Mo.

Ok, free lunch is over but with ~8 solid years of contribution at my salary we’re topping up Pillar 1 pension until 2032 at least. Which is cool assuming we could keep being insured and pay just the minimum while maybe we’re early retired in Italy.

Sadly it’s not possible with current rules… and as I previously said, it’s not clear if you’re allowed to just pay minimum contributions if you’re early retired in Switzerland, with a decent net worth and investment income.

Anyway, we can safely assume that each additional year we’re staying in Switzerland, whether we work or not, whether we contribute minimum payments or more, our Pillar 1 pension will increase by 80 CHF/Mo for each year of contribution.

Now, how to get the Net Present Value of this future cash flow?

I’ll do that in 2 steps and I’m going to explain my process in details.

First step is getting the Net Value at retirement age, i.e. how to get the lump sum equivalent of the future cash flow in 2042 (let’s simplify and skip the transitory first year).

A picture is better than thousands words

How to get that value? I’ll revert the 4% rule for that. That’s the perfect case for uncle Bengen and the guys from the trinity study!

So, with current contribution (2018) and current laws we’re going to receive 400 CHF/Mo gross pension, it’s 4800 CHF/Year. Minus 25% conservatively estimated taxes it’s 3600 CHF/Year, which is 4% of 90k CHF.

A lump sum of 90k CHF on 2042 is – for our analysis – equivalent of an annuity of 3.6k for the following 30 years.

I know the 4% rule assumes withdraws inflation adjusted, but that’s automatically done by the re-evaluation rule of Pillar 1 pension. The rule holds.

Now, how to discount those future 90k to today?

Now, how to discount those future 90k to today?

This is much simpler, it’s enough to choose a discount rate and apply for the 24 years left before official pension age.

The factor I choose is my current SWR, 3.5%.

Why? Because that’s my safe lower bound expected average growth (inflation adjusted) of investments left alone coasting for N years.

My SWR is my opportunity cost. I currently assume I’ll be fine taking out 3.5% of my NW per year, which is stronger than assuming that an amount invested and untouched will grow by 3.5% per year (+inflation) in the worst case, over such a long time frame.

90000/(1.035^24) = 39416

Net present Value of my expected Pillar 1 pension is ~40k CHF!

It means, if I take an amount of 40k CHF and invest it according to my asset allocation for 24 years it will become (at least) 90k of today CHF (nominal value will be inflation adjusted) in 2042. 90k CHF in 2042 is the equivalent amount to sustain 3600 CHF/Year inflation adjusted withdraws forever (for another 30 years at least).

This can also be done the other way around: if the Swiss government comes to me and tells me: “Listen RIP… good luck in your retirement country. But we don’t want to have you on our payroll forever. Here are 30k, please sign this document that you give up on your pension entitlement” I’d know how to reply to the offer 🙂

I made a calculator that you can use too 🙂 Just copy the spreadsheet and play with it!

Let’s embed it here:

In the second tab, named “playing a little bit”, I’ve explored how the lump sum would grow if we keep contributing. As we’ve seen it doesn’t matter if we just contribute the minimum or more.

For us, NPV value is 39.4k this year (2018), 49k (+9.6k) in 2019, 59.1k (+10.1k) in 2020, 69.9k (+10.8k) in 2021 and 81.4k (+11.5k) in 2022 and so on.

Assuming no change in the laws, with each contributing year our Pillar 1 pension NPV grows more than linearly thanks to several factors:

- We (sadly) get closer to pension age, i.e. money are coming sooner.

- We contributed one more year, i.e. our expected gross monthly pension grows.

- [Should be irrelevant] every 2 years pension value is adjusted by inflation and salary growth. This is not taken into account in the calculation because we’e reducing everything at today purchasing power of the CHF.

Now, before we go, let’s play with some variables. In Switzerland it’s possible to start withdrawing Pillar 1 pension up to 2 years before pension age (with a penalty) or defer up to 5 years (with a bonus).

Here’s a quick recap:

Would it be a wise choice to anticipate/delay pension age? Should we accept the early retir… HAHAHAHA!! Sorry… Is it more convenient to anticipate retirement by 1 or 2 years? What about delaying it by up to 5 years with a huge bonus?

Those are questions we can answer with our analysis, even though must admit that the 4% discount rate for “30 years pension horizon” doesn’t help in this situation.

With my model it’s better to delay pension as much as I can, since my opportunity cost is 3.5% while the Net Value at retirement age grows by 5.2% each year. But that doesn’t really scale, maybe actual life expectancy should be used instead, lowering actual Net Value at retirement age in case of a delayed pension and increasing it for an anticipated one. Or SWR could be increased with pension starting age, which lowers the Net Value at retirement age.

Let’s do the second one, increasing SWR by 0.2% for each year after age 65. At 70 I’ll be happy to take a 5% SWR since my horizon is probably more limited than the 30 years of the Trinity study. If I then make till 97 like my Grandpa, well, good for me! Pension won’t stop.

I’ve used our current situation (2018) and changed expected pension amount and Discount factor of pension payments (SWR at pension age).

Now, with my arbitrary discount factors it seems the optimal is to neither delay nor anticipate. But “Anticipate” is more appealing. Being more optimistic with investments and increasing the discount factor until pension age (expected investments growth, currently 3.5%, i.e. my early retirement SWR) lowers the overall NPV of Pillar 1 but makes “Anticipate” the winner.

Delaying becomes appealing if you’re conservative/pessimistic about investment growth. If you keep money in saving account expecting 0.01% growth, maybe you should consider delaying pension.

Ok, that’s all for today 🙂

I’m going to add Pillar 1 NPV to my Net Worth starting in January 2019, in the virtual section, to not mess up current metrics and forecast. And to not cheat my way to “Der Millionen” 🙂

“Hey RIP, late question: what about the mandatory portion of Pillar 2?”

I’ve said I don’t want to lumpsumize it, I’d rather account for it at its today take-out value (nominal value minus expected lump sum tax, i.e Kapitalauszahlungssteuer)… but ok, let’s quickly do the math 🙂

Right now (August 2018) my Mandatory Pillar 2 take-out value is roughly 35k CHF. Expected lump sum tax is 6%, so I could take out (if conditions are met) 32.9k CHF.

What’s its NPV? Should I take the money out (if possible) or not?

Current law forces Pillar 2 providers to offer a 6.8% conversion rate on the mandatory part of your Pillar 2, but this is probably going down to 6% with the big pension system reform of 2020.

Let’s do some math (you can play with the sheet “Mandatory Pillar 2 NPV” of the same spreadsheet):

Ouch, the NPV of Mandatory Pillar 2 is 19.5k, while I account for 32.9k… but it’s not the end of the story. I’m using a 4% discount factor of pension payments, like for Pillar 1. But while Pillar 1 pension is inflation adjusted, Pillar 2 pension is not! Let’s fix that by artificially increasing the discount factor to 5%:

That makes things even worse. NPV is now 15.6k! And we’re not done yet… see that 6.8% conversion factor? It used to be 7.2% years ago. Swiss government lowered it because it was unsustainable. And guess what, it still isn’t sustainable at 6.8%! the big 2020 pension reform will very very likely lower it to 6%:

Which actually makes withdrawing it as a lump sum at pension age better than converting to annuities, but still way worse than current lump sum value I account for 🙁

“… so RIP, are you going to change this one too in your NW? And maybe do some math for the extra mandatory Pillar 2 and Pillar 3, since you can’t freely withdraw them…”

Definitely not for extra mandatory Pillar 2 and Pillar 3, I can withdraw them as soon as I leave Switzerland or buy a house or start a company.

Mandatory Pillar 2 makes me think a bit but in the end no, I’ll keep accounting for it with its current lump sum value. It’s an actual account to my name, and there are conditions for which I can withdraw it now (paying lump sum tax), like buying a house or starting a company (leaving Switzerland is not enough, sadly).

“ok, you’re cheating but we like you RIP, so no worries 🙂 Are you going to consider yearly variations of Pillar 1 NPV as income?”

I’m not cheating! Ok, just a little bit. No, I’m not considering Pillar 1 contributions as income (while I do that for Pillar 2 contributions and employer match).

“Can we do all other analysis on Pillar 2, like anticipating/deferring pension age or see how the NPV grows with time?”

Yes, we could, but I’m tired and a little bit depressed by the numbers so NO. Do it on your own if you want 😉

That’s all folks!

Wow, it seems I am not a hardcore numbers nerd, still made it to the end. This is actually a fair system and your numbers are promising. In the worst case, only that ~500€/month can fund a life at some low-cost area 🙂 Also, it is good that you can make such calculations, I have no chance doing this for several reasons (changing laws, lack of data and information). According to some articles I dug about the topic currently in Serbia if you hypothetically go with a “realistic” scenario and have 30 years in work an through that period you earn the average salary (~600€/month gross currently) and pay the mandatory fees of 14% (your employer pays an additional 12%), then when you hit the mark (currently 65 for males, 62 for females) you can expect a pension of ~200€/month. It is a bargain, isn’t it?

same in Italy. Pension system has been destroyed each year since 20 years. Every year, pension age moves away 2 years and pension amount is cut in half. Add to that almost zero transparency and the highest national public debt in Europe and you can deduct your conclusions.

Luckily, Switzerland is more reliable, transparent and less populistic 🙂

Thanks for another great analysis! I’ve been following your blog for a while and it’s filled with very useful info. This one in particular is great as I always seem to ignore the pillar 1 in my assets NW, kind of on purpose given that the retirement age seems so far away and there are not that many decisions I can take on it, so I always delayed analyzing it.

However, in fact, I recently learned that I may be able to cash out some of my pillar 1 contributions if I leave Switzerland in the future. At least that’s the case as of now (who knows what happens in the future), so I knew I would have to do some kind of analysis at that point. Your ideas here are definitely a good starting point to compare cash out withdrawal vs future cash flow. In case someone else is already in this situation, this englishforum thread has quite some info on the cashout calculation: https://www.englishforum.ch/leaving-switzerland/272073-ahv-1st-pillar-cashout-success-story.html.

Thanks for the precious link!

I didn’t find that!

Going to add to my Swiss Pension System post 🙂

Welcome to retireinprogress 🙂

I am curious why you counted Pillar 2 annual growth to be only 0.5%? I have never gotten less than 3% with some years higher than that.

Maybe I am misunderstanding something?

Pillar 2 is out of my control.

Our Pillar 2 provider at Hooli is very conservative and it guarantees only 0.5% (essentially keeping up with inflation).

There’s a discussion happening these days whether to allow more aggressive plans like 1e but it’s a complicated matter.

Hello MrRIP

I am also italian but I’m based in the latin side of the röstigraben.

I started reading your blog two weeks ago and it’s really shedding light on many obscure points. Thank you!

Here’s my comment :

You may know that if you quit your job and won’t be working again you can transfer it on an account called “de libre passage” here in Suisse Romande. There are many foundations offering better performance than Hooli’s 0.5 %.

If you change a job your 2nd pillar capital should be transferred to the new company’s pension fund.

Some people transfer it to a libre passage fund when they quit a job to go on sabbatical and do not transfer it again to the new company’s pension fund thus benefiting of better performances.

I’m thinking on doing something like that.

What do you think about this?

Hi Escargot, welcome to the “right side” of the röstigraben 🙂

If you happen to come here ping me and we’ll have a chat!

Talking about the “vested benefits accounts”, which I think it’s the equivalent of your “de libre passage”, a friend of mine lost the ability to keep mandatory and extra mandatory pillar 2 separate, so when he moved to another country they didn’t let him withdraw the extra mandatory part of pillar 2. Maybe he did something stupid.

Anyway, it’s of course something I want/need to explore 🙂

Hi MrRIP,

Can you give more details about what happened to your friend? At which bank did he open the vested account? I was also wondering if one could use his 2nd pillar to reimburse a mortgage in Italy. Have you heard of someone who did that?

Btw it would be a pleasure to visit the “right side” of the röstigraben.

In which Canton do you live in?

I don’t know all the details about his Pillar 2 story, I might ask him (or he might jump in since he reads my blog).

I’m not aware of anyone who used Pillar 2 to finance a mortgage abroad, but according to AXA (page 3 here) should be possible but only if you move out for good: “An advance withdrawal or pledge for purchasing residential property abroad requires the owner to have his domicile there or to use it as the usual place of residence.”

But from what I found on EnglishForum maybe you’re only allowed to withdraw Pillar 2 for property/mortgage on the first month after leaving Switzerland and it may be taxed on your next country of residence as income.

Better to triple check with both your Pillar 2 / Vested benefit account bank and with your next country before doing the move.

Hello Mr RIP.

My plans to move out of Switzerland are pretty long term actually.

Those were really random thoughts.

Thank you for your answers!

Hi Mr. RIP,

I know this is an older post, but my wife just quit her job to take care of our child and has to do something with her pillar 2 pension. We are still staying in Switzerland so she obviously can’t cash it out, but what options does she have? Is there any way to have it invested in more equities? Currently it’s in a SwissLife account which is yielding basically nothing on an annual basis. I know you quit your job at Google relatively recently so I’m curious to know what you did with your pillar 2.

Thanks for your response

Of course there is.

Both Viac and Finpension (and many more) offer a so called “Vested Benefits Account” that can be invested as you wish.