Table of Contents

- The Wants

- The Financial Plan

- (back of the envelope) Analysis

- Alternatives considered

- F.A.Q.

- Are you still interested in FI? And in RE?

- You didn’t mention investments at all. How is your investment strategy going to change?

- You didn’t mention cutting expenses… Should BabyRIP go to Kinderkrippe if you’re both unemployed? Should you cut cleaning lady costs? Should you move back into a smaller flat? Anything else?

- What about going back to Hooli?

- What about unemployment insurance? Will you go to RAV?

- Should you rent an office/coworking space if you want to work on your projects?

- Last but not Least… for how long are you allowed to stay in Switzerland without a job?

- Let’s face the elephant in the room: How do you plan to generate money?

Hi readers,

This is the second post on my quitting series. Last time I told you that on Feb 6th 2020 I quit Hooli. Well, I gave my notice period, I’m still a Hooli employee until March 31st. I also shared with you my internal dialogue associated with this tough decision. I have a lot more to write about it, about all the reasons why I quit, why I got progressively more detached over time, why I think I’m done with my career, what I didn’t like about my employer and my industry, but also why I think Hooli is still a great company… but not today!

Today I’m going to talk about the financial plans for the near future. It will be an interesting journey, I hope you’l enjoy it 🙂

And of course, please, help me validate my plans, give me feedback and kick my ass if necessary!

So, I quit my job and I’m not looking for another one. I’m not FI in Switzerland and I’m staying here. How to call this?

LeanFIRE? Nope. At an optimistic 3.5% SWR our wealth could cover half of our current baseline expenses.

SemiFI? Well, maybe. But according to r/SemiFI “about” section: “semiFI is a strategy in which one downscales in employment after acquiring a large portion of one’s savings goal. Downscaling could mean intermittent work or a lower paying job. It’s about achieving partial freedom now, rather than total freedom later“. Kind of fits my current situation. Except that I’m not downscaling. At least I don’t have the intention of taking part-time, intermittent, or a lower paying job in my field right now. I’m running away! I don’t want an office job, and I don’t want to freelance (for now) as well. So… Nope.

Just taking a Mini Retirement? Yeah, maybe, kind of. How mini is this retirement? I don’t know. How retirement is this mini? I know not.

What else? Partially funded lifestyle change? Unemployed barista FI? Work not Optional?

Nein.

“So RIP, you’re telling us that you quit your current job, you’re not looking for a new job, and you’re staying in Switzerland spending at least 7k CHF per month? And you recently moved into a more expensive flat while also sending your daughter to an expensive Kinderkrippe? Well, that’s… interesting…”

So much interesting that in absence of a better term I want to call it StupidiFI. I.e. being technically FI according to my old metrics, but intentionally not FI because I want to live in a VHCOL country with my family. I’m promoting stupidity!

“HaHaHa RIP! 30 years of Net Worth tracking, 18 years of “dream jobs”, 7.5 years of accelerated accumulation at Hooli, and almost 4 years blogging about FI… and you’re screwing everything up now? Haha where is the unsubscribe button? 😀 ”

Yeah, it’s fun. But – as always – wait before judging 🙂

I have a plan!

But before that, let’s see which kind of problem are we trying to solve.

Is this a FI problem? I mean, should we optimize our family decisions to achieve FI by some definition? Or is it something else?

The way I now see Financial Independence it is a bit different from few years ago.

I started my FI journey thinking “let’s work work work accumulate a lot and then call it done, quit, and relax”.

I’m no more that person. Going that way already costed me some health and happiness. I’m closer, but I’m not there yet. Something needs to change.

I want to optimize for health (physical and mental), then for happiness (family, individual, circle of people that I care about, and rest-of-the-world in this order), then – eventually – for freedom, wealth and financial security. Which are inferior goals compared to the first two, but still nice ones to achieve.

This means I’m ok with slowing our wealth accumulation down and taking some risks, if this means having a better chance at the life satisfaction game.

So, what are the criteria to improve my health and my family overall happiness? I and my wife sat down together several times in the last couple of months, and defined what’s important for us. Sorry BabyRIP, your vote doesn’t count yet. Well… you got good attorneys, do not worry.

The Wants

The list of criteria is pretty long, and most of them are in open conflict one another, but we ended up finding agreement on the following:

- I’m not able to be an employee anymore for the foreseeable future. This might change in few months/years, but I need to take a significant break now.

- We love or current neighborhood, city, and country. We want to try to stay in Switzerland because we objectively like almost everything of our daily life here. A lot of friends, an amazing almost car-free neighborhood, a lot of green areas, essentially the best place for a child to be born, a multicultural environment, a mentally challenging community, physical safety and much more. The only problem is that it’s very expensive.

- Moving back to Italy is still an option, but it doesn’t excite us. We are willing to sacrifice a bit of financial security to try to stay here in Switzerland. It means we’re ok with reducing by 5% the chances of FIRE success in future in Italy if that means raising by 50% the chances of staying in Switzerland for 5 years or more. Probabilities are subjective, but I hope you get the idea.

- If we had to go back to Italy we have a huge list of criteria (good quality of life, not a major city, close to the sea, close to public transportation, fast internet, bicycle friendly, not far from both our families, vibrant community and so on) that made us think at the Romagna area, eastern side of Emilia-Romagna region.

- Current candidate Italian town for now is Ravenna (or Ferrara, Faenza, or any one on the “colli romagnoli” like Modigliana). Do not ask me more about this, we chose that place almost randomly. If the Ravenna project will kick off, we’ll explore the area in depth and pick a final destination – which could be completely different from the current candidate.

- It may even be that in case we more back to Italy I’d make a “call to action” to kick off a early retiree eco-tecno-village somewhere in the south of Italy. Instead of trying to find he best existing place to go, let’s try to create a place where we want to go! Who’s in?

- We owe our daughter something, but not everything. I’ve written down (not validated with my wife though) what I owe my daughter, and what I owe her not. It’s my duty to keep her safe, well fed, educated. It’s my duty to expose her to opportunities and enable (to a certain extent) her to achieve her full potential. It’s my duty to make her feel loved. I also perceive as my duty to grow her in a lovely environment, which translates in trying to be happy myself and cultivate love and harmony within my family. It’s not my duty to grow her in the safest place in the world. It’s not my duty to send her to the most expensive university. It’s not my duty to optimize for her opportunities at the price of my health and happiness. She’ll be fine anyway. I grew in worst conditions, without me as a parent, without internet as an opportunity machine. I had the gift of the struggle. She’ll be fine everywhere. Of course growing in Switzerland is a plus, but it’s a “best effort”, not a “must have” feature.

- I want to be productive on my projects, which may or may not earn some money. I don’t want to retire to live the good life. I can think of nothing less pleasurable than a life devoted to pleasure. (John D. Rockefeller)

- My wife also wants to be productive and have some space to cultivate her passion projects, but we both agree that to maximize the likelihood of staying in Switzerland for as long as we want I’m the best bet for the family. Therefore she’s willing to take ownership of a larger amount of shared household responsibilities (taking care of BabyRIP and house chores). Sending Baby to Krippe 2 days per week is a good tradeoff for now. When she turns 3 (April 2021) more and cheaper options will become available, like Spielgruppe (playing groups) in our neighborhood. Then at age 4 she’ll go to Kindergarten every day, which is essentially free.

- We both value “alone time”, “family time”, and “social time”. Which means whatever productive activity we take, it must be flexible enough to not suffocate the above mentioned priorities. We want to give ourselves the gift of time.

- We’re both aware that we have been lucky so far with our parents’ health. It won’t last for long. our parents are in the 67-76 years old range, and their health won’t be so good forever. We want to be able to give them the support they need, when they’ll need it. Which kills any long term crazy plan like move-to-Thailand-because-is-cool.

The Financial Plan

The above list is pretty big, and it tries to answer too many questions: where do we go? What do we want to do? How to make it financially sustainable? There are many moving parts and unknowns. Since this is still a FI blog, let’s fix the financials first.

We have a good amount of money, which we all know it is not enough to be FI in Switzerland at our current spending level. Well, actually it’s not enough to be FI here at any spending level for a family of 3. But it’s enough to bootstrap next phase of our life, and a plan B.

How? Not too fast. It’s… Storytime! 😀

The rant

I wanted to quit Hooli in June 2019.

I remember counting down the days.

I actually wanted to quit in fall 2017! I was struggling to find meaning while working in Hooli Shopping Search Quality (ranking algorithm). I was doing good and getting good performance scores, but I couldn’t sustain it anymore.

“Why RIP? What didn’t you…”

No no no. Not today. Shut up and listen!

“😐”

After 6 months of pain, and feelings of meaninglessness I reached “bonus day” (Jan 25th 2018) and thought… “Ok, maybe I should just quit and then think what to do. No, that’s crazy. It’s Hooli, the best company in the world! Let’s try to change team again (I already changed team 1.5 years prior) because I’m sure it’s just a quality problem. I don’t like working in ranking, search quality. Hooli is full of almost infinite opportunities!”

Changed team (Hooli Video) in February 2018. By the end of March (two months later) I was already half dead. In retrospect I would have been much better off staying in my previous team and maybe grinding another year to get a promotion… but that’s just a stupid “what if” game that doesn’t make sense anymore. Financially, I knew I was going to enjoy 3 months of generous Paternity Leave in summer 2018, so I started planning for a potential quitting date of January 2019.

I started my first “freedom calendar”, a countdown sheet to count the days until January 31st 2019.

Year 2018 has been a slog and my productivity declined, but the long summer break (paternity leave) helped in making it a bit more sustainable.

Then December 2018 came. Out of nowhere, a couple of weeks of interesting and challenging algorithmic work showed up. Such a rarity! You know, the things we ask at coding interviews are never ever ever representative of daily life of a software engineer, but those two weeks have been awesome! I worked extra hours, I didn’t want to stop working on both Fridays! I was in the flow thanks to a self contained problem I had to solve and engineer. Awesome! Maybe this is going to last! I was re-evaluating my quitting decision… Add to that the October-December 2018 market downturn, and you got it right: I’m not quitting in January 2019 anymore!

Of course it didn’t last.

Corporate bullshit machine forced me to switch to another project while the amazing one was not even close to be finished, but “good enough”. Maintenance mode. Soon to be deprecated, rewritten, offered to someone who would have hated it. My frustration and feelings at the time were close to this amazing write-up by Eevee in his Vox 2015 interview:

Ok, I told you today I was not going to tell “why” I quit- and I’ll stop here, for now 🙂

So I entered my dark Q1 2019, where I started another countdown sheet with the goal of quitting by June 2019 (a vesting event):

The pain was unbearable though. I asked for a part time work reduction, and/or for a sabbatical but… denied both. So I got a paid 6 months “sabbatical” thanks to a comprehensive doctor who diagnosed me with burnout on the last week of March.

The actual plan

June 2019 arrived, still on sick leave, still a Hooli employee.

I was fine quitting in January 2019. At FIWE 2018 (June 2018) I had a talk about my midlife crisis. Everybody told me to “go fuck myself” and just quit the job that was making me unhappy. We also wrote a funny resignation letter together!

I was sincerely happy to quit in June 2019. The economy was doing great, and our Net Worth crossed 1M EUR.

Why am I telling you this?

Because my financial plan for the short and mid term future is connected with June 2019.

As you should know if you’re following me since at least last summer, I didn’t give myself permission to quit. I wanted to try yet another thing at Hooli Cloud, and I did try it. It didn’t turn out to be enough to bring my motivation back, but it came with some perks: a lot of extra money.

I want to give a specific meaning to the extra money earned in this very last attempt.

Quitting in March 2020 brought to the table 9 more salaries, a yearly bonus, 35k USD of stocks, 6 months of Reliability Engineer extra 20% compensation, and other perks like pension contributions, health insurance contributions and so on.

“RIP, what a pity… June 2020 was close… and Hooli stocks are skyorocketing! How much would you vest?”

Oh please, give me a break! What? Ehm… something like 40k USD of stocks in June 2020…

“…And then December 2020 / January 2021 would be near!”

Can you see the danger? I found the courage to break this golden chain, so please GFY!

Back on track: I wanted to quit in June, and maybe moving back to Italy. I was more than ok with that. How are we doing, financially, compared to June 2019? We’re in a much better shape, almost 200k EUR wealthier!

I want to use this amount as a buffer, as “recreational money”. I want to visualize the power of extra 9 months of work in terms of extra years of living in Switzerland! The growth of our wealth since June 2019 is now funding the “Stay in Switzerland” project.

Let me introduce you to this graph: In this graph (live link in my spreadsheet doc here) the yellow line is our Net Worth since January 2018, measured in EUR.

In this graph (live link in my spreadsheet doc here) the yellow line is our Net Worth since January 2018, measured in EUR.

The blue line is the so called “Ravenna Threat“, i.e. a threshold value for our NW that if reached from the above “something should happen” (more on this below). The Ravenna threat value is our Net Worth level by end of June 2019 (1,018,750 EUR), growing by 1% per year to emulate inflation adjustment.

The red scary line is the “Pioltello Monster“, which is our Net Worth in January 2019 (759,370 EUR) growing by 1% inflation. If our NW would reach the Pioltello Monster “something should happen NOW”. Why Pioltello? Because it’s a crappy town close to Milan, Italy, where “someone” owned a shitty flat. Do we want to awake the Pioltello Monster? No! Never!

The difference between current Net Worth and Ravenna threat is the Swiss Buffer, which is nicely crossing 200k EUR these days: the actual actual plan

the actual actual plan

So, finally, the financial plan is the following:

1) We stay in Switzerland, working on our passion projects, while our Net Worth is above the Ravenna Threat, i.e. while the Swiss Buffer is positive.

2) If our NW declined and fell below the Ravenna Threat for 3 consecutive months, either we should find a way to become cash flow positive (get a real job?) or we leave Switzerland.

3) If our NW declined and fell below the Pioltello Monster, we must react immediately: leave Switzerland or get a job.

4) To give us some breathing time, we allow ourselves a grace period of 1 year (until March 31st 2021) where we don’t care what happens to our Net Worth. That means if tomorrow market crashes 90% and we found ourselves below Pioltello Monster, we don’t give a crap anyway until March 31st 2021.

That’s it.

That’s our current financial plan, which is – for now – only setting conditions and consequences. It tells us nothing about how we plan to make or spend money.

It’s a plan that allows us to focus on short/mid term goals without the worry of money. I strongly need to care about my health, enjoy time with my family, cultivate my creativity and passions, check if my software career is definitely dead or not.

I know it doesn’t make sense to plan for the far future in this moment.

(back of the envelope) Analysis

Let’s play a bit with numbers.

Swiss Buffer is currently 200k EUR (212k CHF). February 2020 is telling me that we can keep expenses at around 6k CHF per month. Of course, given our NIWK (No Income With Kids) status, we’ll try to be frugal and think twice about going out for dinner and other superficial expenses. I’m optimistic that we can keep yearly expenses in the 70-75k CHF range.

[2020-02-27 Update: yeah, I wrote this post less then 10 days ago and Swiss Buffer is now 150k. Almost 50k lost in slightly more than a week. I should have called Coronavirus Monster, not Pioltello!]

At this spending regime, our buffer would last almost 3 years. This is of course “all other things being equal”. If our portfolio generates positive returns, this can last for much more. If in the meantime we earn some money, the buffer can last even more. Maybe forever?

On the opposite side, if market crashes in the near future it can send us back to Italy earlier than planned, unless we’re wiling to become cash flow positive again.

I’m a prudent person, leaning toward pessimism (which I simply call realism, or “worst case scenario planning”, or fear setting – which is part of stoicism), but I feel optimistic about the future 🙂

This is a huge shift in how we perceive our wealth. We’re kind of taking a part of it, and perceiving it as a “happiness fund“. a fund we’re ok with squandering to try to build the life we want (we saved for it).

And if things won’t go in the direction we hope, we’ll be fine with it. We would have invested 200k EUR in 2-3-4-N years of living the life we wanted. We’d wake up one morning and… “holy shit, we wasted a fortune! We only have a Million Euro (plus some) left 🙁 Let’s go back to Italy and be almost FI there”.

It doesn’t look like a disaster scenario to me.

Few days ago, a reader with whom I exchange regular mails (thanks JV!) sent me this amazing post on the More To That blog, which of course I devoured in the last 3 days. Go read it! The post resonated a lot with me. It told me that I still approach wealth with a scarcity mindset. This plan for the near future is a huge step up in the Money Spectrum. The Swiss Buffer + Ravenna Threat funds match the freedom-as-leisure and freedom-in-work stages modeled in the post. While reading it I perceived myself climbing up a ladder made of objective wealth and smiled at it. But the final twist (ok, no spoiler) hit me even harder. It resonated with Money and confidence are interchangeable, one of my preferred posts on Mr Money Mustache blog. It’s a cold shower, and a call to action.

And I’m ready for it!

Alternatives considered

Moving back to Italy soon

Live FIRE metrics say we’re at 102.16% of our original goal, which means we’d be FI in Italy.

[2020-02-27 Update: aaand we’re back at 98.39% in less than 10 days…]

Wait… let’s celebrate! Hold my beer!

Well, the target was not well designed. It was not based on real Italian expenses, Italian tax conditions, drags on Investment returns (i.e. lower SWR to consider)… it was a coarse grained target, to give a direction for the wind to blow. Anyway, even if not “really FI” in Italy, we’d be very close.

Would that be such a bad idea to move back to Italy on April First? Apart for having spoiled a nice April Fool joke, we don’t see it happening now. We feel much happier with this new plan.

But moving back to Italy in few years from now might not be a horrible thing. As I said, our parents are growing old and may need some help, our finances would be much stronger in Italy than in Switzerland, and maybe if we can skip the new fascist wave which is coming with the zombies, the walkers, the undeads, and the night king we will find a welcoming place 🙂

Having said that, a game where we reduce the “Italian FI fund” by little, while increasing the odds of living “forever” a life we think it’s better… that’s a game we are willing to play.

Setting two distinct funds

Another alternative would have been to set a specific Swiss Fund and a FI Fund, and let them grow independently. Maybe the first one just cash, and the second one with investments and cash. Dividends from FI Fund would go reinvested within it, while any other earning would go into the Swiss Fund.

Advantages:

- if market crashed tomorrow the Swiss Fund won’t be affected and we can stay in Switzerland for a more predictable time.

- We can be more aggressive with investments in the FI Fund.

Disadvantages:

- The first advantage is a lie. If FI Fund crashes 50% I won’t feel at ease draining the Swiss Fund.

- Swiss Fund will hardly sustain us after 2-3 years without a positive cash flow.

This alternative makes our permanence in Switzerland more predictable and the exit conditions random. I actually want to opposite: clear exit conditions and some randomness in the Swiss permanence.

Having a single fund means that the “Stay in Switzerland” project is connected with portfolio fluctuations, currency fluctuations and all other risk factors in our Net Worth. I’d rather keep the “Almost FI” condition (Ravenna threshold) constant (inflation adjusted), while accepting market fluctuations and cash flow events into the Swiss Buffer, with a one year grace period.

F.A.Q.

Are you still interested in FI? And in RE?

Of course I am!

I’m so into FI that after I reached it (102.17% on Feb 19th 2020) I’m going to lose it on purpose to be able to reach it again! 😀

[2020-02-27 Update: it didn’t take much, we’re at 98.39% a week after…]

Jokes apart, FI is always a goal, even if not “the” goal anymore. I think I’d design my life differently if we were “comfy FI”.

Since we’re not, I will still schedule my time around productivity. “How to make money” will be a central thought (not in the first 3-6 months, I hope), and my endeavors will revolve around chances to make some money. If money weren’t an issue anymore, I might focus on more idealistic activities for the long term.

About RE… I’m not even sure what it means now. What is Early Retirement? Am I retired now? Isn’t it more of a state of mind? Isn’t it a “spectrum” instead of a black or white thing? I think we need to rethink the concept of Early Retirement, which is what attracts most of the haters and critiques to the FIRE movement btw.

You didn’t mention investments at all. How is your investment strategy going to change?

I don’t think our investment strategy is going to change a lot. I think the investing sheet on my NW spreadsheet will keep functioning and telling ourselves where to put our money.

I already switched to be more prudent, and raised a huge cash cushion. Even too much! I’m in the process of putting money back into stocks after having chickened out in November 2019.

We will start the journey with a sizeable cash cushion (100-120k CHF in our PostFinance account), and on the investments side we have another 250k EUR sitting in InteractiveBrokers waiting to be reinvested in 2020. The plan is to Dollar Cost Average 20k EUR per month into VT, VYM and VYMI. Plus some bonds, more on bonds will come soon.

Over time, assuming we don’t earn a dime, our cash cushion will shrink. I will adjust the target down, probably down to 50k over time.

Anyway, if the question was “did you change your Investor Policy Statement?” the answer is “not yet”, but I should. It’s so outdated now.

You didn’t mention cutting expenses… Should BabyRIP go to Kinderkrippe if you’re both unemployed? Should you cut cleaning lady costs? Should you move back into a smaller flat? Anything else?

Move back to a smaller flat? Nope.

Cut cleaning lady costs: done. But maybe we’ll hire her back occasionally, like once a month.

Baby to Krippe? I think there’s value for all of us if she goes, even though it’s not cheap (924 CHF/Mo for 2 days per week).

What else… I’m still monitoring expenses and see what’s the baseline after the move settles. We know we have 3-5k CHF more to spend for the move into the new flat (a new sofa, a new bed&mattress for us, the entire Baby room, a bookshelf, and a couple of lamps), but February has been a nice benchmark month so far, with zero move related expenses and just a couple of one-offs (a new phone for me for 198 CHF, and a family yearly pass at the amazing local Zoo for 210 CHF). So far so good. We’re on track to finish the month below 6k CHF expenses, which is very good compared to last 5-6 months.

We plan to review more closely our current expenses, and to see if we can cut something, later in the year.

Anyway, I do want to take a minute of silence to be grateful for the fact that we’re allowing ourselves to stay in the most expensive country in the world, both unemployed, in a big flat, sending our daughter to expensive childcare and evaluating whether we should have a cleaning lady or not? I don’t like to brag, but I’m a bit proud of this 🙂

What about going back to Hooli?

On my side, never say never even though I don’t want to consider it for the next 11 months.

Why 11? It seems there’s an unwritten rule that if you quit in good standings you can come back within one year no question asked. But it’s not been confirmed by HR. Plus, since my performances deteriorated in last 2 years, I don’t think I’ll be welcomed back at Hooli.

Last but not least, it’s performance evaluation time right now. And I’ve done nothing to prevent a “Below Expectations” rating. Good thing is that I won’t see it coming, because the disclosure of rating scores will happen in end of April, after I quit. But I’ll get rated anyway, and that rating is going to be not good. I’m doing nothing to prevent it.

They say don’t burn bridges… I hope that in the remote case I would want to come back my story will be strong enough to overcome a not-that-amazing leave.

P.S. If you’re a Hooli employee and you want to leave an internal “unsolicited feedback” to tell me if and how I made an impact on your life… that would mean a lot to me 🙂 If you don’t know how to find me, I registered an obvious “5 letters alias” internal email address 🙂

What about unemployment insurance? Will you go to RAV?

Initially I didn’t want to go. Unemployment here is a real job. You’re a RAV employee. RAV stays for Regionalen Arbeitsvermittlungszentrum (Regional Employment Center).

Being a RAV employee means that you have monthly meetings with your tutor, must attend whatever course they send you to, must learn German at level B1 or above (they’ll send you to an intensive German course at the beginning if you don’t speak good enough), must apply for at least 10 job positions per month, and if you want to go on vacation, you accrue 5 days of vacation every 60 working days (roughly a week every 3 months).

In exchange for that, RAV (actually the Arbeitslosenkasse, the insurance) will pay you a salary which is capped to 70% or 80% (having kids it’s 80% in my case) of 126k CHF annually, i.e. 8.4k CHF gross per month. Not bad.

Do I want to do that? Add to this that if you quit your job you won’t get paid for the first 3 months, and if you get an offer you kind of must accept it or lose unemployment money. Plus they can send you to work somewhere for the RAV money, and you have no say. It means they can tell you “hey, tomorrow you go to work for this company for a month, we pay you 8.4k CHF”.

Do I want to do this? Definitely not.

But maybe the devil is not as black as he is painted.

First, the “burnout doctor” convinced me that I should do it. That I’m quitting my job for health reasons, and that he can certify my medical condition to RAV. Which means no waiting period, i.e. I get paid from day 1.

Second, one can announce themself to RAV as seeking standard employment or self employment. I don’t know exactly how the latter works, I’m going to dig into this during March. What I heard is that RAV will support you financially (3 or 6 months) if you want to become self employed, given that you’ve done some homework (like Porter’s 5 Forces analysis.. yes, I know, terabytes of bullshit), and you have a concrete plan to profitability. No need to send job applications or other bullshit.

This is still to be defined, but I think I’ll take advantage of unemployment for a while, at least to make the pay cut more gradual. In the end, I’ve paid unemployment insurance for 7.5 years, and I have certified medical conditions. On the ethic side I feel ok with that.

Plus, becoming self employed is something I want to do anyway (even if just to take my whole Pillar 2 out).

Should you rent an office/coworking space if you want to work on your projects?

I hope not.

I’m paying 930 CHF/Mo more than a couple of months ago for this new flat which has a dedicated room for my office and my sauna (LOL).

I’m also spending another 924 CHF/Mo to sent Baby to Krippe 2 days a week.

That should be enough to allow creative work to happen.

In case working from home will not be sustainable during the days Baby is at home, then I’ll look for a solution. Either a coworking space (there are two within 500 meters from home), or a Hobbyraum, i.e. a spare room for cheap rent that almost all buildings have here in our neighborhood. Our building has two amazing rooms, one of which seems not occupied. I’ll contact the landlord to see if it’s available and what’s the price 😉

Last but not Least… for how long are you allowed to stay in Switzerland without a job?

That’s a great question. I’ve been awaken by a friend/colleague: “Hey RIP, you’re an immigrant, you have a work permit. They’ll kick you out if you don’t have a job anymore!”

At first I had cold sweats.

Then he sent me a link: “here you go. You can stay in Switzerland for 6 months, then you’re out“.

Then he walked away. And I panicked.

Then I did my research, and found that’s more complicated than that, but in a positive way.

According to the Staatssekretariat für Migration (SEM):

Type C EU/EFTA settlement permit: […] While holders of a settlement permit are entitled to stay for an unlimited period of time, their permanent residence status needs to be confirmed every five years. […]

My C Permit has a control date of October 2022, so for the next 2.5 years we should be fine. My wife and daughter C permits are even fresher. I don’t know how weird would it be if I will be kicked out from Switzerland while they could stay. Btw, if by October 2022 we are still both unemployed with no income I guess it’s time to leave anyway.

There’s also the option to stay in Switzerland without gainful activity.

Again, from SEM website:

Economically inactive persons must have sufficient financial means to ensure that they do not become dependent upon Swiss social security benefits (welfare) and therefore a burden on the host country;

Economically inactive persons must be fully covered by health insurance (all risks, incl. accident insurance).

Financial means are deemed adequate if they exceed the welfare entitlement threshold established under Swiss law

I think we can demonstrate enough “financial means” even at my C permit expiration control time, just in case.

Last but not least, on Englishforum (which is not the law, I agree) people seem to take it easy with a C permit and no job…

Btw, my C permit control time corresponds to my 10 years in Switzerland, which means I could start the naturalization process and obtain Swiss Citizenship. Now that I think about it, October 2022 would be quite a benchmark for our plans…

Let’s face the elephant in the room: How do you plan to generate money?

It’s a tough question… and as I said I don’t think I have the clarity to answer right now.

I can give you a list of possible options:

- Find another job in my field? A startup? A non profit? This is not a solution that I take into account right now, but I don’t exclude I’ll go this way in a year from now. Even though I consider myself unemployable right now, I know that going back to Plato’s cave is the easiest solution. I’ll try to resist. It seems a joke, but after I sent my resignation letter recruiters are contacting me 10x more frequently. Just today I received an interview offer for Congo Rainforest, Web Services division :I It will be hard to ignore the inflow…

- Freelance/Consultancy/Training, maybe part time/seasonal? That’s also another option. I’ve talked with a few people living a very good life working as contractors / freelancers. Being able to control where to work from and being in control of their working time. I already did that for 2 years, and it’s been the best time of my career! Why not try it again? Well, not in the near future, but I guess it will look like a very interesting option in a year from now.

- Become a Financial Advisor/Planner? Get an official certificate for it? That’s something that excites me right now. I may decide to take a serious certification like CFA or CFP and take the financial coaching one step further. In a recent Compound episode, Josh and Michael pointed out that “financial advisors don’t retire“, and that’s probably because it’s a nice job, well paid, with all the positive aspects of a freelancing job (work from everywhere, you decide how many customers to handle, you decide how much you want to work).

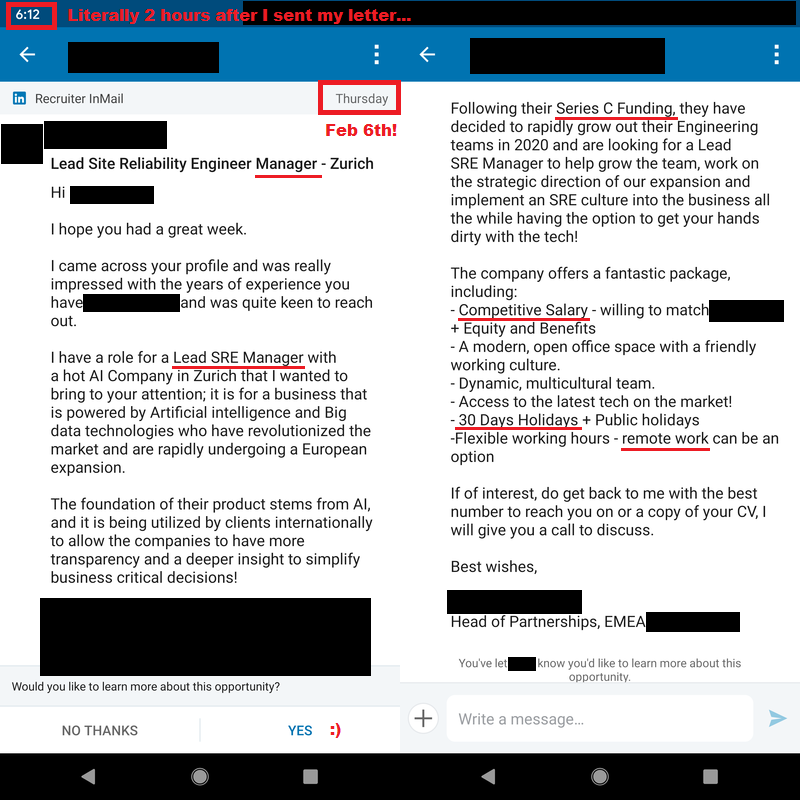

- Try a real job (maybe part time) that excites me. People manager, community manager, teacher assistant and so on? Yeah. That could also be an option. A regret I have at Hooli is that I never got that extra promotion that would have allowed me to manage people. I think I’d be a good people manager, and I have hard time convincing recruiters that I’d be good at it outside Hooli. Just on the same day I sent my resignation letter, a recruiter contacted me to check if I’m interested in a Site Reliability Engineer Manager position at a company paying Hooli-like salaries. I thought it was a joke. It took me 2 hours to craft the resignation letter and to click “send”… and two hours later I accepted to interview for a manager position? LOL. Anyway, I’m letting this application die. Not now, not today. Call me back in six months.

- Do not care about money and do whatever I like, at least for a while? Things like blogging, coaching, writing a FIRE book, writing a fiction book, do standup comedy, act in theater, teach theater acting, launch a podcast, start a YT channel, create online courses, help people with career development, take another degree, focus on my health, focus on my family, teach Youniversity, all the other things I mentioned here… Yes, that’s where my guts are telling me to go now.

- Do a mix of the above (work part time or freelance while blogging)? … and that’s where I’ll probably end up in few months from now!

{kind=link}

So I’d probably just work on my passions for “a while”. For sure until this summer, I owe it to myself and my family.

Then we’ll see what happens, and where the rhythm of the music, the waves, the randomness of life will drive us. Life is not a journey. What will I want to do in few months from now? I know not.

My hope is that I could implement the Passive + Passion income model by Miss Montana. But as I said, I know not (yet).

And it doesn’t mean I don’t have options, or I have no idea. It just means I don’t know yet which way I want to monetize my skills. I might start the CFA or CFP certification, and kicking off a new career. I could keep doing coaching (maybe improving the quality of my job), offering career growth support (how to pass a coding interview), or manage actual people money… or any one project out of the ~150 entries in my 15 pages doc titled “Crazy ideas on how to make money in the future” (not shared here, sorry).

I mean, I have a lot of options. I’m aware of that, and I’m extremely grateful for it. I just don’t know which one I want to pursue yet. Right now, all I want to do is to not focus on making money, and just express my creativity.

The good news for you (I hope) is that the most obvious channel where to convey my creativity is this blog.

I will focus on this blog, on writing (more technical posts, promised!), on networking, on meeting people, on having fun.

I’ll try to adhere to a strict schedule: working in the mornings, ideally 6 hours a day (7am-1pm, maybe more in the Krippe days), and spending afternoons/evenings doing sport, enjoying leisure time with my family and friends. Maybe coaching in the evenings, but not after 10.30pm I promise (to myself!)

Yeah, that’s all.

Wish me good luck!

You have many options, but you are not retired yet. It takes time to recover from a burnout, but then you must choose what to do next. Personally it took me 1 year to recover from my own half burnout, I had many ideas but finally I decided to really retire, quit the corporate bullshit and live the good life.

Ok. I was tempted to put “retired” on Linkedin btw 😀

With a C permit you can also leave Switzerland and come back up to 3 years later, as long as you notify the immigration office upon leaving. This may be something to consider if you want to try Italy

Yes sure, we know that 😉

You mentioned the problem with tax authorities in a recent blog. They might tax you as a professional invester, since your living expenses are paid throughout your investments. What are you going to do about that?

First, if they tax me for capital gains it means market in 2020 will do great, which would not be a bad news 🙂

Second, I don’t think this is going to happen this year. this year I still have a significant income (3 months of Hooli, bonus, maybe unemployment). I bet 2020 income would be above 100k CHF.

Third, even if I earned less and the market would do great, I’m behaving very “not professional” this year, following the 5 steps to not be considered an active investor. unless profits from investments would be greater than salary (which is hard in 2020) I don’t fear it coming.

Fourth, I know people with much more money than me that play riskier games (options, leverage, value investing) and still are not classified Pro. It seems being classified as a Pro very rare. See this comment here: https://retireinprogress.com/i-did-something-im-not-proud-of/#comment-1849

I spend 7k eur per year in Germany, my head spins when I read about the 7k per month 🙂 Combined with my wife and small baby it’s not more than 16k/year or so. E.g. the Krippe will cost me about 400/month for 5 days a week, then the Kindergarten is similarly free. The quality of life is definitely not 3-4x worse than Switzerland.

Yeah, I gasped at the 7000CHF/month figure, too. I think the RIP family could, after careful (re-)consideration of their expenses, FIRE in basically any country in the EU. The German border is a mere hop of 20km from Zürich. The standard of living there is, like, the same, isn’t it..?

Standard of living might be “like the same” (nope, they’re definitely not!) but it’s more about our connection with our community. Our roots are here.

Welcome to Switzerland!

Germany is a very remote option for us, but not one we assign zero chances.

Don’t forget your ahv liabilities which can be substantial when unemployed. Also for your wife.

You’re f***ing right… I think for 2020 we’re covered by salary and eventually unemployment (we’re paying contributions) but I need a solution for 2021 or else it’s another X CHF per month.

Ah. OK. I mis-read your post initially as not wanting to take RAV – which I would not advise both for the loss of income and the AHV on top. I had thought that you would get no RAV support in case you are trying to become self-employed (but happy to be proven wrong). Any low income self-employment will also impact future RAV benefits.

What do you mean by “Any low income self-employment will also impact future RAV benefits”?

You mean in a positive or negative way?

I really enjoyed reading your thought process there, had to laugh at the concept of ‘stupidiFI’. Wishing you the best in going forward!

Thank you, I’ll keep you all posted 🙂

Hi RIP

With a C permit you can stay as long as you want in Switzerand:

Die Niederlassungsbewilligung C ist unbefristet und wird ohne Bedingungen erteilt.

Betroffene verlieren ihren Status bzw. ihre Bewilligung nicht bei Arbeitslosigkeit.

Sind sie jedoch längere Zeit und in erheblichem Umfang von der Sozialhilfe abhängig, kann ein Widerrufsgrund erfüllt sein und die Bewilligung kann widerrufen werden.

Regarding your expenses I think that your monthly budget should be approx. CHF 1000 more, i.e. at least CHF 7000 given your fixed cost of approx. CHF 4000 (flat + child care + health insurance). It´s quite difficult to live a “decent” life in Switzerland with less. It´s also more in line with your current spending. This additional CHF 12000 should´nt change your financial numbers so much.

It’s not guaranteed that you can stay forever in Switzerland. It’s still a work permit and I’ve read stories (extreme ones, though) of people being kicked out with a C permit.

6k vs 7k is a huge deal. Closing the gap from almost 4k CHF/Mo (what my Nest Egg could generate at a 3.5% SWR) would be easier.

This month we’re below 5.5k by now (Feb 25th) and that’s very promising 🙂

Hehe this reads like the extended version of the summary you gave me on Monday. One thing which is unclear to me. Isn‘t receiving unemployment money the same as social wellfare regarding the resident permit?

And I see you added the Cookie warning 😉

Maybe unemployment money are considered social welfare, I don’t know.

My wife recently got the C permit and she’s been on unemployment for almost a year. So they didn’t matter.

Also, my C permit control date is in 2.5 years, and I don’t plan to still be unemployed then. If we’re staying here and going for Citizenship in 2.5 years I think I’d do my best to look attractive to Swiss Authorities 🙂

Cookie warning is just the beginning, more legal GDPRy stuff are coming

In my opinion Ravenna is a great place to live, in general in Emilia Romagna there is a high quality of life, with high standards in services such as school, healthcare and university. Also in Ravenna you are very close to beautiful places, sea and nature. Furthermore, it is not to be overlooked from a logistical point of view that you are also close to the Bologna high-speed station and to an excellent Bologna airport with many international flights, including low-cost ones, in March the new monorail to connect the central station and the airport is inaugurated, further improving the interconnection for those who want to avoid using the car to reach the airport.

You may also already know that the University of Bologna plays a leading role internationally in the field of Artificial Intelligence. The new international master’s degree in Artificial Intelligence has achieved very positive results, with hundreds of requests to participate from all over the world. The new course, in English, focuses on the founding and applicative disciplines of Artificial Intelligence: knowledge representation, reasoning, machine learning, machine vision, data science, data optimization, decision support systems. This is to tell you that there are new and interesting opportunities in innovative sectors for those with excellent mathematical and computer skills like you in Italy.

However continue to prioritize the recovery of your best mental and physical health, the rest does not matter.

Good luck!

Massimo

AWSOME! Ravenna it is! Not today though 🙂

Thanks for stopping by, Massimo!

Ciao Mr. RIP : )

A typical “Hooli” question:

When you say “A regret I have at Hooli is that I never got that extra promotion that would have allowed me to manage people. I think I’d be a good people manager, and I have hard time convincing recruiters that I’d be good at it outside Hooli.”

Then, as a Manager (brrrr… starting sentence creeps ; ), what would have you done with a Team member like you. For sure this will help me to grow and understand something new. Thanks.

I’ve been living out of Italy for the last 14 years. Some “little” comments:

– You will always be able to get back so Italy, anytime you want.

Think about Abruzzo, if it’s community you look for, then you’ll like it.

When you’ll move away from Switzerland, imho it will be very challenging to get back, so think about it carefully before you move (as you always do atomically ; )

In my case, making a stand firm decision on which country I wanted to live for the next 10 years, improved pretty much all aspects of our live (wife + 2 kids in CH), even in short term. It kinds unblock me mentally and emotionally, maybe something can be re used (like mail client instead of rewriting a new one ; P). Whatever is your decision, your parents will understand and accept it. Maybe

And yes, as a father, you are responsible for your decisions now, that will influence Baby RIP life in the future. I don’t see any mention to 2th Baby RIP though in next 2.5 Years plan… things can go better, but from FI perspective even worst 😀

A pleasure to read your blog. Feels like being at home sometimes. 😉

Thanks,

Daemontool

Hi Daemontool, very good question “As a Manager what would have you done with a Team member like you?”

This question can’t be answered in a vacuum though. It’s not a single side. For example, I would have loved to approach the employee (me) and asked him “what would make you happy here?”. I know myself, I’d have answered “autonomy, mastery, creativity, purpose… and no corporate bullshit (meetings, reorgs, pretending, stack ranking, change of directions, paperwork, stand ups…)” then the problem would have been to find a way to make the employee thrive AND the company happy. If the company has no room for employees personal satisfaction it would have been hard to keep an employee like me. But I know I’m a hardly employable person, I’ve never been happy as an employee. Best time of my career has been when I was a freelance. Luckily, for myself as an hypothetical manager, most employees are easier to manage I guess 🙂

Of course when (if) we’ll leave the country we do it after tons and tons of spreadsheets. Btw, you think Abruzzo is a good choice for a semi-retiree? Why? I’m curious 🙂

Good point on making a decision and deliberately not look back for a specific time frame. To brood over past decision and second thinking yourself all the time doesn’t help. If a decision is made, there’s no looking back 🙂

That’s the goal of our grace period of 1 year (I can’t think 10 years in the future for now), and our current plan with triggers and thresholds.

You don’t see mentions of 2nd kid, but we’re thinking about it. We’re both old, and the opportunity window is closing soon. Right now is not the best time, but this summer we’ll sit and talk about it. Biological clock is ticking faster.

Thank you for your comment, it made me think a lot!

hey RIP,

one thing that crossed my mind reading deamontool’s feedback is that you will also reach a point where you must consider the impact on your kid(s) from moving countries. you probably have ample time for that but once kids start school somewhere it may impact them adversely to move.

in my case they’re gonna start kindergarden this fall but i am contemplating moving to the US. i would not move there permanently, i already know this, so i sort of need to understand the impact on eventually returning…dialect is hard :))

Yeah, I know and I care about that as well.

We’re “lucky” that our daughter is not yet 2 years old and we have at least another 2-3 years of exploration before impacting her life too much with many moves in the delicate learning age.

It seems the stars align pretty well: C permit control date, Swiss Buffer (expected) expiration date, and kindergarten starting date: Fall 2022.

Let’s see.

Hi Mr RIP,

A note regarding unemployment benefits salary ceiling: it went up from 126’000 to CHF 148’200 in 2016. Therefore, you would qualify for 80% of that figure, i.e. CHF 9’880 monthly.

Also, unemployment benefits are not considered “welfare”, so no worries about your C permit status, for a while yet 😉

I’d just like to add that I love your blog, your style, intelligence, wry sense of humour and openness. I look forward to every post.

Wishing you all the best on this next phase of life’s journey. (Ich drucke Dir die Daumen.)

Oooh, that makes unemployment waaay more interesting!

Thank you so much Halcyon 🙂

Ciao MrRip,

it’s a pleasure to read your blog.

I wanted to ask you if you ever analysed the taxation situation in Italy. I am trying to get my head around it but the topic is quite complex (and boring). However it has a big impact on the FI target.

My understanding is that capital gains are taxed at 26% in Italy. On top of this there is a 0.2% tax on financial assets held abroad (I guess that US or IE domiciled fund belong to this category). All in all that is significant!

There is a new advantageous regime for foreign pensioners transferring their tax residence in the southern regions of Italy (including Abruzzo 🙂 ) but a part of the income should come from a legit foreign pension fund (OUCH!). The regime is a substitute tax of 7% on any foreign income and allows exemption to the 0.2% tax on financial assets held abroad (http://kluwertaxblog.com/2019/01/11/italy-a-country-for-tax-savvy-old-men/).

Another tax incentive is the so called “rientro dei cervelli” for people relocating in Italy and producing income in Italy. Under this regime there is a tax exemption of 50% or 90% for a move in the south of Italy. However capital gains do not seem to qualify a income earned in Italy (OUCH again!).

I am curious to hear if your understanding is similar to mine and to know your views about this topic.

Best of luck!

Rico

P.S. My target italian region to retire is Abruzzo. Disclaimer: I’m from there so I’m heavily biased. However I can say that it is considerably cheaper than more popular destinations like Marche, Umbria and Tuscany while being really similar to these regions in terms of climate, food and culture.

Hi Rico,

I know Italy is in the business of extracting money from those who have some, especially if legally earned and virtuously saved. That’s a pity.

I didn’t run the math, I just assume that:

– SWR must be lowered to take into account the 0.2% tax, plus eventually any wealth tax (Patrimoniale) they will introduce. Because they will.

– monthly allowance should take into account Capital gain tax, which asymptotically goes to 26% over time, as proceedings from SELL actions approaches 100% capital gain. I would use an intermediate tax level, like 15%.

I can elaborate on this if you want.

In simple words: let’s assume you buy something at price 100 and it grows by 10% per year.

– If you sell it after 2 years you sell it at 121, realizing 21, paying 5.46 (26% of 21), which is 4.5% of withdrawn amount (5.46/121).

– If you sell it after 10 years you sell it at 259 (100 *(1.1^10)), paying 26% taxes on 159, which is 41.34, which is 16% of withdrawn amount.

– If you sell it after 30 years you sell it at 1745 (100 *(1.1^30)), paying 26% taxes on 1645, which is 427.7, which is 24.5% of withdrawn amount.

As you can see, over time the portion of sale price which is capital gain grows, and your taxation approaches 26%. But it does this over time.

Few considerations:

– taxes are lower at the beginning, which helps

– taxes are lower if your investments don’t do very well, which helps! We’re usually too conservative and like to plan for the worst case scenario. In this example your asset is growing by 10% per year. If the asset grows only 5% per year (or worse), tax impact would be even lower. TL;DR: you pay more taxes when things go well, which won’t impact your worst case scenario by much.

– dividends are not considered here. I guess it’s more tax efficient to invest in accumulating (thus non-US domiciled) ETFs. You pay taxes on dividends even if your fund lost 50% of value due to a market crash

– inflation in your fiscal currency can rip this thing apart. If tomorrow Italy quits the EURO and print Liras, you’re going toward full 26% faster. Maybe your USD denominated fund grows by 0% this year, but if Liras inflation is 100% your fund value in Liras doubles, and in Liras you’ll be taxed.

This comment is long enough I should have made a post about it 🙂

And it’s not over yet!

About the special regime for foreign pensions and “Rientro dei Cervelli” I read so many unofficial things that I decided to stop. I’ll investigate that issue if/when we move back.

About Abruzzo, we should have a talk sooner or later 🙂

Hi RIP,

Just wanted to mention that I am originally from the Romagna area you mentioned in the post (indeed, I basically grew up in one of the towns you mention). Even though I have been living abroad for a number of years now, I go back to visit fairly often, as an important chunk of my social and family network is still there.

So this is just to say that I think I still have a good grasp of daily life in that area. I won’t write here a mile-long post with what I believe are all the pros and cons, as these things tend to be fairly context dependent, but in case you have any questions about that area (or even specifically about those places you mention) I would be very glad to be of help.

So feel free to contact me – I think you should be able to see the email associated to this comment. Even if you decide you are totally fine in Switzerland now and you go back to this potential plan in 2022, feel free to drop me an email then, I’ll be happy to help.

This blog has been a great help to me since I found out about it (hell, I really wish I found out about FIRE years ago, I am ten years late to the party and my retirement day is far and hazy in the future…), and your investment strategy and discussions have been a great source of inspiration for me (except that I am really poor at this game, my total NW is less than your cash stack, oh well!), so I’d be glad if I could give something back.

Cheers!

Thank you Matteo, welcome to retireinprogress 🙂

I might contact you… sooner than planned, given that the Swiss Buffer lost 50k in 10 days!

Hi Rip,

congrats for the decision taken for change. Taking such decision requires a strong guts and bring together a lot of mixed feelings.

You are a remarkably careful planner considering all aspects, planning different scenarios, deciding on the location where to live based on defined parameters. I liked the pick of Ravenna, I was there only once, a rainy day working day, not a relevant memory, but I trust your points and from other experiences it is true that people in that are are nice that is one of the most important points in making a place.

Still I was intrigued by the fact that among parameters I did not see any reference to the education system. I have also being living close to Zurich for the last 6 years, I love the place, still sometimes the idea of going back to Italy crossed my mind. Now I have 2 kids, ages approaching 3 and <1 and one of the points that makes me always think in taking such decision is the education system of one country vs the other. I think about the basic one no private schools or super duper universities. I must say that I did not document me enough, it never feels enough given the amount of variables :-), but differences seem to be relevant!

About financial markets lets see where the virus will bring them. Honestly we could think that this is a bit a overreaction, in general, but we could also think that the markets were overinflated 🙂

All the best and keep up! however it goes you’ll find a rewarding way!

Thanks Francesco, and welcome to retireinprogress 🙂

About the education system I must admit I don’t like the Swiss one much. That’s why I’m not putting emphasis on “how cool is education here compared to XYZ”. The Swiss system is pushy and if your kids are not in the top X percentile at the age 12 they’re put on a slow track and denied university. Young kids here are forced to “know what they want out of life” very early in their life, that’s why you see “Leerhe” for almost everything, even to become a cleaning lady at age 16. That horrifies me. Add to that that our daughter is “not Swiss”, which could add another layer of prejudice… I have friends with teenager or preteen kids who tell me that it’s not a very relaxing environment for kids. I also have heard from a couple fo friends with grade school age children that here they tend to take quick countermeasures as soon as your kid diverges from “the average”. Is she a bit (5 decibel) too noisy? ADHD. Take those pills. Does she hug other kids? Take those pills. Does she miss a word out of 100 by the professor? She doesn’t speak perfect (Swiss)German, take those extra classes and go fuck yourself a couple of extra years in a slower classroom and goodbye university.

I’m not sure it’s the education environment I want for my daughter.

Amazing analysis!! Bravo. I admire Your thought process, providing transparency, taking the time to writing them down, transmitting them…..I can go on. All the very best. Bon vent. Partha

Thank you Partha, I really appreciate your nice words 🙂

Hi Mr.RIP,

From time to time I come by here because I am abroad Italian too. I gasped (like many) at ll the numbers. I knew Switzerland is another level, although I did not expect the difference that high.

Nice places very near to Switzerland which I consider “almost swiss” from mindset and quality are Vorarlberg (A), Südtirol/Alto Adige (I), Nordtirol and Osttirol (A). The Italian one is multilingual, has good infrastructure and autonomy, the Austrian ones have very good welfare system and infrastructure.

I think you are doing great and you can relax. I also work in IT since 20 years and feel the strain of being confronted with problems all the time. My theory is that this changes your brain in the long run and that is why many in that area seek peace of mind and seek to “express creativity”. I don’t have perception that we will ever have trouble finding a job though, especially the ones who are good at solving problems.

Sincerely,

Vasquita

Hi Vasquita, welcome to retireinprogress 🙂

Which “numbers” you gasped at? Our expenses? Well, Switzerland is expensive. A Family is also expensive as well, people tend to forget that 🙂

Good point about how IT destroys you from within and one needs to seek calm and creativity after a career in IT.

But it’s not the same for everyone. I kind of envy those who can survive (and thrive too) in such environments. I think it’s like the army. You have to be “wired in a certain way” to enjoy it.