Table of Contents

Hi RIP Friends,

This is the second post in a short three posts series about my experience with a Financial Advisor. Your can read first post here, where I explained how I was cold contacted on LinkedIn, and what happened during our first 1h-long video call.

Let’s call The Advisor’s consulting company MCDD, which is not its real name.

The Advisor sent two Structured Notes factsheets to me few weeks after our call. She claimed that these notes were issued exclusively for MCDD customers, and that they were especially suited for this “uncertain market times”. But it was an obvious lie. As we’ll see, the two Notes she shared with me perform way better in low volatility environments. Also, the notes were created exclusively for MCDD customers but… MCDD is never mentioned in the factsheets! Not a great start.

I received the factsheets a couple of days before the October meetup with fellow Mustachians in Zurich, and discussed the products with my dear friends Mr. Cheese an Julianek, in front of a (couple of) Beer(s). I thank them for their inputs and the interesting conversation 😉

Also note: the Structured Notes subscription deadline was end of September, and I received them after the deadline… maybe she intended to just show me the “kind” of products, not the actual ones she wanted me to invest in. I don’t know, I forgot to ask. Again, not an amazing start. She was supposed to be a professional with 20+ years of experience in giving financial advices.

Another thing to note is that I received the Factsheets, but not the actual Prospect Documents. Sadly, the Factsheets don’t mention fees and other nuances and technicalities of the investment, which could be a place where the devil hides. Like currency conversion fees, reference currency, asset currency, call risks, and so on.

I won’t tell you much about my conversation with the Advisor like I did in the previous post, it wasn’t a deep conversation. I showed my perplexities to the Advisor in our follow-up meeting and she quickly moved on trying to sell my the next crappy product, the Insurance Policy Pillar 3A/B that we’ll see in next chapter.

I kind of regret having been so direct with her in this second meeting. I would have loved to see the Prospect documents, shame on me for not having gone for it. This post would have been much richer if I had gone close to sign a concrete proposal.

Anyway, I how you enjoy this deep analysis of the Structured Products I’ve ben offered.

Have fun, and let’s get started! 🙂

What is a Structured Note?

The best definition I’ve found is the following, from a Singaporean government agency website:

A structured note is a debt product whose return is linked to the performance of one or more underlying assets or benchmarks. It may be the interest that is payable on the structured note and/or the principal repayment, that is linked to the performance of the asset or benchmark.

(also check the Investopedia definition here)

Essentially, you’re buying a debt obligation with a financial institution (usually an investment bank) that we’ll call the issuer. You lend your money to them, and expect a future cash flow that depends in a nonlinear way on the performances of a basket of assets.

I know, it’s complicated, and this should already be a yellow flag.

It’s complicated for the average investor, but not for someone who likes to think in bets, and who adopts a probabilistic thinking approach in financial decision making. In the end it’s not rocket science, but average people should never ever ever EVER invest a Dollar on products like these, because you should not invest in what you don’t understand, right?

Ok, good.

There are infinite types of Structured Products, you can essentially reproduce whatever risk/return profile you want. In this post I can’t possibly cover every single type of structured product. I’ll just analyze the actual Notes the Advisor shared with me.

If you want to know more, I recommend the Structured Retail Products website.

RIP Notes

They offered me two similar products. Two notes with the same structure and reward profile.

Both of them had the following structure:

- I invest X USD (or GBP, never CHF) in their product before the given Strike Date.

- The product defines a Final Valuation Date (4-6 years), i.e. the duration of this debt obligation.

- I will get Quarterly or Annually coupons (very high, 10-17% annual yield) if the price of the lowest performing asset in their basket is above a Trigger Value (95-100% of Strike Price).

- At the Final Valuation Date I will get back 100% of my principal if the lowest performing asset price is above the Protection Barrier (70% for both Notes). Else I will get the performance of the worst performing asset.

Plus there are two other features (Autocall and Memory) that I will explain while analyzing the first Note.

Simply stated:

- You get quite high “dividends” (10% or above) if none of the assets in the basket performs particularly bad.

- You don’t get any upside benefits if some of the assets perform exceptionally well.

- You get the downside effects of the worst performing asset in case it performs particularly bad.

Here follow a few consideration before we take a look at the actual Notes.

First thing that comes to my mind is: you want to have a small basket. You’re linked to the worst performing asset in the basket, so the less they are the better it is for you.

Let’s assume a Protection Barrier of 70%. If you have a basket of 4 stocks, and 3 of them perform spectacularly well but one drops by 50% you’re doomed. You won’t get any coupon, and the capital returned to you at the Final Valuation Date is 50% of your initial investment.

What happens if one of the assets goes to zero? You guessed it right: you’re screwed even if the others were Tesla, Domino’s Pizza, and Bitcoin 🙂

You have to eat the worst apple in your basket. The more apples in your basket, the easier it is that one is rotten.

Second, you want correlated assets in the basket.

Let’s assume 20% of the world population don’t like RIP Pizza (how dare you!!). And let’s assume that the likelihood of a person craving for RIP Pizza is correlated with their culture, their eating habits, the fact that their circle of friends like RIP Pizza or not. So you get “clusters” of people who like RIP Pizza and clusters of people who don’t. Maybe we discover that RIP Pizza is very popular in Indonesia, but it’s hated in the Philippines.

What are the likelihood that taking a sample of 10 people in the world everybody loves RIP Pizza?

If you take 10 random people, despite the fact that RIP Pizza is incredibly popular (80% of people loves it), there’s only a ~10% chance that each one of the 10 random people loves it, i.e. 0.8^10 ~=10.7%.

What if instead of taking 10 random people in the world, you randomly select just a person, and then take the remaining 9 people in the same neighborhood (same culture, maybe close families, maybe friends)? What are the odds of all of them loving RIP Pizza?

Well, taken to the extreme, if you take 10 people who have the exact same opinion (correlation = 1) the odds that all of them like RIP Pizza become 80%! Same odds of an individual liking RIP Pizza.

And if you’re the cook who’s been told “You’re fired if I find even a single person that doesn’t like your Pizza among the next 10 customers“, trust me: you want the highest correlation possible 😉

I think this is crucial in understanding this kind of products.

Third, what about anti-correlated assets?

They’re a death sentence for your Note.

Having assets that “if X goes up, Y goes down” in your basket, and having your performances linked to the worst performing asset is a suicide strategy.

Like having a basket of 3 Pharmaceutical companies racing for a Covid vaccine (yep, take a look at my second Note)

Brace yourself, Notes are everywhere!

Yeah, three tech companies in a winner-takes-all industry, after an incredibly long bull market 😉

I think this is the way to bring dumb money to the table, and let the asset bubble explode.

Pump and Dump is coming, babe!

Anyway, let’s take a look at a concrete example, my first Note:

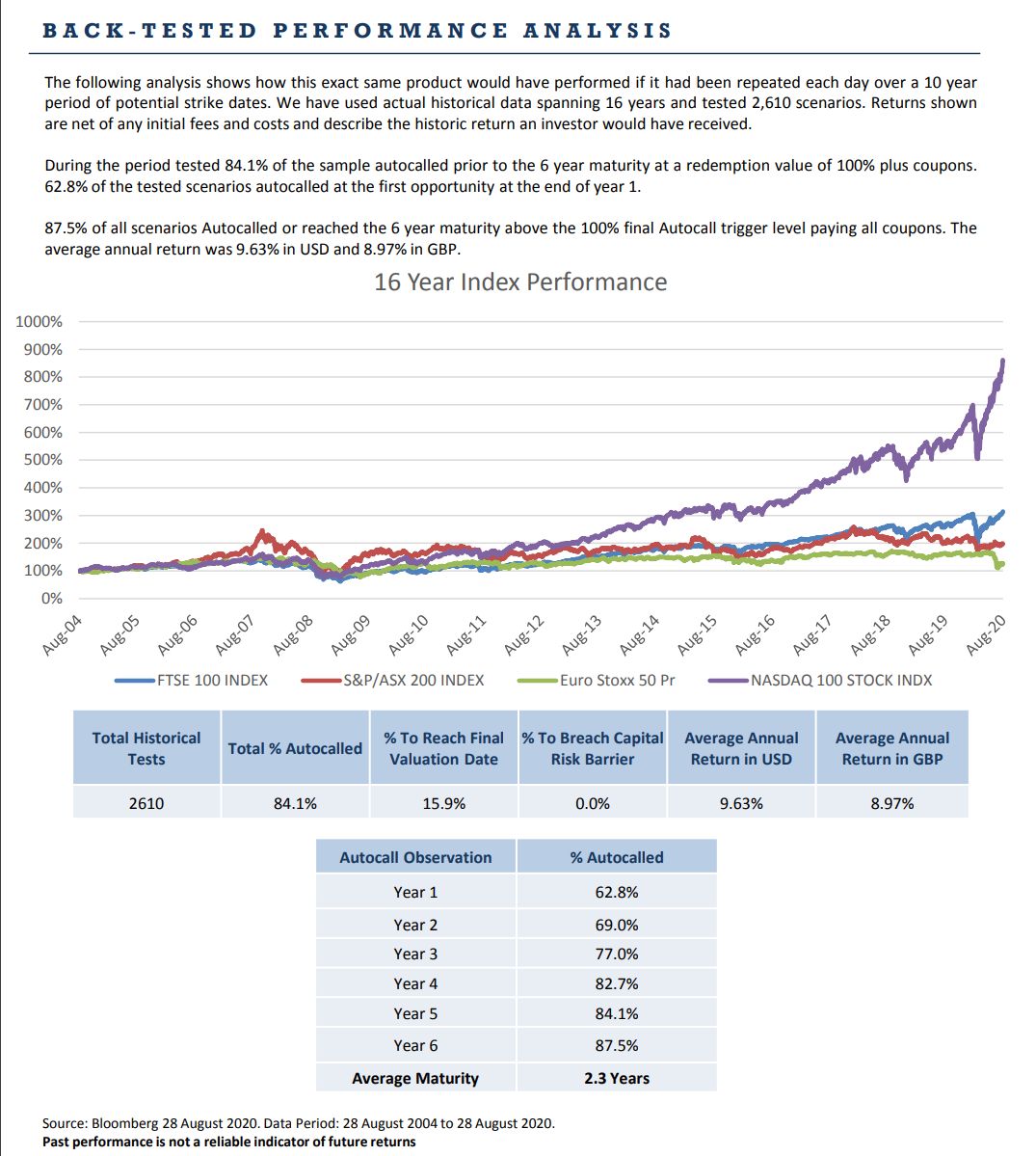

Note 1: Yearly 10-11% Coupons, Basket of 4 Stock Indexes

Before we even start: who am I dealing with?

This Note was issued by a Canadian Bank (CIBC), and proposed to me by the Advisor, who works for MCDD, the consulting company. The factsheet is produced by an intermediary brokerage firm (that I censored here) that, on their website, “seeks to add value to our institutional clients’ investment decisions“, i.e. there’s another middleman who’s going to take a cut.

How many middlemen there are? This is another thing to keep in mind: in a low yield world, any hand who comes to grab a 1-2% or more is going to kill your returns.

This Note is offering a 11% yearly coupon in USD, or 10.25% in GBP. It a very high dividend. You’re not getting such a “passive income” from your Dividend stocks, or from your S&P500 ETF.

As you can see it’s a tempting proposition: in a low yield world, where people and their financial advisor & retirement planners are craving for a “fixed income” solution that guarantees a 3-4% per year, a solution that promises a 10%+ return catches a lot of attention.

Plus if the excrement hits (gently) the ventilating system you still get 100% of your principal back, since the Protection Barrier is 70%. It means that even if each one of the 4 assets in the basket loses 29% of their Strike Price, you’d get 100% of your principal back.

Sounds good, right?

Well, it’s much more complicated, and the “good parts” of this Note end here.

Let’s take a look at the return of the Note compared to the return of the worst performing underlying asset, assuming the Final Valuation Date was just one year later:

As we saw, below the Protection Barrier (70% of the Strike Price) your Note performance is the same of the worst performing asset.

The range between 70% and 110% is very interesting: you get better performances than the worst performing asset: between 70% and 100% (the Trigger value) you still get 100% of your invested capital, and above 100% you get 110% (capital + coupon), which is a better return than the worst performing asset (if it performs no better than +10%).

You don’t get any extra benefit if the worst performing underlying asset performs better than +10%. If it doubles, you get only the 10% coupon. It has limited upsides. But not a bad limit, we’re talking about 10.25% in GBP (or 11% in USD).

Let’s enlarge the picture to take into account 10x and a 1/10x performance of the worst performing asset. Let’s imagine the worst performing asset is a company like Tesla, that could easily 10x (been there, done that) or be decimated:

Yep, now it sucks… you get all the negative effects, but if your asset “10x”s you only get +10%.

Here’s the logscale, where you can better feel the pain of the negative returns:

Mind that I don’t think the underlying/return profile is bad per se.

You know what? I’d take it if we were talking about a single, low volatility asset like an Index! I’d take this profile on S&P500 anytime you offered me!

I expect a yearly return on S&P500 to lie somewhere between -50% and +50%, with an historical average nominal return of +10% (there are more positive years than negative ones).

No wait, the historical 10% return for S&P500 is the nominal average total return of the index.

It’s important to mention that the underlying assets of this Note are NOT total return indexes, they’re just indexes. They get partially smashed by dividends. While S&P500 total return historical average nominal return has been 10%, the historical average return of the S&P500 has been 8% without dividends. We don’t get any dividend by owning the Note, and the reference performances are not accounting for dividends! Very bad.

Fun fact, the Note issuer is incentivized to discourage companies stock buybacks programs, and maybe suggest them to distribute larger dividends 🙂

Anyway, as I said I would invest in a Note with the above profile on a basket of a single asset with low volatility like the S&P500, especially in this – in my opinion – inflated scenario.

The medium-long Duration of this Note (6 years) reduces the probability of falling below the Protection Barrier of 70%, and the Memory feature will provide me all the returns I’ve eventually missed while the Note was under water. Where should I sign?

The problem is that they’re not offering me this Note on a basket of a single low volatility asset. The basket is composed of 4 indexes:

- FTSE100: Market Cap Weighted 100 largest companies in UK.

- Euro Stoxx50: Market Cap Weighted 50 largest companies in EU.

- ASX200: Market Cap Weighted 200 largest companies in Australia (funny, 200 from AUS, and only 50 from EU).

- Nasdaq100: Market Cap Weighted 100 largest companies listed in Nasdaq Stock Exchange (mostly Tech stocks).

What’s the problem with this basket?

First of all, it’s a large basket! There are 4 assets… the likelihood that the worst performing won’t hit the Trigger Value (or would fall below Protection Barrier) is non-negligible.

Second, they’re uncorrelated. They had to play hard to find uncorrelated assets in a global market, but we can assume Australian, UK, EU, and US Tech stocks are as uncorrelated as large cap stocks can be. It could have been worse, like adding “small cap indexes” in the basket (small cap stocks are less “global”, so geographically separated markets are less correlated), but it’s already enough of a bad deal.

Third, their currencies are uncorrelated. EUR, GBP, USD, AUD. Let’s not forget that your “worst performing asset” will be measured in a reference currency (GBP or USD), while the assets in the basket are tied to the whole set of 4 currencies! This increases volatility, which is bad for our Note. Ok, this is partially mitigated by the anti-correlation between currency performance and the large cap index in the same market (since profits made abroad are worth more in local currency). If the AUD drops 50% compared to USD it’s more likely that the ASX200 companies make good profits abroad and that the index goes up by a lot (in AUD). Anyway, your Note is measured in USD or GBP… if the USD goes up (when? when???) the odds of an Australian or European, or UK index not meeting its strike value (in USD) grows.

Fourth, this is a Structured Note whose underlying/return profile is suited for a neutral market, and I have trouble considering current stock market “neutral”. According to Structured Retail Product Academy there are products for bullish markets, bearish markets, neutral markets, and for several goals like capital protection, yield increase, leverage, and so on.

So far, not so good.

But there are two features that could make the Note look a little bit better: Memory and Autocall.

Memory

The Memory feature means that if at an observation date, i.e on every Note’s Birthday, the worst performing asset’s price is below Trigger Value (100% of its Strike Price, according to this Note’s Factsheet) you don’t get the coupon but the coupon itself is not lost (yet): it’s accumulated somewhere. Once/If the Trigger Value is met (at an Observation Date, not infra-dates), you get paid all the coupons you missed.

Ok, not bad. Kudos.

Autocall

The Autocall feature means that if at an Observation Date the Trigger condition is met (worst performing asset above 100% of strike price), the Note would redeem immediately, and you’d get back 100% of initial capital plus all the “memorized” coupons.

Cool, I won’t have to wait until Final Valuation Date!

This is a good thing, isn’t it?

Well, in theory it should be a good thing. You get all your money back (plus coupons) and then you decide if you want to invest in another similar product again. Of course maybe future Notes won’t be so generous with coupons, but the opposite might be true as well. Hard to tell.

In practice, this is a nice strategy for the middlemen chain to charge extra fees to you. You keep paying subscription and currency conversion fees every time you re-invest your money.

Imagine this realistic events flow:

- You have 100k CHF ready to be invested in this Note.

- Intermediaries take 2%, so only 98k CHF gets wired to the issuer.

- The issuer doesn’t know what to do with CHF, the Note is listed in USD. your 98k CHF gets converted in USD with another 2% currency conversion fee on the issuer side. You now have 96k CHF converted in USD (more or less 1 Billion USD) invested in this Note.

- Everything goes well, and one year later the Trigger Value is reached! Yay!

- They want to wire you 1.11 Billion USD, i.e. the original Billion plus the 11% coupon. Which is 106.5k CHF (96k + 11%), assuming USD didn’t lose another 10% compared to CHF in the meantime…

- On your bank account you only see 104.3k CHF, because your bank took another 2% currency conversion spread.

- Then tax declaration day comes, and they don’t give a crap about your double currency conversion losses. Your asset generated 10.5k CHF nominal profits (106.5k – 96k), and this profit is getting taxed as income (no Swiss tax-free capital gain), at your marginal tax rate, on top of your salary. Say 25-30%. Another 2.5-3k CHF gone.

- You end up with 102k CHF, a 2% Real Profit instead of the promised 11%

Mind that we’re assuming a stable CHF to USD conversion, and the worst performing asset in the basket closing the year above 100% strike price in the reference currency… this is an optimistic scenario!

Ok, maybe you’re Fin-savvy enough and you have a cheap way to handle USD or GBP directly, like I do: I have a USD denominated bank account with PostFinance, and I use InteractiveBrokers are a cheap currency conversion engine. So maybe you can skip the double currency conversion fees… but you won’t escape taxes and middlemen fees.

According to Mr Reset, who’s been scammed by the same advisor company (MCDD), they take 2% each. I see three entities involved in this Note. Maybe not all of them take a 2% fee (that would be outrageous), but I won’t be surprised to discover that the total intermediary fees add up to something like 3%.

So the Autocall feature might be a double trap: first trap is that you see the money immediately. You paid 100k, and after just one year you have 104-108k (before taxes) back. It feels good, so you buy Notes again, and buy more. Second trap is that you were promised 11%, you actually have to take into account intermediary fees, currency conversion fees, currency fluctuation risk, and taxes. It will be a miracle to keep half of the promised return, and we’re exploring the scenario where everything goes well on the performance side.

The overall conditional cash flow for this Note is the following:

They also added a backtest for this Note that goes back 16 years. Well, of course every structured product you’ll see would have performed amazingly on past data. I mean, this is the kingdom of cherrypicking, in both basket components and backtesting dates.

{kind=link}

I bet there are entire datacenters running code to find and film someone who flipped 10 consecutive heads on a coin, and to build structured products on him 😀

I’m actually thinking that maybe basket components are picked just to look good in backtesting while granting enough confidence to the Note Issuer that things will go well for them.

Anyway… Before jumping to conclusion let’s take a look at the second Note.

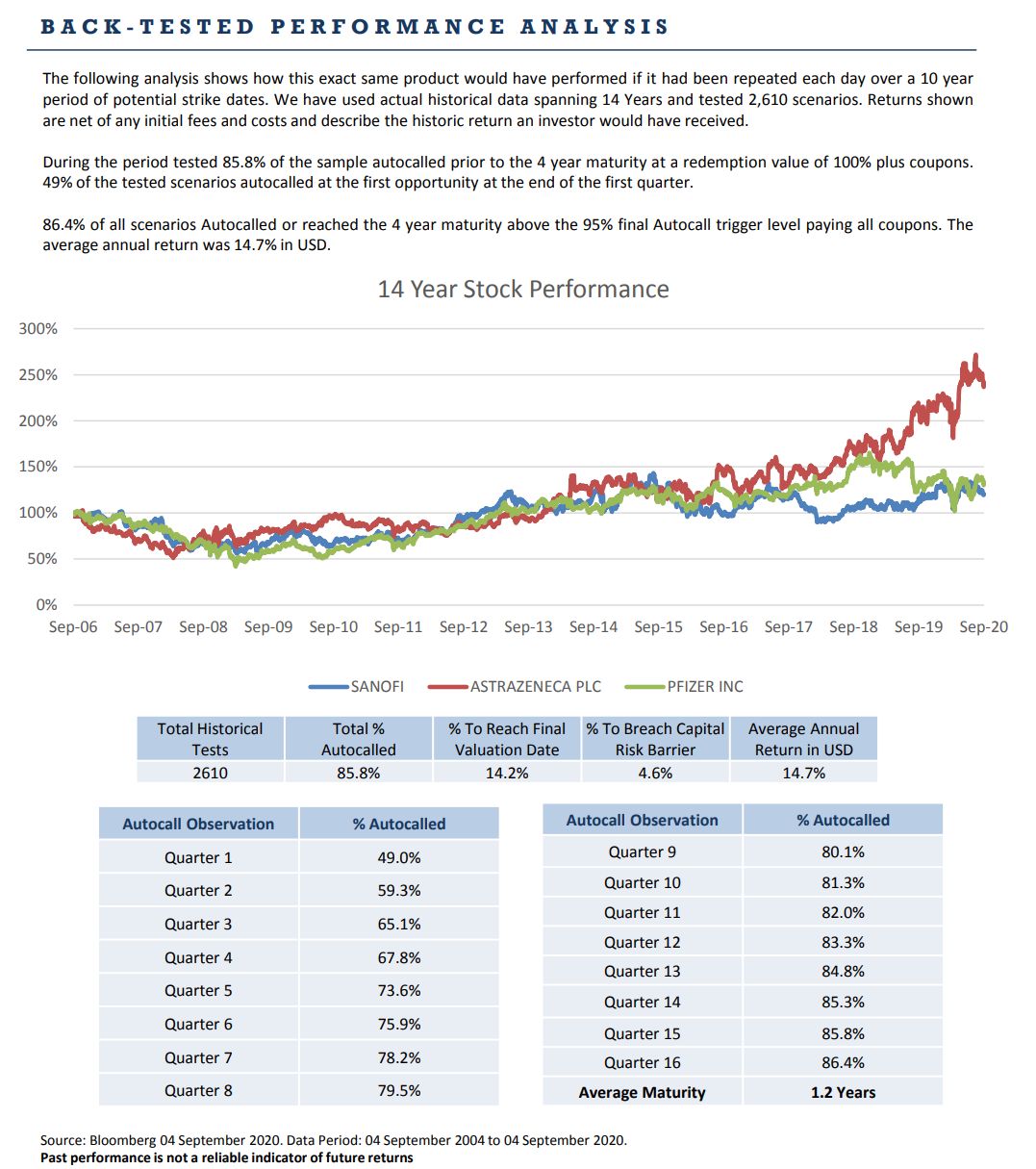

Note 2: Quarterly 4.25% Coupons, Basket of 3 Pharma Stock

I won’t redo the entire analysis, since the two Notes are structurally similar. Let’s just look at the differences.

This Note promises an even higher coupon! It’s 17% per year! Actually it’s 18.11% per year if you take into account compound interest. I mean, if the Trigger Value is met each quarter, thanks to Autocall you can reinvest the original amount plus the coupon on each subsequent quarter, which leads to 1.0425^4 = 1.1811478… ~= 18.11%.

Plus, the Trigger Value is 95%, which means you’d get 100% of your invested capital and all the amazing coupons even if all the assets in the basket lost 5% of their Strike Price! Awesome, right?

And the basket is composed of just 3 assets, not 4! This is an amazing Note!!

Or… is it?

Sadly, the good news end here. Let’s take a deeper look:

- The basket is composed on 3 assets, but they’re Individual stocks. Individual stocks are more volatile than Indexes. Individual stock returns are skewed by few winners. Several studies have been made on the subject, including a famous one by JP Morgan in 2014 where over 13k stocks have been analyzed. The study shows that 40% of stocks suffer a decline of 70% or more and never recover… The Trigger Value of 95% is just an irrelevant illusion of safety. Take a look at this amazing video by Ben Felix.

- The individual stocks in the basket are over-inflated pharmaceutical stocks at their all-time high valuation. I don’t know if you noticed but there’s a pandemic going on, and pharma stocks have been very hot recently. Maybe it’s already too late.

- The stocks seem correlated (which would be good), but given the winner-takes-all nature of a Gold rush (Covid Vaccine), I’d bet their future returns will be anti-correlated. We’ll see it in the mini-backtesting section of this Note in Q4 2020.

- The Note duration is just 4 years. A longer duration would have helped in high volatility environment.

- Frequent Observation Dates might trigger more Autocalls, potentially incurring in more fees. Maybe they can’t totally kill your quarterly returns with currency conversions and middlemen fees, they need to play smarter. Maybe only taking a 1% fee (but 4 times a year) on each Autocall…

I regret so much not having moved further with The Advisor, and missed the opportunity to see the actual fee structure! I’m sorry that I have to speculate on fees and not be factual 🙁

If anyone of you has extra details, please let me know!

“Ok, RIP, this Note is Riskier, but also the profits are higher! It’s called risk/reward frontier”

Yes, I know… But how can I quantify it? How can I price this product? How can I tell if the coupons are good or bad, given the other conditions?

“I don’t understand…”

Complexity

What I’m saying is that it is very hard to price this product.

By “pricing” I mean finding the values of the relevant variables that would make me buy the product.

I mean, if the quarterly coupons for the second Note would have totaled 100% instead of 17% I’d have bought the Note. What about 50%? What about 20%? I would have probably invested at 50%, but not at 20%… that means there’s a break-even value somewhere. How to find it?

What if the Protection Barrier was 20% instead of 70%? Then I’d buy the Note for sure! What if it was 50%? Mmm… I don’t know…

How to find the correct “price” for this product?

Let’s change the question, let’s invert: what’s the expected return for this product? Is it Pareto Optimal among all the available investing opportunities on the market? Can I find a set of assets that has a Pareto Superior risk/reward profile? Is the risk-adjusted expected return better than, for example, Earning Yields of the MSCI ACWI Index (currently 4.48%, since “World AC” CAPE is 22.3)?

I’m not even asking the “do I want to take this kind of risk?” question, which is purely subjective.

(Psst: take a look at this amazing Rational Reminder podcast episode with Ben Felix and William Bernstein, it’s mostly about risk, volatility, market expectations, age, and optimal portfolio based on these factors!)

I didn’t ask the above questions because I want to deep dive into the complex math behind expected returns for such products. It’s beyond the scope of this post, and probably beyond my current skills. And obviously it’s not solvable in closed form: you need a Monte Carlo simulation, along with models for expected future returns of underlying assets. No, it’s not beyond my skills!

I asked the questions to point out that you and me, average investors, don’t have the skills to judge if it’s a honest offer or not (before fees).

I intuitively think that it’s an inferior product in terms of risk adjusted expected returns, let alone my risk aversion that would discount risk even more, but I have no math to back my claim.

I’m much more confident in claiming that an actively managed US stocks fund with 10 years of underperformance history and a 2% TER is an inferior solution to Vanguard VOO, because the two are easier to compare.

My friend Julianek (who works in close contact with entities that issue such Notes) told me that they’re usually not unfairly priced, but the layers of fees on top will kill your returns. He said that the Autocall feature is there because they want to milk more subscription fees from you. My gut feeling is that they’re also mathematically inefficient, but this is pure speculation.

My First-Principles-Thinking reasons to claim the mathematical inefficiency are:

- Given the unicity of each structured products, it’s impossible for an individual to run an optimality analysis. And it’s easy for the issuer to run their simulations, discover that a coupon of 21% is the break even, and then offer a coupon of 17%. Who will ever complain? Who will ever find it out?

- Given the high “golden path” returns, retail investors won’t complain that they’re not higher. Nobody complains that the lottery prize is “only” 10M instead of 30M, even though the redistribution of lottery ticket sales among lottery winners is ~33% (in Italy at least).

- I assume the issuers (Banks) hedge and don’t play dice with these products.

I would like to spend few more words on the last point.

The Bank doesn’t play dice with the Structured Note

(Note: this is purely speculative. Please, change my mind if you have valid arguments 🙂 )

Structured notes are debt obligations. The issuer takes my money and uses it whatever they likes. Like if I subscribed a bond with them.

Let’s assume the issuer is taking my money, hiding it under a mattress, and crossing their fingers in the hope that the Trigger Value is never reached until Note’s Expiration Date.

Is this a good strategy? Are they just betting? Playing a Russian Roulette with me? I don’t think so.

Why would they take the same (high) risk that the Note carries with it?

My model for Note’s issuers (banks) is that they’re rather conservative. Banks are conservative. Now, I don’t know much about this CIBC bank… but it’s one of the Big Five banks of Canada, I assume they must play safe.

So, what are they doing with my money to hedge the risk?

At the very minimum they’re investing it in a low risk / low reward instrument, aiming to a low yield (say 2-3%) and still crossing their fingers. If the Notes are efficiently priced, on average they should win.

But this is still risky: in case the Trigger Value is reached they need to give me back a 10-17% return. As far as I know they don’t run charities – or when they do I’m not one of the beneficiaries but an involuntary contributor!

So they probably want to use my money to build a portfolio with a return profile that mimics the one they’re offering to me. Bonus points if it’s Pareto Superior, i.e. if for every possible outcome their strategy holds non-inferior returns compared to the Note’s obligation.

In this case they simply arbitrage between me and a set of more efficient products, making a profit with zero risk. Maybe using a combination of bonds, stocks, and derivative products (stock options, futures…) they can build a Pareto Superior return profile.

if this is true, and in my opinion this is very likely, that means the Note is mispriced for me, the unaware retail investor, even before fees and hidden costs.

Another hypothesis is that they’re simply gambling the system on a larger scale, like a Ponzi Scheme. They’re gambling like crazy, and if the castle of cards crashed they go belly up – or they ask for government support (like Italian banks). Head they win, tail government bails them out. Or worse, creditors bail them in.

Are they playing this game? Should I take into account credit & counterparty risks?

Hint: you always should when lending your money.

Anyway, I believe this second strategy is less likely to be the dominant one.

Other Random Problems with Structured Notes

Credit/Solvency risk: the issuer may default.

Underlying assets defaulting: if the product has some specific link to underlying assets, and one of the assets goes bankrupt, the issuer might not repay the principal. See structuredretailproduct.com for more details.

Illiquidity/Untradeability: Notes rarely trade on secondary markets, which means if you want to sell your investments before maturity you’ll have a hard time.

Call risk: according to the SEC and to Investopedia “for some structured notes, it’s possible for the issuer to redeem the note before maturity, regardless of the price. This means it’s possible that an investor will be forced to receive a price that’s well below face value“.

Conclusions

Structured Notes with the analyzed profile (there are infinite kinds of structured products) are risky and tax inefficient investment tools that carry limited positive but unlimited negative consequences.

The actual purchase of these instruments via a brokerage-like consultancy firm will bring extra more-or-less-hidden fees into the equation, that will make the investment even worse.

Structured Products are complex investment tools that make pricing and understanding risk not feasible for a retail investor, as also stated in the Factsheet:

I therefore recommend you not to invest in these tools, unless you’re really aware of what you’re doing, the risk you’re taking, and the fees you’re paying.

But if you have the required skills to judge the quality of a Note, you can probably build an alternative, derivative-based portfolio with a Pareto Superior return profile, and show the middle finger to the middlemen.

Bonus: What if I invested in those Notes?

What if I decided to buy the two Notes by end of September 2020? How would I be performing today, December 21st 2020?

Let’s see what I would have gained so far!

Note 1

All the four indexes are above 10% their strike price in their currency (which gained at least 5% compared to USD). This means probably the worst performing index in USD is the Nasdaq100, which is “only” up 11.3% compared to its Strike Price of September 30th 2020

Ok, we’re far from Autocall Trigger (end of September 2021), but if nothing else would happen for another 9 months we’d get the 11% (in USD) coupon (minus fees and taxes).

Which is less than what the market returned during last 3 months! VT is up 14.43% since September 30th. A 14.43% capital gain (not taxed in Switzerland).

So… inefficient!

“But RIP, you’re investing in USD Bonds…”

Sssh, shut up! Next!

Note 2

We’re close to the first Quarterly Observation Date (end of December 2020), can we cash the 4.25% USD coupon (while the USD lost 3.75% vs the CHF in the meantime)?

How are the three pharmaceutical stocks performing today?

Pfizer is kicking asses 🙂

What about AstraZeneca?

Ouch, it’s a -11.5% in GBP (-7.4% in USD). It’s below Trigger Value 🙁

What about Sanofi?

Oh, no! It’s at -7.2% in EUR… but in USD it’s just -3.2%! Above Trigger Value! Yay!

Sadly what matters is the worst performing asset, so maybe we’re going to skip the December 30th observation date, and “memorize” the coupon for next quarter.

In the meantime we should cross our fingers that AstraZeneca recovers, while Sanofi doesn’t lose an extra 2% and the USD keeps going down…

Who would have thought it! In their 16 years of backtesting the Note performed amazingly! 😀

{kind=link}

Who would have guessed that these stocks were anti-correlated during a vaccine gold rush?

Hint: everyone.

Bonus Conclusion

Both Notes were inefficient, and I had superior available alternatives – that I didn’t take anyway, but that’s another story.

It’s a high volatility market, and this Structured Note’s profile is suited for “calm, sideways markets”.

It’s a highly inflated market, a double digits drop for any asset is behind the corner, especially for individual stocks, especially for stocks with high expectations like pharmaceutical companies during a pandemic.

Think twice trice ten times before buying these products.

External Resources

Investopedia article “Why Structured Notes Might Not Be Right for You”

Structured notes are complicated and are not always designed to be in the best interests of the average individual investor. The risk/reward ratio is simply poor. The illustrations and examples provided by investment banks always highlight and exaggerate the best features, while downplaying the limitations and disadvantages. The truth is that on a historical basis, the downside protection of these notes is limited, and at the same time, the upside potential is capped. Now add the fact that there are no dividends to help ease the pain of a decline.

If you choose structured notes anyway, be sure to investigate fees and costs, estimated value, maturity, whether or not there is a call feature, the payoff structure, tax implications, and the creditworthiness of the issuer.

SmartAssets article “What Are Structured Notes and How Do They Work?“

A structured note can open up myriad opportunities for investors. A disreputable institution or a wary bond issuer can slam all of them shut. Be aware of the considerable risks before considering this particular investment.

If you feel your portfolio can withstand the risk for the potential rewards that structured notes can provide, they may be worth considering. However, if you’re approaching structured notes with any trepidation, consider seeking some impartial advice.

Investments for Expats article “Structured Notes: What You Need To Know As An Expat”

Money Sense (Singaporean Government Agency) article “Understanding Structured Notes”

A detailed article by the SEC (US Securities and Exchange Commission) about “Structured Notes with Principal Protection”

The retail market for structured notes with principal protection has been growing in recent years. While these products often have reassuring names that include some variant of “principal protection,” “capital guarantee,” “absolute return,” “minimum return” or similar terms, they are not risk-free. Any promise to repay some or all of the money you invest will depend on the creditworthiness of the issuer of the note—meaning you could lose all of your money if the issuer of your note goes bankrupt.

Also, some of these products have conditions to the protection or offer only partial protection, so you could lose principal even if the issuer does not go bankrupt. And you typically will receive principal protection from the issuer only if you hold your note until maturity. If you need to cash out your note before maturity, you should be aware that this might not be possible if no secondary market to sell your note exists and the issuer refuses to redeem it. Even where a secondary market exists, the note may be quite illiquid and you could receive substantially less than your purchase price.

That’s all for today 🙂

Good summary of structured products. I thought i would add more details about “the bank not playing with dices”, i.e what exactly is the role of each financial entity in a structured product transaction.

There are usually four actors involved in such a transaction:

– the buyer (i.e you, had you bought the note)

– the distributor, who is usually incentivized with a “distribution fee” (2% of the notional is not unusual) to distribute the product to the buyer. In this scenario that would be MCDD. But in some cases it is more blurry. For instance in the case of wealthy people, the distributor can be directly their private banker who is solicited directly by the issuer (unbeknownst to the wealthy individual -> there is then a huge disalignment of incentives).

– The issuer of the note. The issuer will take the money sent by the client (called the funding) and invest it in low risk securities like treasuries. In a sense this is a business model very similar to insurances: you receive premiums/funding, invest the money and pay back later claims/redemption of the product. Because treasuries don’t pay that well, often the issuer will charge an additional “sales credit” fees that is a few dozens basis points to the buyer.

We need a hedger as well. The issuer will make at most less than a percent on the funding (treasuries pay peanuts currently), so someone has to hedge the risk when the note performs well for the client. In the case of the notes discussed in this article, the issuer won’t be happy if he has to pay you 17% per year and only make 1% on the funding. So there is a fourth actor involved to hedge the risk of the product. It is not unusual that the issuer and the hedger are the same entity, but they can differ (in which case the hedger takes a commission of a few basis points). As you correctly mentioned, these products are usually a combination of bonds and options. Thus they can be hedged so that if the note performs well for the buyer (and thus badly for the hedger), the hedging trades will counterbalance this and the hedger portfolio will be breakeven. Now for the sophistication of the hedger: it is usually a sell-side entity (indeed they need a big balance sheet to be able to do the hedging trades), so keep in mind that the hedger is usually hedging thousands of such notes at the same time. Thus his business model is to not take a view on where the notes are heading but just to hedge them so that the portfolio is breakeven and he makes money on the hedging fees.

About the pricing of those products: as you correctly mentioned, these notes are extremely hard to price, and most actors will price them with a monte carlo engine. The parameters of the engine are usually the volatility and correlation of the underlyings. The flaw is that these parameters are only about past time series/volatilities/correlations, which works most of the time, but when they don’t, the losses are staggering for the hedger.

thanks Nero Tulip for your very deep comment which more or less confirms what I intuitively deducted.

I see that the hedger is not purely arbitraging but taking some risk, and I understand that they don’t hedge individual Notes but aggregate positions. Probably the total volatility of a basket of N notes is lower than the sum of individual ones, which means the issuer doesn’t have to spend all the funding in hedging.

… and maybe when “the losses are staggering for the hedger” then “mama gov” comes rescuing? 🙂

For “Mama gov”, we will have to see, this kind of business has different cultures around the globe. For instance, structured notes are popular in Switzerland but not in many other parts of the world. American firms famously preferred credit derivatives (like CDO, CDS…) to equity derivatives and we know how it ended. Asian markets prefer to do everything OTC (so there is no note per se). In France, Societe Generale is famous for its derivatives but the population hates everything related to finance so i doubt that the business is big enough so that retail investors are involved. As far as I know Switzerland is unique in the way those products are proposed to the public.

In CH, as far as I know only UBS, CS and Raiffeisen are deemed too big to fail by the government, and so they may indeed be bailed out in case of misdeeds. But smaller players like Vontobel or Leonteq will surely go under if it happens to them.

Now regarding hedging in particular, you don’t need a big portion of the funding to hedge the product. For instance, the notes you are talking about in this article are made of two components:

– a bond issued by the issuer -> in case the issuer is the hedger, there is nothing to hedge here. If the issuer defaults he has more important things to do than hedging his own bonds. This bonds represent usually more than 90% of the value of the note.

– an option. More particularly, the buyer of the note is short a put option on the worst performer of the basket of underlyings. The “high coupon” that the buyer receives is nothing more than the premium received for the sale of the option, spread over multiple periods. The option may have exotic features like autocall and memory, but the principle is the same: the buyer is short a put option.

This means that the hedger is short a bond (that he does not have to hedge if he is the issuer), and is long a put option. Hedging a put option is well documented (for instance Nassim Taleb wrote a book on the subject called Dynamic Hedging), and the hedger needs to buy/sell the right quantity of the underlying so that the sensitivity of the option to the underlying (delta, gamma and other funny greek letters) is cancelled by the position on the underlying. Here is an example for call options: https://www.investopedia.com/ask/answers/040315/how-can-you-use-delta-determine-how-hedge-options.asp

Now back to what i said earlier: these notes seem to be more and more distributed to retail investors and i doubt many of them have any clue of what should be the right premium to receive to be compensated for the risk embedded in their short put option (on a worst performer!). Not sure that 17% is even big enough in this case…

I assume it is a coincidence that someone called Nero Tulip mentions Taleb…right 😉

The ‘coupon’ of the note is the premium of the options less the charge the issuer decide to keep for itself: part finance, part marketing.

I think they choose names that their sale dep think can sell well, here I bet the pharma stocks because Swiss but also because every doctor/lawyer (the usual buyers of these things) read those names in every newspaper.

Hi ILS, welcome to my blog 🙂

I’m interested in understanding more, and I would love if you can expand your comment a bit more. What do you mean by “The ‘coupon’ of the note is the premium of the options less the charge the issuer decide to keep for itself”?

which options? Are we talking about a plain PUT option (at protection barrier strike price)? How would you formulate such an option? And which products emulate a link between my returns and the worst performing assets in my basket?

Can you please list in this concrete case a set of options that would replicate one of my notes?

My intuition is that this return profile is not replicable with standard derivatives, but I’d love to be proven wrong

Thanks!

my professional experience with basket options, how these securities are called, is limited to currencies. Maybe some premises are due: to price an option you use some variant of the Black-Scholes formula (which was originally invented by Ed Thorpe…nice story told in his book “a man for all markets”), which assumes that securities prices can be modelled with a normal distribution, later refined to take into account that the tails of that distribution are too ‘slim’. You can then build a correlation matrix between all securities based on historical data and adjusted the way you want (in this case for example for the covid vaccine).

With these two elements, you can basically price any type of scenario combination. The Covid-vaccine adjustment, as any other adjustment, is priced by the ‘market’ as an average of all the market participant opinions: you can think that the adjustment is too expensive or too cheap and therefore trade against it, but that’s the best estimate there can be.

Another element is that you can hedge any option going long/short the underlying security: this is called delta hedging and there are formulas that tell you you much underlying you need to hedge that option in that specific moment in time.

So the seller of the Note can hedge itself in many ways, all of them leaves it at zero risk:

– if it holds the securities in other part of the bank for other reasons, it has a ‘natural’ hedge via delta hedging

– it can buy/sell the component of the Note, the options, to other banks

– it can trade the basket option with another (usually bigger) bank, that ultimately is able to create a natural hedge on its balance sheet.

If the Note was linked to a single stock, the issuer sell a out of the money CALL on that stock, gets a premium plus the dividend on that stock and can use 100% of those proceeds as the coupon (interest) of the Note. if you use multiple stocks and the level is based on the worse of them, you can show an higher coupon because the probability to get there is lower.

You are right that these Notes works best in a ‘neutral’ market, which makes them not really interesting because the market is rarely neutral.

The Animal Spirit podcast has now like 4 episodes on Structured Notes, if you need more infos (I also wrote a post about InnovatorETFs on my blog ;))

As your friend said, the coupon you get on the Notes is usually in line with the market price, the seller gets its money via the FAT fees it charges.

(I have several friends living in Zurich that in normal times I visit regularly, maybe one day we will discuss this in front of a beer eheheheheheeh)

Thanks for your detailed contribution ILS.

Didn’t know about basket options, and Delta hedging.

Thanks, I think I now got it 🙂

Le “Note Strutturate”, o Certificati, sono strumenti derivati estremamente complessi SEMPRE svantaggiosi per l’acquirente. Il sottostante è un’OPZIONE, un derivato finanziario che rappresenta l’ombra della nota stessa. Nel contratto di OPZIONE io ho il diritto, ma non l’obbligo, tramite pagamento di un prezzo (premio), di esercitare o meno la facoltà di acquistare (Call) o vendere (Put) una data quantità di una determinata attività finanziaria, detta sottostante (es. le azioni che tu hai come ‘strike’ nella tua ‘nota strutturata’), a una determinata data di scadenza o entro tale data e a un determinato prezzo di esercizio (strike price).

Se MCDD avesse in mano l’opzione di comprare 1milione di azioni Tesla, OGGI, al prezzo di un anno fa (Tesla ha fatto +650%) oggi la eserciterebbe, con un guadagno di 6,5milioni. Del resto se Tesla fosse crollata non dovrebbe sborsare 1 milione, avrebbe ‘buttato’ solo i soldi dell’acquisto dell’Opzione.

Però le banche non amano buttare soldi, neppure potenzialmente. Allora cercano un ‘pollo’ a cui rifilare una nota strutturata: se tutto va bene (Tesla sale) gli dò solo un x di percentuale di interesse, a lui le briciole a me la pagnotta. Se invece Tesla crolla tanto che io perderei il prezzo della nota (strike price) allora è lui che paga, non io (non gli ridò il capitale investito, che lui ha prestato a me – la Nota è un titolo di debito – e con cui io ho comprato un pacchetto di OPZIONI).

Con dei semplici calcoli attuariali (semplici per chi ha la nota tecnica dell’opzione che sta dall’altra parte dello strumento, lato consumatore è MOLTO complesso perché devi stimare al buio) io calcolo come impostare una ‘Nota Strutturata’ con cui guadagno sempre.

L’OPZIONE è bella perché puoi guadagnare infinito e perdere al massimo X.

La Nota Strutturata / Certificato è una ‘fregatura’ (mi si passi il termine, è IMHO) perché puoi guadagnare massimo Y < al potenziale rendimento di X e puoi perdere tutto.

Il meccanismo è commercialmente molto valido perché la Nota Strutturata (che è svantaggiosa) viene proposta quasi come un investimento ‘sicuro’ (prendi 12% a trimestre, potenziale, e hai il capitale garantito, salvo una “remota” possibilità che lo strike price fosse inferiore… a orecchio è ragionevolissimo), l’OPZIONE invece appare come estremamente pericolosa (puoi guadagnare infinito, ma di fatto se Tesla è scesa tra un anno ti conviene buttarla l’OPZIONE e perdi tutto).

Ovviamente viene la nota strutturata (o certificate) OLTRETUTTO costruita in modo che ci sia un valore K COMMISSIONE che va a remunerare chi vende questa roba. Quindi la signorina che ti ha chiamato (chiamarla Financial Advisor è un pò triste per la catagoria…) prende un 3/4% (di solito) di parcella su quante ne vende.

Ovvio che il suo obiettivo è venderle e poi rivenderle: queste note escono ogni mese, e lei ha un budget di roba ogni mese da collocare: ti ha fatto vedere quelle vecchie, ma punta a chiamarti per prenotare le prossime sottoscrizioni. Poi magari azzecchi la nota strutturata su Tesla, tu prendi il 3% l’anno e sei contento (uhhh… rende più di un BTP! Quanto è BUONO questo titolo! Tanto su Tesla e quando mai perdo?!) e lei ogni mese ti rivende qualcosina.

Tutto ciò è molto brutto… non si chiama qualcuno perché probabilmente ha dei risparmi per vendere a freddo gli strumenti più complessi (ed alcuni tra i più rischiosi) del mercato. In Europa (non so Svizzera) che la normativa Mifid2 che vieta di fare queste cose (non che non le vendano anche ai 90enni con la terza elementare).

Poi c’è gente a cui i certificati/note strutturate a qualcuno piacciono (a me no, li considero troppo complessi e poco efficienti per i semplici risparmiatori) e allora qui ne trovi una bella carrellata: https://certificati.leonteq.com/

Inutile che ti dico che prima del termine le note strutturate sono anche molto illiquide e difficili da negoziare (di solito) e che c’è rischio controparte (se l’emittente fallisce il liquidatore fallimentare può mettere nelle masse di proprietà della società i soldi con cui le hai sottoscritte… oltre a bail in etc…).

Hanno alcuni vantaggi fiscali come l’assorbire (in Italia, almeno) la minusvalenza fiscale accumulata pregressa anche con le ‘cedole’.

Amazing contribution Bowman, it would be very useful to my English speaking community. I’m replying in English, I hope you’ll do the same.

In your Tesla example you’re considering only the “up 600%” and “down 90%” alternatives. This Note sucks in both scenarios, of course… but if Tesla stays flat you win with such a note.

I don’t think it’s necessary a bad deal, it’s just hard to price it correctly. Which means they (the issuers) have all the incentives in the world to find a reasonable balance between risk and reward, but offer a shittier version to you 🙂

Brilliant, but tough post today! I will read it twice! 🙂

You’re welcome!

… wait for the second read…

You’re welcome 😀

Usually this kind of transactions take place between a sucker and a crook. If you are certain you are not the crook you might very well be the sucker. If it looks like crap, smells like crap and tastes like crap there is no need to further stir it up.

False dichotomy, fallacy of Gray.

With this line of reasoning no transaction makes sense.

As we live parallel lives, funnily enough, someone sent me a link to a structured note and it was the first I’d ever seen: https://www.fairinvestment.co.uk/product/mb-uk-supertracker-plan/

LOL, how did it go? Did you show them the middle finger? How crappy was it?

I would be curious to see what would have been the next step…

As you rightly noticed structured products are mostly not suited for retail investors.

The financial advisor should have first assessed which type of investor you are and your financial knowledge and experience, before proposing these products (ok, they didn’t actually propose the products to you, they were just examples).

In Europe (and Switzerland is mimicking a light version of it) there is quite a big regulation with stringent rules aimed at protecting investors from these cases.

Yeah I know… I should have gone a step further but I didn’t.

She didn’t assess my financial knowledge, experience, and more importantly my risk aversion.

I told her “I’m fearful, I don’t like to take much risk”. She translated it “ok, a 70% Protection Barrier on the worse performing among these 3 individual overpriced and overhyped stocks should be good for you” 😀

Hi Mr RIP,

I read a lot of your blog in the past few months and learnt a lot. Thank you very much for this massive amount of work and time you dedicate to share your experiences and ideas. I am considering myself as “financially educated” but I know that sharing allow all of us to exchange ideas and opinions, and I am writing my first comment on your blog. Indeed I would not be so hard with these structured products.

I am using these kind of notes, more specifically called “Barrier Reverse Convertible” in Switzerland (category #1230 from the Swiss Structured Products Association). There is a secondary market with around 10 different products on the SMI index only, and more than 1’000 different products on a basket containing SMI index and other constituents, with different settlement currencies and maturities. There are also thousands of those products on different stocks, that’s for sure.

The reason why I am including such products on equity index such as SMI is to “replace” bonds as the conservative part of a portfolio. Holding bonds in a CHF portfolio seems useless to me and I therefore switched . However, I am not trying to get awesome returns: the last one I bought should lead to a 5-6% return p.a. over 2.5 years, and the underlyings are SMI, S&P500 and EuroStoxx50. There are also a few important points that I want to highlight, with this product as a concrete example.

Facts about the product :

Coupon is 3% p.a. paid quarterly in CHF, and I bought this product at 92.57% on the secondary market. Therefore I get 3% p.a. in coupon + 7.43% over the life of the product (because the product is redeemed at 100% at maturity). Moreover, for these products in Switzerland, the coupon is not considered as an interest but as an option premium, which is basially like capital gain and hence not taxed.

Barrier is at 59% in local currency and the CHF coupon is paid in any case, no matter the underlyings’ performance. Therefore, the FX-risk on USD/EUR is not adding up on the market risk of the 3 underlyings (though I am sure that the issuer has still factored it in its pricing).

Distribution fees are disclosed as “up to 0.29% p.a.” but I don’t know if there are other hidden costs.

Key points for me to consider this product as a “conservative investment” :

A drop of 41% of any of the underlyings has occured only twice in the last 21 years (dot-com bubble 2001 and financial crisis 2008) and in that case, I would expect high correlation as it is mostly the case during significant dropdowns in global equity markets.

In case the barrier is touched and if there has been no recovery by maturity (2.5 years), the worst performing underlying is PHYSICALLY delivered. This means that instead of realizing the worst performance and receiving cash, I would receive an iShares ETF on the worst performing underlying. I would be free to sell it immediately and realizing the loss, or keep it in my portfolio and wait for recovery. It’s true that in the latter case, the “conservative investment” would turn out to be pure equity risk.

In any case, if the underlyings grow, I will not benefit of the upside, that’s certain. Due to the “Early Redemption” feature, the issuer may also redeem the product before maturity. That will probably be the case by end-of May 2021 if the market continue to rise. With Early Redemption, I would realize the 7.43% anyway + the coupon of 3% p.a., which is not that bad for an investment that I consider “safe” with the low 59% barrier. If it happens soon, I will comment again and disclose the realized performance.

Thank you for your time again, and keep on the same way 🙂

It seems a good deal. Actually, “too good to be true”. But it’s still hard to correctly price the asset.

If it seems too good to be true either the issuer is a charity and you’re their target, or it really is too good to be true.

Do you have a link?

It is a good deal, I think. Particularly in the context of near 0 interest rates. You are selling a put option to the bank in that case, that’s why you have decent return.

As an example, you can simply search “CH0521982972” on Swissquote website and access the termsheet (no account needed). I add the direct link below.

With Ask price at 97.16% and coupon at 3% it lead to 4.58% equivalent annual return. If there is an early redemption, then the return is slightly higher (always buy products quoted below 100%). It is the same product that I got earlier this year at 92.57%. 😉

Let me know what you think !

https://www.swissquote.ch/sqi_premium/FileServlet?file=termsheet%2F9%2F7%2F2%2FCH0521982972.pdf

Ciao Giorgio.

I just finished a phone call with a guy offering his service as financial advisor. He worked for ee*e.

After a short discussion in which I mentioned that I have a good 3 pillar, he proposed me a good deal: STRUCTURED NOTE.

Fortunately, I read your blog before 😛

thanks!