Hi dear readers,

Yes, two consecutive posts on our financial update. After this one I plan to publish another personal post (about the flat move), then it’s time to put my hands on some technical topic 🙂

NOTE: brace yourself. This is by far the longest post on this blog. It’s 16k words long. I’ve never crossed 10k before. I know, it’s a lot. But it’s adequate to the intensity of my life in October-December 2019. My blog so far has been a mix of technical and personal posts. Lately, personal posts have been taking over but trust me: a lot of technical posts are coming.

As I said in last update, Q4 has been really tough. Went back to work with some enthusiasm, which turned out to be just delusion that I could have made things work. Plus a flat move, continuous sickness, lack of sun for a month and so on. My health (both physical and mental) is declining again, and I’ll do whatever it takes to invert the trend in 2020.

Table of Contents

Let’s start from the financials, then we move into the personal as usual. Also time for a end of year and end of decade review 🙂

“But RIP, the decade ends at the end of year 202…”

Shut the f*** up! The decade ends now! Because like previous one, the passage from 20X9 to 20(X+1)0 also marked a big change in my life. I’ll write about it soon.

“But RIP, you promised some technical post… I want to know which ETF I should buy for Emerging Markets small cap….”

Yeah, I know… I lied.

I want to write a looong post about the parallel between 2009/2010 and 2019/2020.

I’m sorry, my blog my rules 😉

Back on track. How did our quarter go from a financial point of view?

Metrics & Financials

Overview

Our Net Worth document is available with live data on Google Drive. The new 2020 sheet set (NW and expenses) is live since January 25th. I decided to share an exact copy of my private doc. I’m still trying to avoid the pain of duplication and maybe share directly the private one after some obfuscation. I’ll play a bit with the docs in February, I’m sorry if in the meantime the public doc may get out of sync for a while. But at least now you have more formulas 🙂

Overall it’s been a very good quarter, thanks to Mr.Market (even though I sold a lot of assets), 120% salaries (more on this later), end of year huge Hooli stocks vesting, and announced yearly bonus that will be cashed in January but I already accounted for it to be consistent with previous years.

Even though I played the pessimistic card the entire year, I’m acting optimistically here. The bonus will be paid with the January salary, and the risks of not getting it are close to zero even if I announced I quit Hooli. I guess even if I get fired in January (unless it’s for some severe reason). So I guess it’s ok to be optimistic.

[January 25th Update: Bonus cashed 🙂 I managed to not screw things up]

On the dark side, we’ve spent a lot of money. Cash flow is my main concern nowadays. In November we raised our baseline spending by 2k CHF (BabyRIP’s Krippe, and a bigger flat), and we’re facing one-off relocation expenses in the order of 10-12k split over 3-4 months. Before November, our baseline was 4k, and I considered a partial success any month below 5k. Now the baseline is 6k. I’ll let the storm of “new furniture for the new flat” pass, then I’ll be actively controlling our budget to keep our monthly spending not far from the new baseline.

Net Worth

NW (in EUR): 1.169M (Delta: +85.1k), another all time high. I stare at these numbers with apathy. I should stop and celebrate a bit, but I can’t. In December alone our NW grew by 51.9k EUR. It took me my first 35 years of my life to go from zero to 50k EUR Net Worth. Now it’s a month’s delta. It could have been even better if the USD didn’t tank. In fact, measured in USD our December growth is almost 81k. More than the value of the flat I sold in July!

NW in USD crossed 1.3M, with a quarter Delta of +130k! As I said, this is mainly because USD has been weak compared to CHF and EUR in Q4.

This quarter by month:

- October: +6.6k EUR. Both Mr.Market and cash flow have been very good, what made this month not stellar has been a strong EUR compared to both CHF and USD. In the two other currencies we’re in the +20k/+35k range.

- November: +26.7k EUR. Again, very good Mr.Market, not so good cash flow. This month USD has been the strongest currency, thus a good NW Delta in EUR. Sadly, I sold a lot of stocks by end of November.

- December: +51.9k EUR. Another borderline irrational Mr.Market run (which I didn’t fully benefit thanks to my November sell off), and a predicted huge income. On the negative side almost 11k CHF expenses, and a weak USD. And I’m more exposed to USD than I have ever been.

Our NW evolution during 2019 by month:

This has been the best year on record, with a Yearly ND Delta of +317k EUR (above +300k in all currencies). The second best year in our history is 2017, with a NW Delta of +183k.

Who would have expected that?

In 2018 we crossed the Millionaire status in CHF and USD few times, back and forth, and we closed the year with a NW of ~850k EUR. During the fourth quarter of 2018 the S&P500 lost almost 20%, and the world seemed close to financial collapse, the end of the current financial cycle.

The Bull was called dead.

Wrong!

In my December 2018 Update, in the “expectations for 2019” section I wrote:

My dream goal is to reach 1M EUR, but I don’t see it coming, unless 2019 will be an amazing market year and/or a shitty EUR year.

Nope. We’ve exceeded “dream goals” by 170k EUR 🙂

This is our historical NW, with 2019 highlighted:

Previous years NW deltas have been dominated by savings. This year the impact of market returns has been comparable with savings. Even though S&P500 total return for 2019 was 31.5% (or 33%, depending on how you count initial value: Jan 2nd opening or Dec 31st closing price?), our portfolio Time Weighted Rate of Return has been 23.58%.

On top of that, we held a lot of cash during 2019.

We could have done better.

Cash Flow – Income

Total estimated Net Income (after tax and Pillar 1 contribution) for the quarter is: 79.1k CHF.

Estimated Net Income (after tax) by month:

- October: 12.3k CHF. Base salary and some dividends.

- November: 15.6k CHF. 120% salary and Pillar 2 reimbursement for long term sick leave (2.5 months of contributions, pre tax).

- December: 51.2k CHF. Salary, 13th salary, a huge stocks vesting event, and dividends. The yearly bonus is accounted for in “Other – CHF” (Cell O50 of the 2019 NW spreadsheet), but it’s not part of the cash flow since it will be cashed out in January.

December income has been all time high!

Income streams breakdown:

- Salaries: 52.9k CHF (gross, pre-tax). Very good months!

- Hooli stocks vesting: 34.6k USD (gross, pre-tax). Hooli stocks performed very well this year 🙂

- Dividends: 2780 USD + 45 EUR (gross, pre-tax). Could have been more if I didn’t sell 300k stocks ETF in November.

- Expected Income taxes: -17.8k CHF. According to my 20% average tax bracket estimation. High taxed-as-income (salaries, dividends, stocks) income, high taxes.

- Mr RIP Pillar 2 Contribution: 7956 CHF. Same as always. This is the amount that gets credited into my Pillar 2. I pay 50% of it, and it’s already accounted for in the above salary (which is pre-tax, but after pillars 1&2 contributions). In November, I actually got reimbursed ~3k CHF for 2.5 months of my contributions during prolonged sick leave after 3 months.

- Expected Lump sum Tax on Pillar 2: -477 CHF. According to my 6% lump sum tax estimation.

- Other Income 340 CHF: 150 CHF Home Internet reimbursement at Hooli for Q4 (a Reliability Engineer gotta be reliable), 100 CHF for Mrs RIP’s sales of toys and unused baby stuff, 50 CHF Migros Blue Coupons, 40 CHF a neighbor’s gift for BabyRIP.

2019 estimated net yearly income: 254.6k CHF. Best income year of my life. I didn’t say “so far” on purpose.

Compared with previous years :

- 2016: 191.2k CHF.

- 2017: 250.1k CHF. Without wedding gifts (which compensated wedding expenses): 227.6k CHF.

- 2018: 242.2k CHF.

- 2019: 254.6k CHF.

It looks like stagnation, even though it’s a great stagnation level I’d say.

Mind that these numbers represent total family income, and in 2019 Mrs RIP didn’t work (only brought home 7 months of unemployment benefits). We managed to beat previous years only thanks to Hooli stocks price bump, and dividends growing linearly with net worth.

2020 will be different. Much different.

Cash Flow – Expenses

Yes, you read it right. Almost 11k CHF in December, 6.8k of which in the housing category. I’m accounting for moving costs into housing, of course. I have a separate spreadsheet for our move, with a specific furniture budget and other costs. As of Jan 25th 2020 our expected total moving costs would be ~15k CHF. A shitload of money. Roughly 9k has been already spent, still 6k to go (according to our budget) which means the “baseline spending months” are still far away.

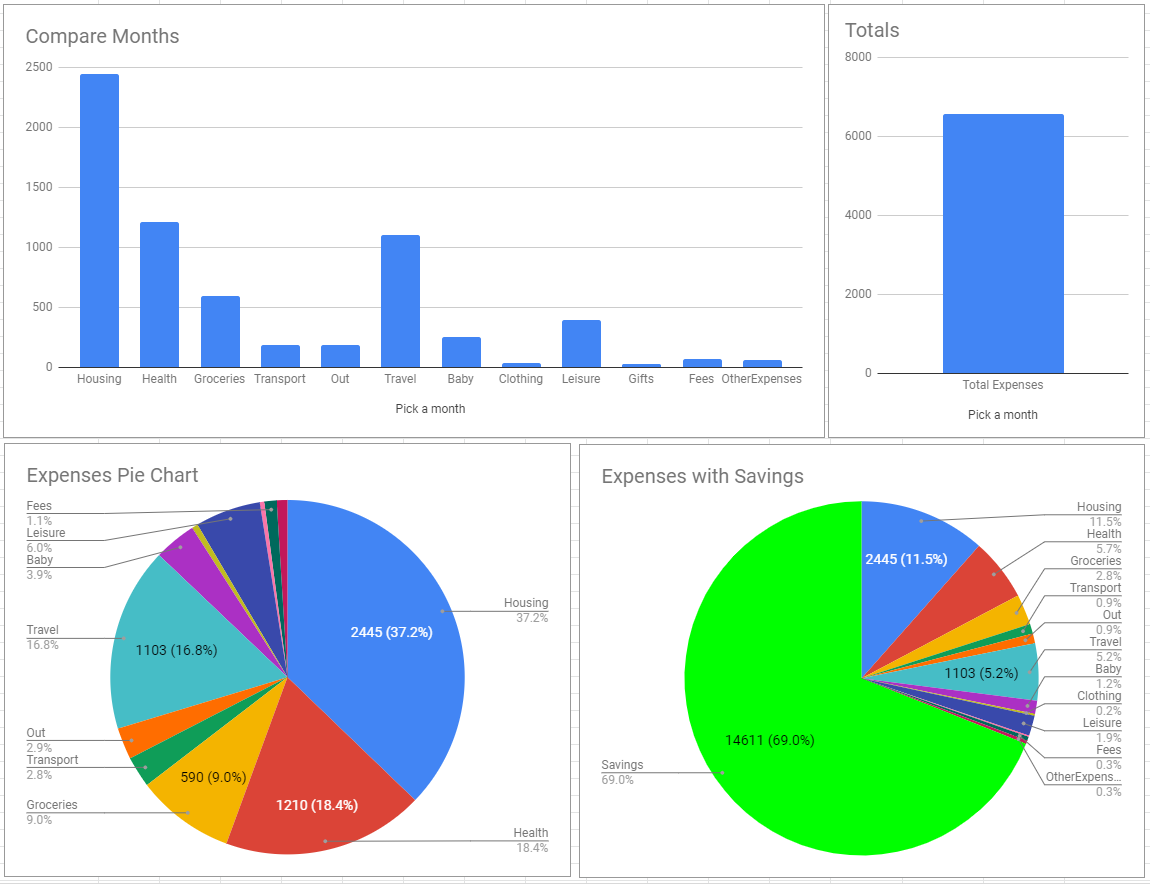

Total Expenses for Q4: 24705 CHF. Average for Q4: 8235 CHF/Mo.

Total Expenses for 2019: 78901 CHF. Average for 2019: 6575 CHF/Mo.

It hurts me to acknowledge that. Close to 80k CHF of expenses in 2019. Worst year on record.

All time high expenses impress me more than all time high earnings or all time high NW Delta because this one is the only one who might last for the following years, maybe even get worse. And that scares the hell out of me. It’s a 27% increase compared to 2018 expenses.

Compared with previous years :

- 2016: 59.7k CHF. Less than 5k CHF/Mo on average, including vacations and one-off expenses. Good.

- 2017: 91.2k CHF. Without wedding expenses: 63.4k CHF. Could have done better, but… Maldives, you know…

- 2018: 62.0k CHF. BabyRIP was born, still expenses looked good.

- 2019: 78.9k CHF. A Disaster! I had to fight burnout, and that meant (in the short term) relaxing some frugality constraints, go travel around a bit more, higher medical expenses. Plus, toward the end of the year, expensive child care for BabyRIP and a flat move.

It’s a steep increase over the last 4 years, and since November 2019 our permanent baseline grew by ~2k CHF/Mo.

The goal for 2020 is to keep the monthly average as below 7k per month as possible. I remember the time where a month below 4k expenses was a good month. Given the +2k baseline (child care for BabyRIP and new flat), a month below 6k (72k per year) should be celebrated. I expect the average month to be around 7k CHF expenses (84k per year). Considering some extra (vacation? missing furniture and moving budget) we could reach 90k expenses.

I’d be happy if we can stay below 80k, but it’s a very optimistic goal considering that health expenses are not going to go down much, and also considering that there will be “extras” waiting for us: 2 weddings (friends and family), old landlord asking ~1k CHF of damages (assholes! It’s not true!) in the old flat and so on…

[Note: on January 23rd our old landlord agreed that the damage they were claiming on the kitchen was not our responsibility. It helped to have recorded a lot of things hashtag datahoarder!]

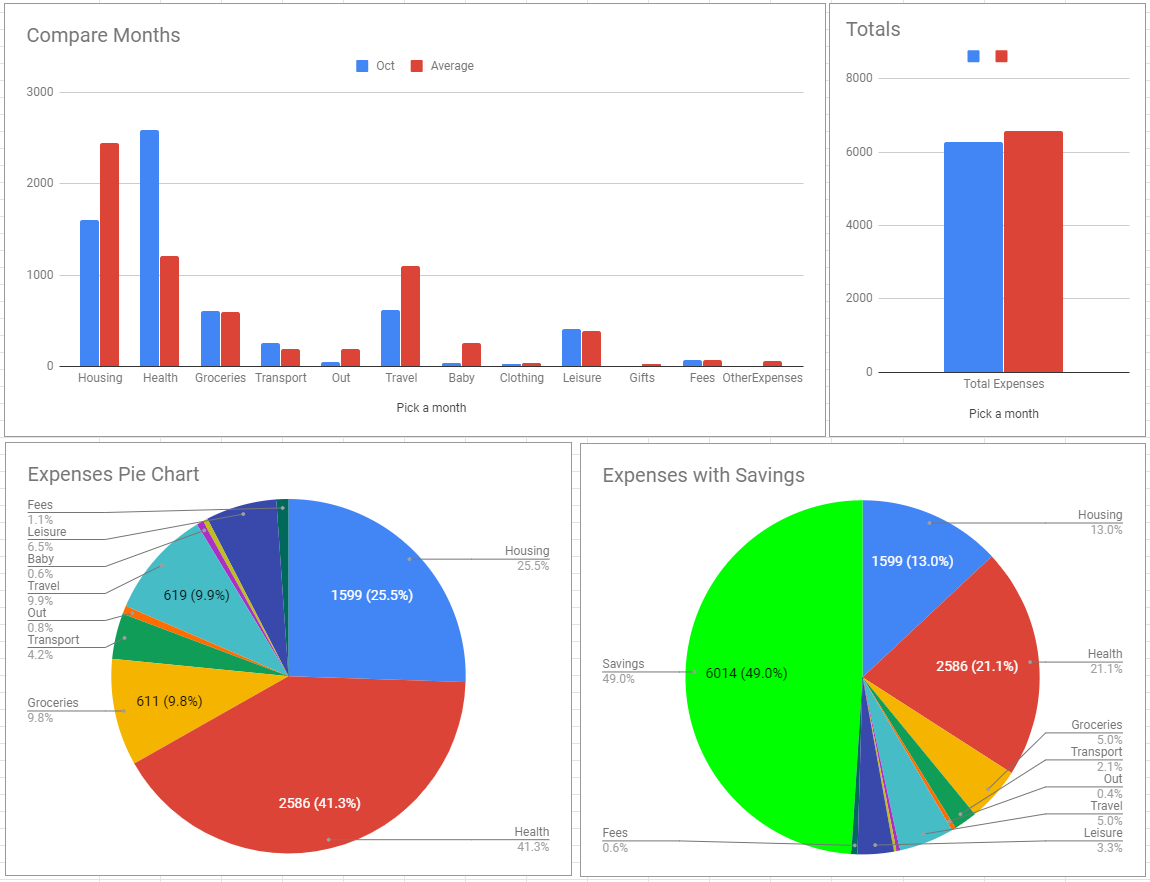

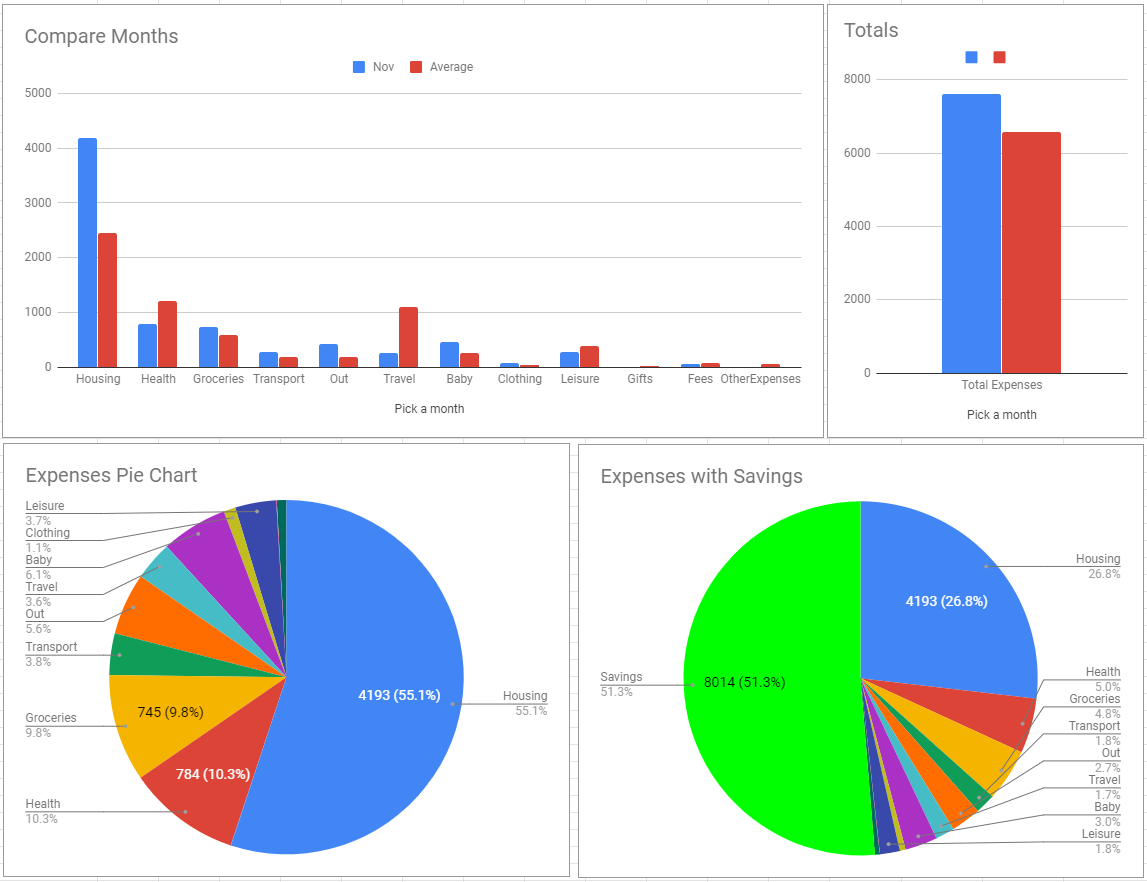

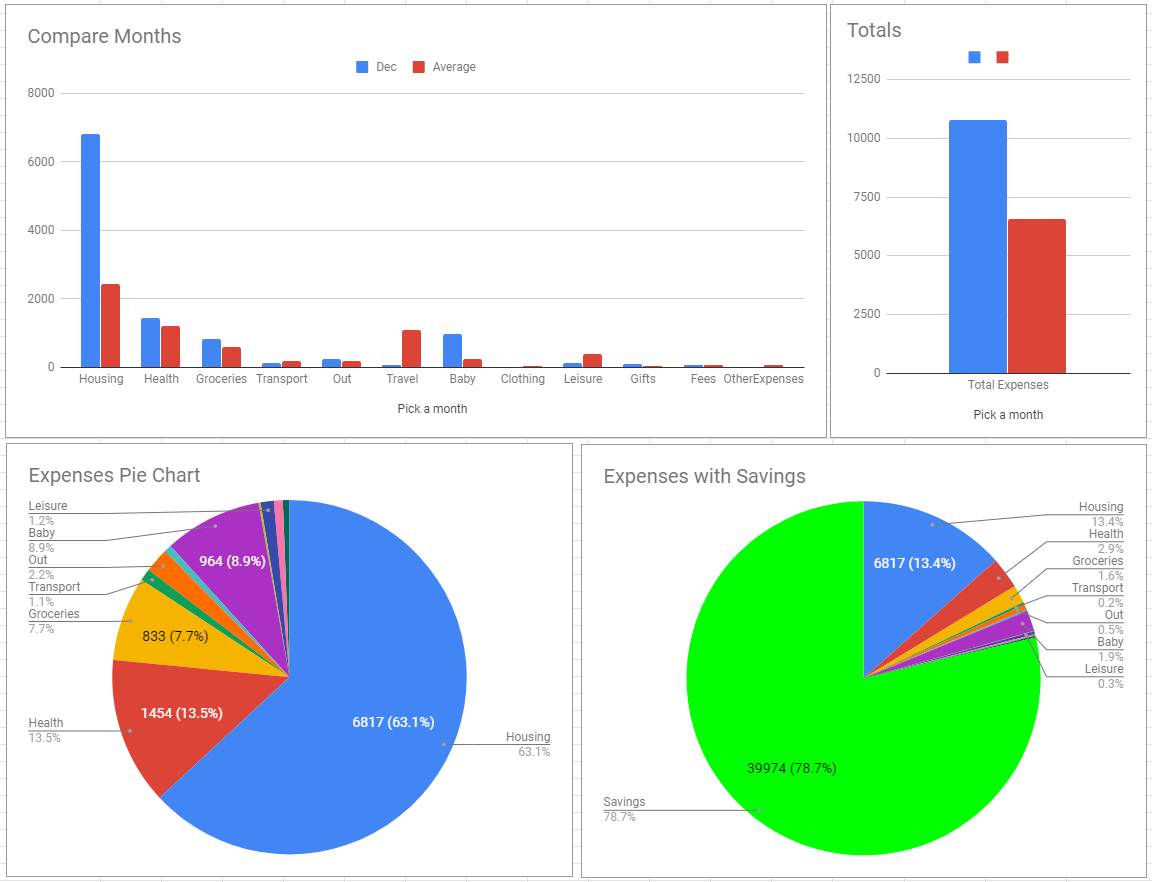

Expenses per month in Q4

- October: 6264 CHF. After two 7k+ months, it’s been a relief. But still a 6k+ month, which is too much for our standard. What drove our expenses so high have been 2 medical bills that made us immediately reach our insurances deductibles. In particular a 1678 CHF bill for Mrs RIP. Without that this would have been a 4.5k CHF month. Plus 129 CHF Mobility yearly fee, 600 CHF in travel (leftovers from Portugal, an Innsbruck visit to Mr DIP’s family, and relatives coming visiting us) and 300 CHF of cash withdrawals for Mrs RIP that I classify as leisure, even though I have no idea where this money goes (most of the time toward BabyRIP).

- November: 7610 CHF. We signed the rental agreement for the new flat (more on this is a future post) starting on November 16th. We paid the full rent in the old flat, plus half of the November rent in the new flat. Plus 150 CHF for my HalbTax, 800 CHF for a Sauna and a washing machine (???), 410 CHF for half a month child care for BabyRIP, an uncomfortable 339 CHF on restaurants (few people coming visiting us, and a couple of splurges during the move), an even more uncomfortable 745 CHF on groceries, 153 CHF for boardgames (do not ask! Ok, Gloomhaven…), and even 60 CHF in IB fees for my sell-off.

- December: 10831 CHF. A disaster! I don’t know where to start. We paid new rent (2345 CHF) and half old rent (690 CHF) since we decided to not rush and allow a full month of overlap time between the two flats. Nov 16th – Dec 15th. We failed to arrange a painless old flat transfer to some colleague of mine, which would have included furniture sale, so we had to move everything. We needed to get help from professionals and spent 1300 CHF on moving, and 600 CHF on cleaning. A 1700 CHF Ikea visit to buy half of the missing furniture (the new flat is big!) completed the picture of 6.8k CHF expenses categorized as “housing”. Add 924 CHF for BabyRIP’s child care and we’re already at all time high levels… then stopping the bleeding was impossible: there’s Christmas, EOY, a dinner out, other medical expenses, other IB trades, and other fucking boardgames: Terraforming Mars expansion “Turmoil”, and Terra Mystica expansion “Merchants of the Seas”. Regret nothing.

{kind=link}

{kind=link}

{kind=link}

Total Expenses in 2019

Housing, travel and health. Paying 14.5k CHF (8.5k insurance premiums, 6k extras) for health reasons sucks. Well, some of the travel expenses were also related to health, so the overall damage of my burnout has been greater than that.

Few more graphs follow, but I’ll save you the Average 2019 Expenses with savings, which is identical to Total 2019 Expenses scaled down by 12.

{kind=link}

Expenses per month in 2019

Starting in June, the bleeding is getting out of control. And 2020 looks even worse.

Starting in June, the bleeding is getting out of control. And 2020 looks even worse.

We’re 300k richer than a year ago, but I feel NOT good spending so much.

Luckily, compared to income per month in 2019 you can still see a lot of non-overlapping area:

Blue and Red came close in August & September, then I’ve put some space between.

Blue and Red came close in August & September, then I’ve put some space between.

Last but not least, this is a comparison with 2018 expenses on a category by category base:

We’ve lagged behind in every category except gifts, going out and… Baby. Whaat? Baby?? Seriously?

Well, in 2018 BabyRIP was born, and we faced many one-off startup expenses (not many though, we got almost all for free). But in 2019 she went to child care for a month and half, i.e. ~1.3k CHF… I find it strange that Baby expenses went down. It may also be a matter of accounting: baby food and nappies are classified as groceries, and I also guess most of Mrs RIP’s cash expenses should be classified as baby. Who cares.

Cash Flow – Savings

Total Savings for Q4: 54.4k CHF. Saving rate 68.8%.

Total Savings for 2019: 175.7k CHF. Saving rate for 2019: 69.0%. This year we failed miserably in our 70% SR quest. It would have been enough to “just” spend 8k in December. Hadn’t we changed flat we’d be at ~72%.

Still not bad though. Still much better that what I expect from each year yet to come.

While earning and spending are the two controllable metrics, saving and saving rate are just function of the first two. They’re dependent metrics, not atomic. I don’t do further in depth analysis like I do with earning and spending.

Irrelevant FIRE Metrics

2020 will be the year when I finally review our long term financial goals:

- Review my IPS.

- Review Asset Allocation and Security Selection.

- Decide if FI is still the priority or not.

- If it still is, what’s the spending target and the withdrawal rate (thus the FU Number)?

- Decide if I’m already FI. 🙂

- Realize in Switzerland we’re not FI yet.

- Decide whether to move to a cheaper country like Italy.

- Realize we won’t go back into the third world.

- Realize in Switzerland we won’t ever be FI.

- Lie down. Try not to cry. Cry a lot.

Buuuuut for now let’s pretend current FIRE metrics make sense and play this meaningless game for this last quarter 🙂

This is the FIRE Metrics screenshot for Q4 2019:

The good: LOL, we’re projected to be FI in January 2020, at the time of writing this post 🙂 Must admit the forecast is a bit optimistic, based on last 12 months of NW deltas (which have been unprecedentedly good). Anyway, at the time of writing we’re not far from 100% (99.49% on January 19th). This is supposed to be a celebration moment 🙂 Please, have a beer!

The bad: the Italian FIRE metrics section is meaningless, we’re not moving back in the near future. It’s good to know that we could be FI there though.

The ugly: Swiss FIRE metrics suck. First of all, they lack other factors like taxes and mandatory Pillar 1 contributions that an early retiree would face in Switzerland, but at least they account for real spending and not “hypothetical”. As you can see yearly expenses are growing (rolling 12 months cumulative real expenses), and they’re expected to grow more in 2020. That drives the FU Number up. Since wealth accumulation is growing at a slower pace compared to target FU Number, the Progress% is going down. Note that the “months left” metric is going down (which is counter-intuitive at first) because the last 12 months NW Delta rolling average is very high, and that’s used to forecast. So the target is moving away from us, but at least we’re accelerating toward it (for now).

So, in 2020:

- Expenses will go up.

- Income will go down.

- Markets will probably perform worse than 2019 (it’s hard to have another +30% year).

- FIRE Metrics in Switzerland will be revisited, taking into account wealth taxes, mandatory pillar 1 contributions, and maybe lowering the SWR given my conservative investment strategy and low expected yield environment due to high CAPE everywhere.

- FIRE Italy metrics will probably be thrashed.

Which means the new FIRE date in Switzerland is:

Let’s move on.

Let’s look at the Expenses and SWR graph.

The red line is the monthly allowance if we were to withdraw from our NW, assuming a SWR of 3.50%. It has caught the orange line, which is the ideal expected monthly expenses in Italy (nonsense). The overlapping of the two means FI in Italy. The blue line (current real expenses in Switzerland) is playing “catch me if you can”, and we can’t. We’re moving away from reaching FI in Switzerland.

Financial Facts

October shitty market start

During the first two days of the month our portfolio lost ~20k EUR. Even considering the salary at the end of month, our NW Delta was already at -10k. It means all else being equal, we won’t get back at the “two-days-before” wealth level until Dec 25th. Two days dive, three months grind.

This was probably the first seed of my November stocks escape.

On October 2nd I received a WhatsApp message from Mr WTF: “Hey RIP, why the fuck every October the markets crash???”

RIP: “Dunno bro, maybe there’s a pattern waiting for you to be exploited…”

I wouldn’t be surprised if he sold his stocks at the mini bottom.

But who am I to judge? I’m just someone else’s Mr WTF.

Let’s move on.

I’m Bond, a shitty bond

We were talking about stupidity, weren’t we?

Last quarterly update I told you I purchased some EU bonds:

I wanted to invest more in low risks, stocks-uncorrelated assets. The bonds above didn’t meet my criteria: IEGA is too much leveraged due to long maturity: if interest rates go up, the fund loses instantly a lot of value. IEAC is a corp (investment grade) bond, which means if the stocks go down this fund can go down as well, because of raising interest rates on new corp bonds.

First technical post will be on bond investing, promised!

So I wanted something as predictable as possible, eventually with positive expected outcome if interest rates go up. I came up with short maturity EU Government bonds.

Now, the problem is: they really suck.

But I wanted to experiment anyway. Let’s consider them as an “insurance” for interest rates going up, which I agree is not a likely scenario, but the opposite of it is irrational (interest rates going even further down) which means… I don’t know what the hell is going on, and I have no idea what I’m doing.

Anyway, this bond exercise is having huge learning value for me, so I’m ok with paying minor consequences for now.

And btw, so far my bond experience has been positive, and almost all of my bonds have been profitable so far, including the shameful IEML (high yield EM Government bond).

So… who’s the boss?? Say it again!! 😀

Ok, back on track. I wanted to buy short maturity EU Government bonds, and after a minor research I came up with IBGS. Not ultra-short maturity (1-3 years), which means they’re still leveraged in the wrong direction of interest rates, but much less.

I purchased 310 shares of IBGS on October 3rd, purchase price 144.76 / 144.77 EUR per share (~45k EUR).

Share price on Jan 19th: 144.06 EUR. Unrealized losses so far: 230 EUR.

“Who’s the boss??”

🙁

Now, the thing I don’t remember is why I decided to allocate this fund a high share of my bond allocation. That’s what you end up doing when you don’t set the right amount of time apart for such important matters.

If nothing changes in the meantime, I think the EU short maturity bond experiment is over. In December I decided I’d sell IBGS after the six month holding period, i.e. in April 2020.

In the meantime, since I decided to reduce stocks exposure in favor of bonds, I also sold some overweighted ETFs in my ideal Asset Allocation, i.e. CEUS (small cap Europe stocks).

I sold 14k EUR worth of CEUS at a small loss on October 17th. I was waiting since forever, it hurts to sell at loss but I wanted to rebalance asap.

With the CEUS proceedings I purchased 9k EUR of IEAC, and wanted to buy more IEGA, but strangely IEGA was not tradeable on IB for several days.

Few days later (October 22nd) I called IB and asked them why I can’t trade IEGA. I discovered IEGA has been delisted on LSEETF. Panic. What the hell does it even mean? Called IB again. They told me to “call iShares” or “sell the ETF manually on another StockExchange”.

After having played around with IB advanced orders interface I was able to sell all positions on BVME (Milano).

Sold 255 shares for 132.30 EUR per share. I purchased them 3 months before for 130.24 EUR per share. Realized profits over 3 months: 525 EUR. 1.6% in 3 months!

Who’s the boss?

And today, January 19th, IEGA is down to 130.01 per share!

Who’s the boss, now, who’s the alpha investor??

“RIP, shouldn’t you hold assets for at least 6 months to be sure you’re not considered a professional investor and pay 30% taxes on those IEGA peanuts profits?”

Yeah… well… I assume I was kind of forced to liquidate if the ETF has been delisted from London ETF Stock Exchange (thanks Brexit, btw).

I assume I can easily defend this move if I have to.

About bonds, I also purchased FLOT and BSV (US bonds ETFs) on December 24th, but I’ve already told you the rationale behind in a previous post.

Stocks

Nothing much to add here. On Dec 24-27th I’ve zeroed my CEUS and VB (small cap both EU and US) positions as planned.

Ah, and also all my EU REIT investments (IPRP).

My stock portfolio looks more simple now, but still not balanced as I would like:

- VT (World – ACWI): 121k.

- EIMI (Emerging Market): 68k. Ouch, I’m double exposed to EM. I need to hold on EIMI until April 2020, then I’ll close this position and buy more VT.

- VYM (High Dividend Yield US): 100k. I know, I posted so many Ben Felix Videos about how Dividends are irrelevant – and in Switzerland even tax inefficient! – but still… this illusion of an income… I’ll work on it. Maybe factor investing will be the solution.

- VYMI (High Dividend Yield World Ex US): 32k. Same as above.

Dividends

Yeah, some ETF distributed dividends. Paid some 15% US withholding tax to the nice guys over at IRS.

I’ll drop a summary of dividends in the following paragraph.

Fun fact: I sold VB (small cap US) shares on the ex-dividend date, i.e. the day the ETF starts trading without the value of its next dividend payment. I actually sold my shares at NYSE opening (3:30pm in Europe) and for a while I feared that I had both lost the dividends AND sold the stock at the ex-dividend value. Since I closed my VB positions, there was no track of pending actions, so I was pretty sure I made a “noob investor mistake”. Then, on December 31st (payment date), I received the dividends. Happy Handing!

2019 Investing in a Nutshell

2019 has been my coward investing year.

I’ve stopped sending automatically money to IB, and I accumulated cash. Only the auto-sold Hooli stocks proceedings (in USD) went directly to IB. Ok, maybe I’ve also sent some CHF sometimes, just to convert to EUR and withdraw into my EUR bank accounts. Apart from that, I’ve been “storing cash under my mattress”, and that’s not good.

Even though I could have done much, much better, I still managed to make 23.58% out of my invested portfolio.

In terms of Profits and Losses, here the full year recap (click the image to enlarge):

I think it’s worth explaining how to read and how to generate such reports.

I don’t think I need to remind you that I’m using Interactive Brokers (IB) as my investment broker. I love it, I recommend it, and I have an affiliation with it (affiliate link).

If you have an IB account you can get a standard report easily from Client Portal –> Reports –> Default Statements –> Activity.

Then select your period of choice (daily, monthly, annual, custom dates), the format (PDF or HTML) and there you go.

The screenshot above comes from the Realized & Unrealized Performance Summary section of the 2019 Annual Activity statement.

On each row, you have a security. First column is the security symbol. Easy.

Second column (Cost Adj.) I don’t know what it means, and I guess I don’t care.

Then we have the Realized section, which means real capital gains (or losses) due to trading. It means I purchased, held and then sold some assets. The section is split in profits, and losses. And each of them is split in short term and long term. Short and long term only matters to US taxpayers, or to anyone whose tax system differentiates between short and long term capital gains. In Switzerland capital gain is not taxed, but the “short” one might trigger the “Asset not held for at least 6 months” rule that might classify me as a professional investor. There are too many entries in the “S/T” columns…

Total realized Profits for 2019: 81.8k EUR. More than our 2019 expenses! Let’s have another beer 🙂

The only asset I sold at a loss has been VHYD (World High Yield Dividend stocks). It hurts to sell at a loss, but I sold it to buy VYM + VYMI in February. Mind that realized P&L doesn’t include dividends, which VHYD provided in moderate quantity over the previous 2 years, almost covering all the losses.

Then we have the Unrealized section, which means potential gains or losses I could realize by selling that asset at its current market price. It means I purchased and I’m still holding the asset. Of course I’m oversimplifying here, only considering long positions – no short positions, no leveraged positions, no options and so on.

Total unrealized Profits for 2019: 15.3k EUR. Time to get drunk!

A couple of minor underperformers (IBGS and IEAC bonds) and a couple of strong performers, candidate to get sold. EIMI, I’m looking at you. April 2020 is coming. Also VYM and VYMI, I wouldn’t sleep comfortably if I were you.

Total Profits (realized and unrealized) in 2019: 97.2k EUR. Minus 2.9k EUR of currency fluctuation. I’m holding a lot of USD cash since November 26th, and the USD dropped compared to EUR since then.

And now for something completely different: dividends!

Let’s take a look at dividends and withholding tax for 2019 (click the image to enlarge):

Total dividends for 2019: 10.5k EUR.

Total US Withholding tax paid: 1k EUR (1146 USD).

So… Add dividends to profits and we’re close to +110k EUR in 2019. Not bad!

For the sake of completeness, I also paid 409.95 EUR in trading commissions this year. Ouch. I traded a bit too much. And go to hell costly-to-trade EU-domiciled ETFs, you don’t get along with a crazy person like me.

But I also got 155.70 EUR in interest on my USD sitting cash, not bad.

“RIP, you got ‘EUR’ interests on USD cash? I’m confused…”

I got USD of course, but I changed my account reference currency from CHF to EUR, so I now get reports in EUR.

IB fun fact time: I got a notification to review some permissions and tax information on my account, like my W8-ben form, and while I was at it I also updated my account settings. And I found this:

And if I wanted to save the new account settings, this was mandatory to fill.

And if I wanted to save the new account settings, this was mandatory to fill.

IB asked me to provide my “sources of wealth”, with percentages.

This is a clear example of american bullshits, where people can’t distinguish between wealth and income. How do I mix them? Most of them are income-related entries, except inheritance, property (or is it property income / rent?), and severance. How do I know what portion of my wealth is due to income from employment vs inheritance, given that the former happens every month and the latter is a one-off? Let’s say my NW is 200k, and I got a 100k inheritance few years ago, should I say inheritance 50%? but maybe my income is 500k per year and I spend all of it, which makes income over say 10 years worth 50 times the inheritance, but still 50% of the residual wealth is the inheritance.

Bullshit.

I put 100% income from employment but laughed at the stupidity of the question.

Revolut

I forgot to mention in my Q3 Update that after many recommendations I decided to open a Revolut account and get a physical credit card.

What is Revolut? Well, I will write a full post about it, not today though.

TL,DR: it’s a “credit card”. No it’s more: “a bank account”, since you have an IBAN… but it’s also a form of online payment and peer to peer money transfer… and it’s free and its main selling point is close to zero currency conversion spread.

It’s a lot of things, and it smells like a bank 2.0. Seriously, it’s incredibly cool. After having heard about Revolut so many times in internal Hooli mailing lists I decided to give it a try.

Opening an account is a 5 minutes thing, and it only requires the Revolut app on your smartphone.

Then creating virtual debit cards takes seconds. Then ordering a physical one for free takes maybe 5 seconds. Then handling your payments, enabling online purchases, adding layers of security, classifying your expenses… it’s so modern, that you can’t tolerate other tools anymore.

For example, you can enable online payment or card swipes just before using it, and then turning the features off. No more risks of having the card cloned, or involuntary purchases. You can also block/unblock, change PIN, and many more other stuff within the app.

It’s simply a Revolut-ion in the credit cards world.

But I’m not using it full power yet, since I love the cashback on my Cumulus Mastercard (affiliate link) for Swiss CHF payments.

I’m using it for sending money p2p to friends when needed (if they go to Ikea and I ask them to buy some stuff for example), and to make payment in USD and sometimes in EUR.

Our three currency financial life was lacking a use case: USD payments. Not a very frequent use case, but sometimes I need to buy stuff on amazon.com (when .it or .de don’t have what I need), or the monthly Breaking Italy Club subscription on Patreon (why the hell Patreon only supports USD?)… now I use Revolut for that and I don’t let banks and credit cards rob me with their currency spreads.

Mind that it’s not all roses, if you use it during weekends you get a 0.5-1% surcharge.

Anyway, I totally recommend Revolut if you’re looking to get rid of banks and credit card annoying fees for transactions in a currency different than you base one.

BancoPosta

If I’ll push the pedal on Revolut usage, I might be able to close my Italian EUR bank account with Poste Italiane (Italian postal system), which is becoming ridiculous.

I was close to close it (no pun intended) in November, when they changed something in their second factor authentication backend and I have not been able to access my e-finance for 3 weeks.

I called their call center several times, and the two times out of maybe ten where the underpaid but arrogant operator didn’t put the phone down during my issue explanation I got two contradictory answers, both wrong btw.

in mid December the service restarted working correctly (by chance), lowering the priority of getting rid of this account enough to fall below my laziness threshold.

Buying a house

“Whaaat RIP? The hell are you talking about??”

No, not me!

Of course I’m not talking about me. I’m talking about… uhm… everyone.

Many friends, colleagues, and random people with cash at hand are buying a flat/house in Switzerland right now. The market is crazy. Even my dear and financial savvy friend Mr VCF approached me saying:

Mr VCF: “RIP, give me a reason to not buy a house right now.”

RIP: “Wait, what? Are you serious? Well, one reason is that everyone else is asking themself this very same question. Everyone I meet right now tells me the same: ‘stocks are overpriced, bonds have negative yields, savings accounts are shitty… but mortgage rates are low, so let’s buy a house!’. Do you remember what happened in 2005-2007 all around the world? Have you heard the term ‘Dumb Money’? If the Uber driver tells you should do X, it’s time to run away from X! Unless that Uber driver happens to be someone who knows shit“

“Those are not valid enough reasons, RIP. We’re First Principle thinkers. Please, convince me I should not do it”

“Challenge accepted… but I’m not even sure I’m qualified for it. Maybe I have some confirmation bias and I want my choice to not buy a flat in Switzerland to be the right choice. Anyway, I have scheduled to write a full post on this topic sooner or later, with pros and cons of buying vs renting. For now let’s just focus on the worst case scenario. Interest rates are so low… and people have money they don’t know where to put it so…”

“So they want to buy houses, which inflates the demand… and given interests are so low, prices go up because all shortsighted people care about is monthly mortgage interest payment…”

“And…”

“And if mortgage interests go from 1% to 3%, unlikely but an option – it happened many times in the past – the mortgage payment triples!”

“Yeah but…”

“But people do block their mortgage for up to 10 years, so if interest rates go up now one can be ‘tranquil’ for another 10 years”

“Yeah but…”

“But this is a shitty counterargument because you’re only paying interest, and pushing the problem further in the future won’t help much. And btw whomever I talk to they’re saying ‘it’s not worth to get a fixed 10 years mortgage, interest rates are much lower for shorter term mortgages!’ which is the definition of Dumb Money”

“Not only, it’s also…”

“Wait! In case interest rate raised, house prices would drop. It’s a double leveraged investment: 4x on your mortgage (financing 80% of your flat with mortgage), and another huge lever thanks to low interest rates. 1% to 3% is +200% interest payments… and in Switzerland you don’t repay the principal, so you’re only basing your decision on the interest payments…”

“Yes, but let’s not forget…”

“And if prices go down more than 20% your mortgage becomes bigger than your house value! You’d owe the bank more money than what you can get from selling the flat. Negative equity. And 3x monthly payment! Essentially everything seems cheap and convenient now, because nobody expects a black swan – which is not even that black.”

“You got it!”

“Thanks RIP, that makes sense. I’l think about it!”

“You’re welcome 🙂”

This discussion – a bit romanced here – really happened. TL;DR: it looks like everybody is signing reverse insurances here: small expected positive returns 95% of the cases, but unbounded negative returns in 5% of the cases. And maybe 5% is an optimistic prediction.

Would you play this reverse lottery?

Everyone around me is talking about it. If I had to mention only one thing I learned from my investing curiosity it is this one: “Be fearful when others are greedy and greedy when others are fearful“. Yeah, I know, it’s not mine, I never said it was original 🙂

Pillar 2 Buy in

This year I was not sure.

I’ve been doing extra voluntary payments to our Hooli Pillar 2 pension plan for last 5 years.

2019 I was not sure.

I won’t be able to get the money out for the next 3 years. Buy-ins are blocked for 3 years, even if the conditions that trigger the pension cash out are met (leaving Switzerland, self employment, buying a primary residence).

And even if you can withdraw the rest, if you made a buy in in last 3 years the tax authority can decide that you tricked the system and tax you the withdrawn money as full income.

After few weeks of thinking about it, I decided that our expected marginal tax rate was high enough that a buy in would make sense this year.

I opted for the standard 12k CHF buy-in, which doesn’t trigger tax consequences in our Canton in case we’d withdraw the non-blocked part of our extra mandatory second pillar within the next 3 years.

Taxes

I decided to pay in my third 2019 recommended tax advance of ~14k CHF in November.

I don’t need a cheap loan, I’ve way too much cash.

I explained this many times: I’m a C Permit holder, and I don’t pay taxes at source. I get “suggestions” from the tax authority to pay installments during the year, based on previous final tax bill.

I’m doing what they suggest, even though I know it’s not an accurate prediction.

Mutuel

By now you should know that 2019 has been a crappy year for RIP family health. In my previous 7 years here I’ve been paying health insurance premiums and getting nothing back. That’s why picking the highest deductible has been a no brainer for all of us.

2019, sadly, looked like this:

We both consumed all our (high) deductibles and entered the co-insurance region, where our insurance would pay 90% of expenses and we the remaining 10%.

The fact I consumed 80 CHF of co-insurance means I spent an extra 800 CHF on top of the 2500 CHF deductible in 2019 (plus some uncovered expenses): 3.3k CHF.

Given that by the end of December 2019 I already had 3 scheduled doctor appointments for 2020, and my wife was in a similar position, we decided to lower the deductibles for both of us to 300 CHF (the lowest one).

So… on December 27th I called Mutuel and… I discovered that the deadline to lower the deductible for 2020 was end of November 2019! To raise the deductible the deadline was December 31, but if you want to lower it you should tell them a month in advance.

This rule is ridiculous. When I was insured by Assura it didn’t work this way. it’s written in our contracts (and easy to find on their website) though, so I have little to complain about. I felt so stupid for not having checked in advance.

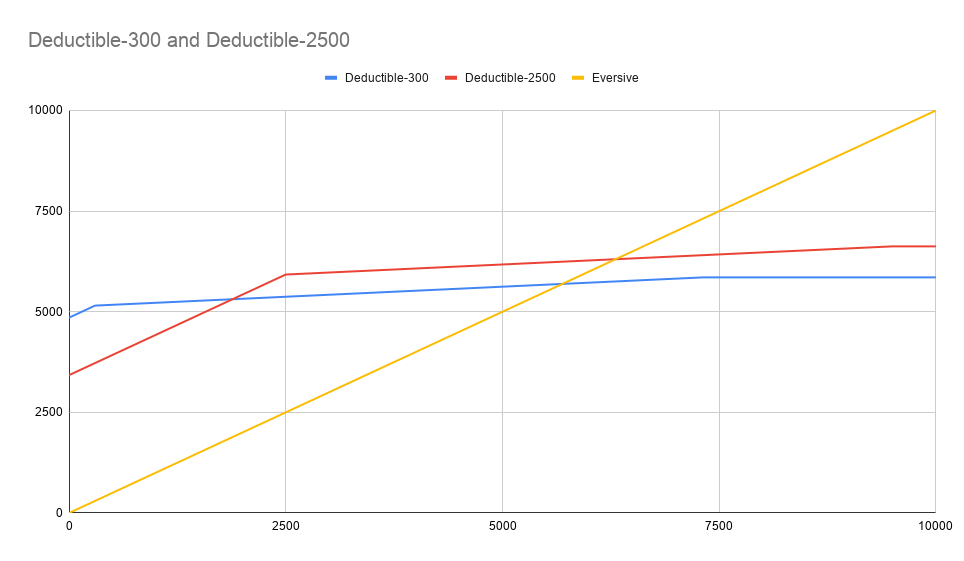

I’m pretty sure we’ll both consume the 2.5k CHF deductible again in 2020, so I tried to estimate the losses and built this graph:

X-axis is your annual medical expenses, Y-axis is your share of such expenses. Without an insurance, the graph would be Y=X, i.e. a 45 degrees line. The eversive insurance model in this graph (which tells us that if you spend less than ~5.7k CHF your insurance makes money out of you).

{kind=link}

Anyway, in the region 0-300 CHF, the high deductible model is 1.4k CHF cheaper over one year than the low deductible, while in the 2.5k+ range, the high deductible model is 550 CHF more expensive.

The break even is at 1887 CHF expenses, where the two models cost the same. I was expecting a more balanced break-even. The switch to the higher deductible would not guarante an advantage if we manage to stay below 1.9k CHF medical expenses each, and in the worst case (expenses > 2.5k CHF each) the loss would be 1.1k CHF total. Let’s see how it goes.

It’s worth reminding that this analysis is tailored to our situation: Mutuel, Telmed, our NPA code and our age. Your mileage may vary. I didn’t consider the intermediate deductibles for simplicity. A full post on Swiss health care system will appear on this blog one day.

Personal & Blog facts

Life Facts

We moved into a new flat!

The entire adventure will be documented in its own post (next one, I guess).

Rent (+ condo fees) increased from 1385 to 2315 CHF (+930 CHF/Mo).

Walkable sourface doubled from 50 to 100 square meters. From a 2 rooms apartment to 4.5 rooms. Two bathrooms. A full room dedicated to my office! Well, not exactly a “full room”… half of it is occupied by a Sauna 🙂

Not that I wanted it, but it happened to be so. More details on my next post!

Here’s my studio view from our balcony (it’s very small, it’s hard to take a picture from inside!):

Anyway, this moving experience has been exhausting. We realized we have a lot of stuff. It hurts me to admit that I’m less minimalist than I thought I was.

We moved in on December 11th but we still have many unopened boxes full of stuff. I’ve assembled so many pieces of furniture my hands still hurt. All of this without much help, and with a 18 months old baby at home.

Today (the end of January 2020) the flat is objectively 80% close to its final state, which I perceive as 100% while my perfectionist wife – who is not happy until the last pair of socks will be in the right drawer – perceives as 20%. I’m starting to enjoy the extra space and amenities, like a washing machine, an elevator in the building…

“And a dishwasher!”

Yeah… well… so far I never used it 😀

My wife is in charge of this strange animal. When it’s my turn – or if it happens to be that I’m alone, like this amazing weekend of January 17-19 – I clean my own dished the good old way, listening to podcasts and using that time to practice mindfulness 🙂

The extra space is pleasant, even though I fight other unusual battles: which of the two bathrooms should I use for… the things? Where should I take a shower? Which of the 3 sinks (!!) should I use to brush my teeth?

I used to have no choices, now I do. And it’s not stress free, because we’re lazy. If a toilet runs out of toilet paper, we don’t replenish it and just use the other one. That means sometimes you don’t know if you’re going to find toilet paper in the selected bathroom. And I don’t even know where the toilet paper reserve is stored, or if we have some – Hashtag First world problems.

Time to move on. Let’s have a RIP homemade pizza, a coke zero, and an amazing The Plain Bagel video on Cash Flow (amazing channel, discovered thanks to Ben Felix):

Back To Work

I returned to work in the new team and new role in September 30th 2019, after almost 6 months of medical leave. I switched from Software Engineer to Reliability Engineer, and from… ahem… Hooli Videos (also worked in Hooli Maps and Hooli Shopping) to Hooli Cloud.

During first couple of weeks I received many mails and personal messages by readers asking “How is it going??”. Thank you for that, I really appreciated it 🙂

How is it going?

It’s been a frustrating experience so far. No need to hide that.

As always, it’s not about people: I have amazing colleagues, really. One of them in particular took a lot of time aside from his projects to try to grow me into this role, and I can see how genuinely interested in my well being he is.

I also have an awesome managers, and I say this not only because he reads my blog (hi Manager!), but because he’s doing everything to help me fit in my new role. Or, since it seems I can’t make it work, helping me find my new way within Hooli, or eventually outside.

I know many persons who leave jobs because of bad bosses/coworkers. It’s never been my case at Hooli. When I’ll leave, the humans – and their collective knowledge – behind the company will be what I’d miss the most.

Anyway, it’s been a frustrating experience so far. As I agreed with my wife, I only had 3 complaint points, and I consumed them all within few weeks into the new role.

I’m old. I’ve been out for several months. My knowledge is outdated. My coding passion is fading and I’m not nurturing it. I’m not willing to put 150% of my brain capacity toward problems which I perceive as irrelevant and impactless in the grand scheme of things to compensate for my obsolescence. Plus the predictably un-disappeared pile of corporate bullshit, that I cleaned myself off for several months, are still there.

I was genuinely excited to start this new old adventure but it took me just a month to revert my mood, and fall back to old bad habits.

Plus my attention has been fragmented by life outside work. Daughter being sick every other day since after starting child care, me myself being sick 3 times (bronchitis 2x, gastroenteritis 1x) over the quarter, the move, relatives visiting, and a genuine desire to take time for my physical and mental health.

My journal entries of October were full of hope, my December entries percolate desperation and depression. Again.

Nope. I Fought, I Lost, Now I Rest.

Mini spoiler: In January I announced my intention to quit Hooli to my manager and my team.

We’re exploring options for a while, like working 60% – which is tempting, I must admit – but honestly, I see myself out of Hooli within a couple of months.

Now that I think about it, if I quit Hooli at the end of March, my “number of months worked” over the last few years would be:

- 2017: 12 months worked.

- 2018: 9 months worked. 3 months of paid paternity leave.

- 2019: 6 months worked. 6 months of paid medical leave.

- 2020: 3 months worked. 9 months of (sadly unpaid) “quit leave”. 😀

I spot a pattern, do you see it as well? Can you predict how many months I’ll work in 2021? 🙂

Anyway, I took some preparing action: I reduced Pillar 2 contributions to the minimum for 2020.

At Hooli we have 3 pension plans. It usually makes sense to take advantage of the tax saving benefits of the maximum contribution plan (8.5% salary contribution). Since there’s a high likelihood that I won’t earn much in 2020 I switched to the 4.5% pension plan.

On the positive side: I got paychecks, thirteenth salary, stocks vested, bonus has been announced (and it’s the lowest I’ve ever received in my seven years at Hooli, another sign of a declining career, also got a 0% salary raise) and will be cashed on January 25th. I’ve also recouped 2.5 months of Pillar 2 contributions thanks to a Hooli insurance agreement with our Pillar 2 provider that states that contributions are waived in case of long term sick leave. And as icing on the cake there’s a 20% salary bonus for for first few months (up to 12) of working as a Reliability Engineer, to compensate for the lack of on-call duties (which are compensated extra).

Plus, I went to the New York office for a week, around Halloween time. Awesome! There I met Virgil, which is still a happy Hooli employee and a nice friend 🙂

Fun fact: during my Reliability Engineer training week (early October), a senior colleague approached me and said: “Hey <Put my real name here>, you are Mr RIP, aren’t you?“.

Me: “Whaaat… how do you… yes, I’m Mr RIP 🙂 but how…”

“I’m a fan on yours! Reading your posts it was clear to me that I would have found you in this room, among the 30 new Reliability Engineers. Then knowing your age, nationality, tenure at Hooli… you know…”

It was fun, but also scary. But mostly fun 🙂

Another fun fact: once the decision to quit was forming in my head, I took a look at the internal epitaph. Yes, at Hooli we have an internal website with employees who left, some data about them: start date, end date, and an optional goodbye message. I discovered that one of my favorite musician, one that dominates by background music listening… he just quit Hooli! I didn’t even know he was a colleague of mine (a PM in UK though)! It’s a sad thing 🙁 Like eating a banana with an olive on Sunday!

This thing of looking at epitaph makes me feel like a 80 years old fart who checks who’s checking out before him. That’s hilarious. And sad.

Health

I felt 95% recovered from burnout when I got back in town at the end of September. Two months of vacation, four months of summer, 6 months of sick leave. Life has been good, I felt recharged and optimistic 🙂

I knew my mental health could have deteriorated again, so I wanted to keep an eye on things and monitor my feelings and body messages closely.

I actually kept a scoreboard of “emotions per day”. That was more work related though. I’ll share it one day.

Another tool I used to monitor my health was journaling. Well, I do that since forever. And consistently, on a daily basis, since at least 5 years. But I kept a separate journal for health (physical and mental) once coming back to work.

Maybe it’s been the overlapping of more things, but the decline in my physical and mental health in last 3 (now 4) months has been steep.

One thing at a time:

Physical Health

There was room to be optimistic at the beginning of the quarter.

I went back to running after months out, and I was doing great. In less than a month of training I was able to run a 5km below 30 minutes. It was almost 3 years I wasn’t able to go below 6 min/km. Good!

Knees

Then on October 24th I went to NYC for a working trip. On the flight back (Nov 1st) I slept in a supposedly comfortable Business seat, which can be fully reclined. Waking up over the Atlantic Ocean to use the restroom, I made some strange sleepy movement and forced an unnatural right-knee movement. It wasn’t much painful on that same day, but the following days I had troubles walking after having been sitting for a while. Then I got sick for other reasons, like a bronchitis, so I took medicines and didn’t feel knee pain. But then it came back. It’s still here, and I hadn’t checked a doctor yet.

Yes, I know, I should have gone to doctor in 2019 because my deductible has been zeroed. The situation doesn’t look better in 2020 though!

I stopped running for several reasons including the minor knee pain (plus being sick all the time, plus it’s been raining every day for a month before Christmas, plus lack of time), but resumed in early January.

The knee kind of hurts now, but I can still go running. Performances have been very modest, above 7 min/km.

Eyes

I know, you didn’t land on this blog to read this shit, you wanted to discover amazing tricks to get rich quickly… but now it’s time to talk about me. So sit down and listen 🙂

Where are my glasses?

I used to have a eagle like sight. I still do, but I used to too. My far sight is still very good. But my near sight started sucking a year or two ago. I put my shit together and faced an Oculist. I discovered I might have some minor retina problem and another one I forgot that would require a control check in May 2020.

And I need reading glasses.

See (no pun intended)? They say we extended life expectancy by X years, but I’m feeling the slow decay of my health at age 42. Do your things while you’re young. Go running that marathon! Go biking around the world, on a ship!

“How can you bike on a ship?”

Leave me alone, now I am the old fart, 80 years old who watches constructions all the time!

Anyway, I purchased two reading glasses for less than 10 CHF total (to give myself the impression that I’m still frugal) but I’m not using them much. I still prefer to make an incredible effort to try to read from near.

Lungs

“Ok I’m done. Enough, RIP. Where should I click to unsubscribe?”

I’m not over yet, come back here soon!

“I think this is the definition of Hell…”

No, what’s happening to my body, projected 10 years in the future, is the definition of (or the directions to?) Hell.

Got pneumonia in July/August. Maybe bad luck? Kept coughing for the following months though.

Got another bronchitis in October, along with BabyRIP. Coincidence? Maybe.

Got another bronchitis in December. Never felt 100% recovered since the pneumonia. This time we investigated more. We suspect Asthma. I’ve done a deep lungs check on January 7th, ad it seems I don’t have Asthma because my lungs capacity is good. But it has always been above average (used to do apnea diving), so maybe today’s “good” is a decline compared to my default status?

Anyway, I still cough a lot, and feel my breathing under sport activity is not normal.

But the doctors can’t figure out what I have.

Dietary

“Knees, eyes, lungs… are we done?”

Well, add to that a gastroenteritis episode, a mild cold and some back pain… I’d say we’re done.

“Awesome, can we move on?”

My weight is all time high.

“Oh shit… here we go again…”

I can’t help but use food to compensate some bad feelings, fears, anxiety and general perception of lack of freedom, lack of time, and the shortness of life.

Sport alone – and I’m not doing much of it – can’t keep my health under control.

“Are we done now?”

With the body, yes.

We’re moving toward Mental Health though. Let’s go there.

“Oh no… I want to kill myself!”

Let’s not get ahead of ourselves.

Mental Health

Sleep

… And let’s start this section with a physical/mental issue: I’m not sleeping as I’d like. Both in terms of quantity and quality.

My journal entries are full of “bad night of sleep”.

Sometimes it’s due to BabyRIP. She used to sleep entire nights, now it doesn’t happen since spring 2019. Even if she only wakes up once or twice per night, I know that my sleep will be interrupted. That makes my sleep suck even if baby won’t wake up that night.

Yes, she sleeps in our room even now that we have a room for her. We want to wait a few months more before forcing this change on her. She has also faced a flat move and the start of her Krippe (child care). And her room is still being used as a temporary storage space.

Sometimes it’s due to Mrs RIP snoring. I’m ultra sensitive these days, and I need absolute silence. I use earplugs, but sometimes it’s not enough. My only good nights of sleep happened when I slept on the living room sofa.

But we hosted Mrs RIP’s parents for a couple of weeks, roughly from December 20th to early January. Which was good to make progresses on the move project, but bad in terms of space and privacy. They sleep with the TV on… and snore. Both. And Mrs RIP as well. I didn’t know where to go to sleep.

Plus, I’m simply too nervous to go to bed at a normal time. I keep staying awake until 1am, at least. I keep telling myself I’d wake up at 6am, then it would be easier to go to sleep at 10pm… but I don’t do that. I can’t even make good use of that late evening time, because I’m too tired. Well, since January I’m using that evening time to meet people for my Coaching project, but that’s the only good part 🙂

End result? I’m sleep deprived. I never had this problem in my life so far.

Pessimism & Helplessness

Every aleatory outcome is going to be the worst possible. (Murphy’s law revisited)

- They’re going to kick us out of the new flat. They’re actually going to demolish this flat and will tell us this bad news soon.

- Baby has a wound? Her leg is going to be amputated.

- For sure the previous landlord will ask us 10k CHF of damages. See? The bill came! Ah, it’s 71 CHF for some minor damage in the fridge… but it’s not over yet, tomorrow they’ll send us another bill!

- The dishwasher won’t be fixed and we’ll drawn during the night.

- X didn’t reply to a WhatsApp message within 5 minutes? He’s probably planning to kidnap all of us and sell our organs on the black market.

I wrote this list out of my head but the more I think about this the more I can find many examples of my unmotivated pessimism. Everytime I watch my daughter playing, I’m ready to jump and save her life from a catastrophic event that surely will happen to her NOW.

Fun dark fact: today (January 26th) Baby fell from the stairs but I caught her before she hit the head on the ground because I was of course prepared to the worst and ready to act! I’m proud of that, but trust me: this is not healthy.

And while this pessimism is easily recognizable (and I joke about it), most of the other sad thoughts I have can be classified as a better hidden pessimism.

Like I don’t rationally think we’re ever going to have money problems, but I’m catastrophic about that. Of course all my banks and brokerage firms will go bankrupt together the day the market crashes!

I feel like I don’t have a clear way out from these negative thoughts, but I have recent memory of not feeling this way. I have good hope that once the dust settles (move is finished, career is over, winter is over and sun is back) I’ll see things with new eyes. With the help of my cheap reading glasses 🙂

Nervousness

I get irritated all the time by the most insignificant things. This might be associated to sleep deprivation though.

I use passive aggressiveness, sarcasm, and a bit of rudeness in conversation with random people as soon as my low-threshold bullshit indicator triggers.

Sometimes I swear and (in my mind) I send people to fuck off 100 times.

That doesn’t make sense. This is the default settings that David Foster Wallace talks about in This is Water. Go check it out.

… yes, it’s all a plan to make you readers stop asking for my time 🙂 Who wants to get help from a person who probably needs a lot of help himself?

Overall

It’s a very complicated situation. I feel generally bad most of the time. I lack enthusiasm and my mind is too much concentrated on problems than to enjoy the good things I have: a family, a nice new flat, a community around my blog and personal finance in general, a huge shitload of money.

But I can’t NOT focus on the fact we’re spending a lot of money each month. This is more impactful than everything else. I see expenses going up and I translate in “prison sentence”.

I look in the mirror and I don’t recognize the person who was able to live on 500 EUR per month. Willing to eat scrap food for days, and feeling great about it.

I see a weak person, that can’t fight with all his strength against lifestyle inflation. And I blame my wife, and sometimes my daughter for it.

My daughter has of course no responsibility. My wife might have some. But it’s outside her capabilities to understand that we’re not frugal if we pick a MBudget item instead of a pricey one, but then we spend 8k per month and I don’t know even why.

I would just like to see that we are in good permanent financial shape. I feel like having 1.3 Millions CHF won’t help if we’re going to spend 85-90k per year here.

And what hurts me more, is that I know I can’t get a job once I decide to finally quit Hooli. I’ve seen it all. From the above. I’ve been at the top of the pyramid. People would sell their family members to be where I am.

And I’m no more employable. My career is gone. Forever.

So even if we have enough financial security, I’m terrified by the hypothesis that one day, maybe in 10 years, I would need to find a normal job. The fact that there’s a chance of this happening paralyzes me right now.

I know these fears are not rational. I have plenty of “skills”, plenty of “money”, we can go back to Italy and be FI today… But still…

“RIP, you should let go the need to control everything. Curve balls will happen anyway, even if you’re on track with your perfect plan. It makes no sense to desire to control more than X% of the things you think you can control. And mind that X is very low.”

The clouds will go away, I hope, once I regain my full time back.

“The clouds… after leaving Hooli Cloud? 😀”

Haha, nice joke!

This summer I was excited, I know that I have this positive mood buried somewhere under layers of shitty Swiss winter weather, an unlucky sequence of health problems, some universally recognized stressful events like a flat move, and quitting your job to face unemployment. And being a parent and husband.

And also a person everyone wants to meet (more on this later).

Too much pressure.

I know the sun will rise again 🙂

Here few December journal entries, slightly redacted for privacy:

Dec 4 – didn’t go to work, didn’t sleep at night. I feel weak, I have 38° fever – went to the Doctor at 3pm and got a medical certificate and a bunch of medicines. We’ll explore Asthma once my inflammation is gone.

Dec 16 – I feel so bad for not being a minimalist. The new flat is already filled with things. And so many things to do. It drains my energies. I don’t sleep much, I’m always tired, I eat shitty food. I feel like I’m not spending much time outdoor. I don’t run anymore, my knee is hurting, maybe I should get it checked.

Dec 17 – met Mrs and Baby in city center after work, then got a Gluewein together and came home. Baby cried a lot and I’m not able to sustain the pain, the noise… I get irritated. At home, feeling weak and tired. Things can’t go on for long. Luckily it’s only 3 days left before Xmas break.

Dec 18 – Sick again… went to the Doctor for a lung check and got medicines for fungi infection. I feel sad for no specific reason. And I’m sad that I feel sad. I’m tired, but still I go to bed at 1am…

Dec 21 – A bad night. I didn’t sleep at all. I have many troubles sleeping, many problems in my head. I’m afraid of leaving Hooli, I’m disgusted by how much we are spending each month, I’m scared I won’t find any job or ways to make ends meet – Baby is sick again, she puked and she has a bad cough and a running nose. This fucking Krippe is taxing the whole family, not only from a financial point of view – we didn’t go to XYZ’s Birthday – spent evening with Baby and Mrs – Baby puked again – Entire day indoor, the weather is also shitty since weeks.

Dec 22 – Sunday, didn’t sleep the entire night again – in laws arrived from Milan – went to Ikea with Mrs, purchased 1.6k CHF of furniture including table, kitchen cupboard, studio desk, two drawers, another bookshelf – heavy boxes, several of them couldn’t fit the elevator and I had to carry to second floor with minimal help from my 75yo father in law… a physically intense day – Tomorrow we’ll assemble everything. I crave for alone time.

Dec 23 – Monday, during the night Baby puked once again. Mrs brought Baby to the pediatrician, she has the usual “3 days virus” – I mounted three bookshelves, then with my father in law we mounted the studio desk. Then the kitchen cupboard but with some problems (we forgot to purchase an essential piece and I’m working with my imagination to avoid another Ikea trip tomorrow). Then the huge table. Then both my studio drawers. I’m destroyed. Then we faced a broken dishwasher… Then I tried (and failed) to install the TV decoder… We must call the Verwaltung and UPC Cablecom tomorrow. What an amazing Xmas break.

Dec 25 – Both I and Mrs are sick. She skipped breakfast, lunch and dinner. I skipped breakfast and lunch – the weather is shitty since forever – I’m a bit sad – Merry Christmas.

Dec 29 – Another bad night with in laws watching TV at high volume, and Mrs snoring. I had to find earplugs. Desired to go to sleep in the sauna, but it’s not suited for that (yet).

Anyway, things are a bit better now. The flat move is 80% done, I have had the best gift of my life i.e. 4 days alone (Mrs and Baby went to Milan). I slept 3 nights for 8-9 hours straight. I unboxed boardgames and even a laptop that was waiting for me since weeks.

I think time alone should be recognized as a basic human right.

January 27th 2020 Update: Naval hit the target with less than 140 characters:

Parenting

Parenting is both amazing and awful. Mostly amazing, but also tough. And we just started: BabyRIP is entering the “terrible two”.

But the love of my life is becoming attached to me a lot, and that replenishes my heart 🙂

She sometimes calls me in the night and wants me to help her to sleep.

I used to be almost a stranger to her until last spring. Today we have our special language, activities, songs, games… She always looks for me when she wants to “write”. She takes pencils and paper and comes to me: “Crive!” (which is “Scrive”, or “scrivere”, i.e. “to write” in Italian).

Then I sit close to her while she makes random scribbles on a paper. Ten seconds later she hands the pencil to me and says “Papà… Bau!” which means I must draw a dog. It’s always a dog. And I’m not able to do so, but she wants me to draw a dog. In response I get creative and draw a 6 legged animals, with a beak and beards. And a hat. We build on top of that. She loves when I go creative and she can’t have enough of my crazy drawings…

The downside of this is that she now wants to play with me all the time I’m at home. She loves my studio, even though we tried to teach her that my room is not accessible, and “when the door is closed it means papà is working :)”

No way. She says “tudio… tudio… tudio!” (“Studio” is also the Italian word for… a studio) and smashes her fists on my studio door. With mixed feelings of (little) annoyance and (a lot of) pleasure I open the door and spend the following 15 minutes preventing her to open and destroy my boardgames. I have two or three (Jenga, Qwirkle, and a 200 pieces Jigsaw puzzle) that she can play with and I don’t care if she destroys them all. It’s fun, but I don’t know how I’ll manage to work on my own projects from home in the near future!

But I’m happy to spend time playing with her, sometimes it makes me think that “who the fuck cares about productivity and projects??”. It’s been amazing to have had 4 days alone, but if life would always be like that it would be an inferior life. Find the right balance is my struggle.

Anyway, she started going to Krippe on mid November, just two days per week. We pay 920 CHF/Mo for this. Mrs is not working, nor actively looking for a job.. but for her sanity of mind we had to send Baby to child care for at least two days per week! Now that we’re almost done with house tasks Mrs will be able to focus on her long term projects.

Learning

Given all of the above (plus all of the below) you’d think my curiosity stream would have been cut, but it’s not.

I’ve been learning and reading and following other bloggers, podcasters, youtubers all the time.

I keep sending myself mails with subject “Curiosity: XYZ”, in the hope I’ll keep up with CuriosiTips posts, but I think I’ve found a better solution.

I’m actually journaling (yes, these days I journal everything) my learning activity in a Learning Journal (which is just a Google Doc on my personal account) since mid September 2019, i.e. four months at the time of writing this post. I think I’m going to clean it for privacy and then share it as it is in the near future. So you can take a look in real time what I’m reading, and some of my quick notes about the source.

Here’s a screenshot of my LJ from mid January:

“Cool RIP, I can’t wait to take a look at your Learning Journal 🙂”

Waaait a minute, I’m not sure I’m going to keep LJ in this form I just shared, i.e. a Google Doc 🙂

“But… in your screenshot it seems you’re currently using it… what’s wrong with you??”

I know, let me explain: I’m working a lot on the meta level now. I’m looking for a smarter and better way to store my knowledge outside my brain. It’s called Personal Knowledge Management, and it’s a real thing. There’s an online course, Building a Second Brain by Tiago Forte that I was tempted to subscribe to, but in the end I didn’t. I’ve never tried apps (Evernote, Notion, etc) because I want freedom.. and the more I look around, the more I see smart people claiming all you need is a text document, or a Database – while a lot of Millennials jump from app to app.

I was actually writing my Personal Knowledge Management design doc, where I tried to define the perfect way to store and recall information… when Nat Eliason triggered me with Roam. You can see from the screenshot that I got exposed to it around Jan 12th (well, you can’t tell it from the screenshot) and after a couple of days thinking about it, I decided to give it a try.

It’s awesome so far, with a lot of pros and few (non-negligible though) cons. I’m going to talk about it in a future post, but so far, so good. I actually cracked it when I started a note on my favorite quotes. Yes, I have a Google Doc with quotes (75 pages) I love. When I pasted it into Roam (1000+ blocks created) it started to slow down kill my browser.

Anyway, I’m going meta meta, writing a Roam note about Roam as a tool about learning. One day.

Here’s for example a partial screenshot of my notes on this article by Joyous And Swift on Addiction, Happiness and Stress. Strongly recommended.

I don’t have time here to illustrate how roam works, just read the article by Nat Eliason and go find more info around – and please tell me what you think!

Anyway, I’m telling you this because I’m moving my Learning Journal into Roam. It’s so much better to have pages linked together!

Let’s move on.

About the “what to learn”, I decided I want to give structure to my learning activity and have “Learning Projects“, i.e. self contained projects of variable duration (daily, weekly, monthly, yearly) with clear focus.

Of course I created a Google Doc named… you guessed right: Learning Projects (LP) and – you guessed right again – I will share it after I clean it.

Here’s a screenshot of two yearly projects (maybe I’m going to pick Rationality this year).

Here you can find a screenshot of some of the Monthly and Weekly projects.

{kind=link}

{kind=link}

Sadly, reading (non fiction) books is moving out of my active habits. I prefer the non linearity of high quality content on the internet.

…And you guessed right once more: this LP doc might be moved into Roam if I decided to go all in with it.

I’m scared of moving everything into a startup tool (with exporting and importing features though) which seems too good to be true, but with some scaling problems and a lack of “calendar” and “TODO” support. I sent an email to the devs and the founder replied:

They are hiring…

“RIP… are you thinking… what exactly?”

No. Nothing. Of course my software engineer career is gone. Of course…

But maybe…

Ok, two more things and then we’ll jump into next section.

My Farnam Street Learning Community subscription expired, and I didn’t renew it. I did get a lot of value out of it, and I also saved a lot of content for future consumption, but I wasn’t able to follow the actual community (the forum) and connect with people there. I didn’t give it high priority.

I believe the FSLC has amazing value, and I’d bet I’ll subscribe again in future, once my life simplifies and my focus on learning could grow undistracted from the need to generate money (hey, they call it FI!). But for now: FSLC, see you later! GG!

Last but not least, I have a set of resources that I consume over and over again. I want to make a list and establish a yearly (or maybe quarterly) routine of preferred resources consumption. Ok, I hate the word “consumption” but I can’t find a better word.

This list contains more philosophical resource. It’s not “Learning”, but maybe “Spirituality”. But still you can learn a lot by re-reading the same stuff, especially it it resonated with you deeply.

This WIP list contains things like:

- This is Water

- The Egg (I want to make a Theater piece with a friend on this short novel, and he accepted!)

- Life is not a Journey

- The Age of the Essay

- Definitely Not Purpose

- … maybe I should add half a dozen of the best TED Talks, and dig into my list of best articles read.

This list is expected to grow. Of course I have saved copies of each resource on my local cloud, in case they’d be taken down from the net.

Enough.

Blogging

It’s been an hard quarter from so many angles (family, move, work, health) but to quote George Best:

I’ve spent a lot of time learning and blogging. The rest I just squandered.

Jokes apart, I’ve not spent as much time as I wanted on my blog – I’m behind 10-15 posts – but I managed to keep it alive – and growing, actually.

I don’t know why, but the audience is growing even though I’m not publishing much.

I don’t do anything that’s recommended to increase metrics. I hate following “best practices”, being SEO friendly and so on, but I do care about organic metrics. If behaving authentically makes more people to come visiting and giving me nice feedback, then I’d proven wrong all the “10 ways to make your blog audience skyrocket!”.

Of course it’s part of first principle thinking: it’s the chef approach. I don’t follow other rules, I just think that if I put passion, quality, and authenticity something good will happen.

The blogs who most inspired me are Waitbutwhy and Livingafi (Doom, I know you read comments on your blog and still reply to them… Doom, please, come back!). They’re the opposite of what a blog should be. No clickbait titles, no “between 500 and 1000 words posts”, no “top 5 something something…” (well, WBW did something like that, but it was awesome anyway).

All I do is blogging as I like (not enough though), behave like metrics don’t count, and then be happy if I’m impacting someone’s life. And be happier if the amount of life impacted is growing!

Anyway, this is the growth (almost +100% in 2019) of my blog:

Almost 200k views, and January 2020 is on path to become the month with most views so far.

What would happen if I’d put more effort into it? I don’t know… Well, the good news is: when I quit Hooli, I will divert office time to my blog. If I decide to move back to Italy, I can afford to not give a fuck about monetization and making a dime out of it ever.

The bad news is that while we are staying in the expensive Switzerland, I need to find a way to make the effort financially justifiable, so something very baaaaad is going to happen!

Joking of course! I will still try to avoid making money like pests.

I’ll write a full post about my blogging ethic in the future.

In the meantime, a nice graph or posts / words per year:

In 2016 nobody was reading my blog, and I still wrote 51 (holy crap!) posts in half a year (started blogging in June). The quality of my English and the quality of my posts were crappy, but they were already annoyingly long (2k+ words on average). I kept going, I didn’t give a fuck about audience 🙂

Not-fun fact: I don’t know what happened in 2017, but it seems I cut the effort… maybe the wedding thing?

Anyway, 366k words written for this blog, and it doesn’t count this post, which is flying at all time high length, and all the half baked drafts!

There’s enough for 5 novels, a series! I could have written my Fantasy saga instead of this blog. Now that I think about it… Or, this blog could be sitting among George R.R. Martin books (now I see why it takes so long for him to deploy a book)

Writing for my blog is not the only blogging activity I do. It’s actually the one I’ve neglected the most in last few months.

Writing for my blog is not the only blogging activity I do. It’s actually the one I’ve neglected the most in last few months.

Meeting and interacting with people has become the predominant one. And I’m not sure I like it this way. I want to write more, I want to raise the quality of my work, I want to review old posts and write maybe a book, a guide, a course. I want to talk about investing with the proficiency of a CFA, and talking about life goals, learning, what to do with your time, why “work” must be redefined, what is “money”, what is “time”… as you can see it’s not about FIRE anymore.

Anyway, pushing the pedal on human interaction has happened both organically and intentionally.

Organically because with more effort I put into this blog, more people I’m able to reach. Word of mouth, press coverage, and my posts being shared helped with the outreach. It was not a goal, it was a consequence of existing, working hard, and maybe produce some quality content (among an ocean of shit).

Intentionally because of three reasons:

First: I’m trying to be nice. I reply to all mails and comments. This generates a lot of nice human interactions, and opportunities to make new friends – but I’m close to the tipping point where keeping up with the inflow consumes all the available time for creativity. I apologize in advance if I won’t reply to your email or comment or social media interaction. It’s just that with my limited time I want to optimize for impact – and 1:1 doesn’t scale much.

Second: I almost never turned down a request to meet in person or digitally. In the last 4 months I’ve had on average 4-5 lunches/dinners per week with people who I met thanks to my blog. Roughly half of them are Hooli colleagues (!!). There’s something special in meeting someone who knows almost everything about you and you don’t know much about them 🙂 And there’s something even more special with meeting someone for the second time! With the many readers/friends/bloggers I’ve met more than once, I’ve installed a relationship that won’t disappear tomorrow. Someone broke the last barrier and came into my new flat, and our kids played together. Priceless 🙂