Hi dear readers,

Today I’ve received at least 20 messages from people asking me a lot of questions related to the current market fall: “what to do now?” “are you buying?” “are you selling??” “are you celebrating that in November you sold a lot of stocks?” “are you StupidiFI plans holding?”…

It’s been an intense day!

Let’s write a quick impulsive post as a public answer, and some more 🙂

Plans are Useless

In preparing for battle I have always found that plans are useless, but planning is indispensable.

– Dwight D. Eisenhower

In early February, I sent my resignation letter to my manager. My last day of work will be March 31st 2020.

Ten days ago, on Feb 19th, I posted my “after Hooli” strategy. Ok, I actually published the post on Feb 20th, but it was 95% ready on Feb 19th. The market peak day. A kiss of death.

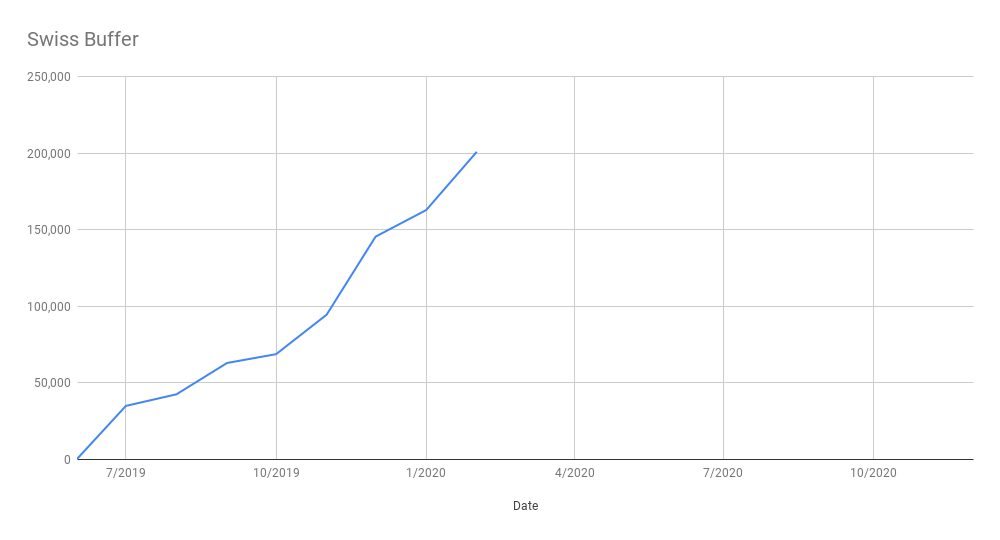

TL;DR: our plan is to stay in Switzerland without a salary while our Net Worth is above a certain threshold. The difference between current NW and the threshold is called The Swiss Buffer.

At the time of writing my last post, the Swiss Buffer crossed 200k EUR (215k CHF), i.e. 3 years of living expenses in Switzerland. February NW Delta was +41k EUR, also thanks to the fact that the EUR lost value compared to USD and CHF. I announced I crossed the 100% old FI goal of 1.2M EUR: I was 102% FI if we were to move back to Italy.

{kind=link}

I said “Wait… let’s celebrate! Hold my beer!”

I didn’t know the beer was a Corona.

9 days later, Feb 28th 2020

“Hey RIP, are you celebrating? You sold almost all your stocks in November, right? 🙂”

“Holy shit it’s been hard… I’m 70k below. What a shock! Maybe you were right about holding too many Hooli stocks 🙁”

“Are you buying, RIP?? I’m excited when market drops! You should be greedy when the others are fearfu….”

I KNOW IT!

I know it.

It’s all easy on paper.

Yes, I sold 300k of stocks in November 2019, and now markets are below that level.

But I still lost a shitload of money in just nine days, and I’m not happy with that.

Some number… in just nine days:

- Our Net Worth dropped by 60k EUR, from +41k to -19k. It’s not only due to Mr Market, Mr USD contributed as well.

- FI% dropped from 102.16% to 97.34%.

- What about the Swiss Buffer? Here you go:

“But RIP, you said you won’t even look at the graph for a year, until end of March 2021!”

YES, I’M NOT LOOKING AT IT.

Calm.

What Happened?

I don’t know, compared to November 2019 I’m less invested in stocks, but I suffered a huge hit anyway.

Even though my stocks investments are ~30% of our wealth, my portfolio is heavily unbalanced toward a pandemic event. My current stocks ETFs are:

- 46% VT (ACWI World): So far, so good.

- 30% VYM & VYMI (High Dividend Yield, US and Ex US): I’m ok with the fact this is tax inefficient, but in this situation high yield stocks performed even worse than the rest. I think that’s due to the fact that high dividend issuing companies are those who sell goods and services, which are being destroyed by anti-pandemic preventive measures.

- 15.5% EIMI (Emerging Markets): I’m extra exposed to EM, and that’s not exactly the best thing in the world when a pandemic begins in the country that constitutes a huge portion of the EM index: China.

- 8.5% invested Pillar 3A (mostly Swiss Stocks): Stocks that follows the high yield model. Btw, many pharma stocks, which might profit by a race to vaccination in the near future.

Plus, I’m heavily exposed to USD currency, which is not performing good as well.

Plus, one of my bonds is: “Emerging Market Local Government Bonds“. Its performances YTD? -7.5%.

How do I feel?

Mixed feelings, mostly negative ones.

I thought my new plan would give me peace of mind, but what’s currently happening is exactly the scenario I didn’t want to happen: a sudden drop of our buffer.

I’m a bit scared.

Luckily I have room to rebalance, and a lot of cash to “buy low”, but as we all know: when will the market bottom? Nobody knows.

I also received messages from people who are excited about the market drop! Maybe that’s my game now that “I’m rich”, and I should learn how to “be happy about that”.

And forget that of course the three people who contacted me, excited for the drop, are 30 years old or younger, with a NW less than 10% mine. And without a dead career.

Anyway, who am I to judge? The net effect of all my attempts to time the market has been negative so far.

Time will tell.

What do I plan to do?

Well, the original plan is still in place.

I’m scared, but we still have 140k EUR of buffer (plus, last Hooli salary in March will be larger) and 13 months of grace period. After that, if the market keeps going down, we’ll be walking on a thin ice.

We’ll face it if/when it happens.

In the meantime I should also stick with my plan to do Dollar Cost Average 20k EUR per month into stocks, mostly VT, as resolution of my November 2019 investing paralysis.

But… oops!

I’m trying to buy the dip (which is not wise: take a look at this amazing article by Michael Batnick) but what I’m actually doing is Catching the falling Knife.

In January I’ve invested my monthly 20k at the end of the month. I wanted to do the same in February. But I saw a dip and decided to anticipate the planned move.

VT peak share price has been 83 USD. As soon as it fell below 80 I purchased my monthly dose: on Feb 24th, I purchased 273 VT shares at 79.50 per share (21.7k USD).

Good 🙂

Nope.

On Feb 27th price dropped below 75, and I bought 300 extra shares at 74.58 per share (22.4k USD).

Then today, Feb 28th, I purchased another 100 shares at 72.45 (7,245 USD).

I’ve invested 50k USD in VT in last 5 days.

Current snapshot price on IB is 72.83.

I’ve Chicken in!

I don’t know what I’m going to do in the following days, but for sure:

- I’m not going to sell for any reason.

- I’m not going to lower my desired cash cushion of 150k CHF.

- I’m not going to invest into stocks more than what I account for in my Investing sheet. Current ideal Asset Allocation is 50/50 stocks vs bonds, and even in that conservative AA I still have plenty of room for stocks investments: 157k EUR.

- I might decide to switch to a more aggressive AA (60/40, 70/30) but only if the drop will be very large (30% or more) and all my rebalancing power had gone. Not sure though.

- I might sell EIMI, but I’m not sure. Well, this year I don’t fear being classified as a professional investor… I would actually want that privilege and be able to deduct losses from 2020 taxes!

I’m curios of the dividend yield of Q1 2020. Most of my ETFs distribute quarterly dividends, I’m waiting for them. If companies have not been impacted much by the virus thing maybe it will be time to double down and buy more. Let’s see the impact of the global fear and all the preventive measures on the real economy. Are we able to self inflict a recession?

Anyway, the plan is still active. It’s actually not started yet: I’m still an employee and receiving a salary.

“RIP…”

NO.

Before you ask: no, I’m not thinking about staying at Hooli any longer. Even if I would, I don’t think I actually could. My resignation is final.

Black Swanning

A (lucky) guy named P, who’s part of my Coaching Program, sent me an email about my plan: “it seems you are planning not to win but to try not to lose… does it make sense?”

Yeah, kind of. it’s been like this for my entire life.

But I’m not alone: Avoid the Zeros is Warren Buffett wisdom, as mentioned in this amazing post by Nick Maggiulli.

I’m always planning for the worst case scenario in the desperate attempt to feel in control of everything. Maybe in the even more desperate attempt to catch Black Swans before they come.

Anyway, P’s comment made me think.

Am I trying to be smart by chicken back in? Probably yes.

Is this carrying a positive expected return? Probably no.

Why am I doing it anyway? Because of my cognitive biases.

Good.

Fun fact: I thought I coined the term “Black Swanning” but I found it exists in the Urban Dictionary and it means… something that has do to with sex… holy crap NO NO NO I didn’t mean that!

There’s More to That.

I planned to blog about other things: I have a half written post #1 in a series on “bonds investing”, but I didn’t find motivation to finish it today.

I’ve been slacking off the entire day instead of working on that post.

But it’s not been a complete waste of time: I’ve read so many – so many – posts of my new favorite blog of 2020: More to That.

I know, it doesn’t fit this post but I wanted to share it here anyway 🙂

I’ve read:

- Money is the Megaphone of Identity: a deep dive into how wealthy you actually are that will twist your way of perceiving money and confidence.

- The Riddle of the Well Paying Job: why compensation can’t compensate for a job you don’t like.

- How Natural Selection Screwed Us: a deep dive into the Resistance, the primordial brain, and its misalignment with our superior mind.

- The Quest to the Unlived Life: in my opinion the best post on the blog! It’s talking about me, about my Resistance (Laziness, Self Doubt and Uncertainty). Do yourself a favor, and go read it!

- Travel is no cure for the Mind: hedonistic adaptation explained in the best way possible, plus philosophy.

- The Economics of Writing: start your writing gig. Now! it’s the best time in history!

- The Release Ratio: the world is full of amazing content to view, listen, read. Just… do yourself a favor and create something as well. Don’t just consume.

I plan to binge read all his remaining posts, and – according to his suggested Release Ratio of 1 – write full notes and reflections about them for my own knowledge building.

Walklogging

About creating, producing content: I’ve been “drafting” this post entirely via audio. I’ve took a long walk during my way home today, and started recording notes. Speech-To-Text is amazing these days!

I went home, and found a lot of material ready for this post. This may be my future of post drafting!

Of course, you can’t do research this way, and your train of thoughts is not perfectly shaped… but I like it, and I’ll do it more often 🙂

Please, have a beer

![]()

Of course I don’t have any factual knowledge about this virus. I don’t know where it’s going. Where we’re going.

My gut feeling is that it’s not as bad as market and governments are telling us.

Maybe we already paid our due to it: BabyRIP has been 5 days sick with fever at 40 degrees and a lungs infection after a quick travel to Rome, before the virus was cool. Now in Italy it’s circulating the hypothesis that maybe the virus was there since January. Maybe she already got it, and she’s now 100% ok. My nephew has been 10 days in the hospital with – you guessed it right – very high fever for a week and a pneumonia. In early February. In Milan. Yeah, not cool.

Maybe we faced the virus without knowing it, and it passed.

And maybe this is just Survivorship bias.

But mortality rate is close to zero for anyone below age 50.

Containment might be useless at this point.

I don’t know, I hope that all we’re doing with quarantines and panic sell-offs is not making things worse.

But I know nothing.

Lessons Learned

Find your risk tolerance.

Get to know yourself better.

Investing is a psychological game.

Stick with a strategy.

Volatility is a fucking beast.

You can’t predict Black Swans.

Enjoy the rollercoaster guys 🙂

Hi RIP,

Thank you for this post with your views and feelings regarding this latest market drop. The important thing is that you are well and your family also. For all other things, financial I mean, time will fix everything and do whatever makes you fell sleep better at night. That’s what I did and no regrets.

Regards,

Luis Sismeiro

Thank you Luis for your kind words 🙂

Today China had only 8 new cases and 0 death, while Switzerland had 7. The virus almost disappeared in China, but the developed world became crazy with it. It is too late now to stop traveling or to cancel meetings. They should just ask 70+ year old people to stay at home, since 80% of the victims have that age.

The market needed a correction and this bad new was the trigger.

I don’t know where you are getting your numbers, but they are fantastically false. China reported 573 new cases (Feb 29th, 2020) which is up from 427 the day before. Please spend few minutes to do some basic research (googling) to avoid spreading false information.

Source: https://www.reuters.com/article/us-china-health-cases/mainland-china-reports-573-new-coronavirus-cases-on-feb-29-idUSKBN20O142

Yes, I agree there was a timing issue on the live website I used (ie a new day started in china) . Still the number of new cases is decreasing in china and there are many reports that the virus targets mostly long time smokers, who are mostly old men in china.

https://www.webmd.com/lung/news/20200226/coronavirus-top-targets-men-seniors-smokers

I get my information from https://www.worldometers.info/coronavirus/ and sometimes they lag a bit behind… or maybe governments are slow to communicate cases.

While it’s true that in China the spreading is being kind of contained (I don’t know how much to trust their publicly shared data), sadly the new cases worldwide are growing at an exponential rate.

I think no matter what governments do, most of us will be exposed to the virus sooner or later.

I enjoyed your post as always RIP, I think everyone is pondering what will happen with the virus.

Lot’s of swiss people that I talked to last week still thought that they can “close the border” easily. It quickly became obvious that unless you are North Korea, closing the border in a global world does not really work.

There’s no way to prevent the spreading. Full stop.

Now is a time for traders and a hard time for investors. Buy the dip or catch the falling knife. That sums it up very good!

Good point. Investors are biting their nails and waiting.

The problem is that what’s happening on the markets is not only emotional / speculative, but it’s very real: companies are suffering the pandemic and losing revenues. This is real. The markets overreacts as usual, but I’d bet we’ll see a decline in Q1 earnings almost everywhere.

Ouch, that drop has got to hurt, but imagine if you hadn’t pulled out in November.

Keep calm and carry on – I know it’s hard for Italians not to worry, it’s in their passionate blood 😉 But is it worth the high-blood pressure playing with a game of dice? Especially when if you lose from an active decision, you’ll feel even worse. Maybe the best thing to do is ignore it and carry on like normal? – I know this is probably hard due to your shifting work life. But remember, even if you didn’t really want to, you could easily pick up a contracting gig for one month and make back a lot (if not all) of your losses! You have the power as you’re awesome! You’ll always be OK.

Haha thanks SavingNinja!

it’s a sum of effects in my case: a large nest egg (–> bigger losses), having sent the resignation letter (–> end of fast accumulation phase), bad sequence of returns right at the beginning, burnout, and being fucking old at age almost-43.

If I were 25yo with a NW of 50k and a fresh new exciting career ahead of me I’d be drinking Champagne right now and hoping for a new 1929 😀

Thanks for sharing the statistics website.

This site is indeed very interesting! (not only the corona related stats)

I find it very factual and a good aggregation point for all you need to know about the Covid-19 (we should not call it “coronavirus” because it’s a family type, not a virus type).

Thanks for the post! Out of curiosity, what do you mean by “young people without a dead career”? Why do you consider your career dead? Just because you quit this month or because you think the industry is in decline?

I do consider my career dead.

The industry is still strong.

Don’t underestimate yourself. It is not because you need some time off that your career is dead. You still have your education and your experience, which put you well ahead from the new graduates. Try to join some hackaton (there is hackerx in Basel end of March and I can still probably send you an invite) or IT job forum and you will see. Even if you are not actively looking, it will be good for your well-being.

Thanks Joel your your kind words 🙂

I know I can’t see it clearly right now, but my perception is that my Engineer career is dead.

Maybe there are things I can do to resurrect it, or use it as a leverage (training, managing people, mentoring) but my main 250k/Year career is dead.

I believe you’ll be just fine 😉

At least your humor is still intact!

You have to be able to have a little laugh at situations like these (which you clearly are – I love your writing style!). I’m not entirely sure how long you’ve spent accumulating your current NW, but at 43 you’ve still got 50%+ of your life left to live. That’s a pretty sweet achievement! 99% of the people on the globe is never going to achieve that (not because they can’t, but because they wont or don’t know how to)

Think about hose poor people who has been working 60 years in jobs they hate, just to make ends meet (even in retirement).

In the greater scheme of things, you’re doing pretty awesome! Who cares if you “lose” 70K or 7K in a week. You’ve got enough, and in the end the market always go up. You know this.

I would most likely be shitting myself too, if I was in your shoes, so kudos for having a drink (a Corona none the less – f*ck that stupid virus) and a smile 😉

There’s always money in the banana stand! (In this case a euphemism for Corporate IT consulting).

Ps. This is why I don’t do stocks! 😛

Thanks Nick, but I don’t share your optimism about my life expectancy 😀

A trick that is helping me these days (more on spending and wealth, not on investing) is the following: am I scared that we spend 6-7k CHF per month and our wealth is 1.3M CHF? How would I feel if we had 130k and were spending 600 per month? Well, I’d feel immortal and super rich. And that’s exactly how I should feel right now. Then the virus came and our wealth is being impacted as well